Basic Rates of Taxes remain the same.

Surcharge

The rates of surcharge applicable for A.Y.2016-17 are as follows -

(i) Individual/HUF/AOP/BOI/Artificial juridical person/

Co-operative societies/Local Authorities/Firms/LLPs:

Where the total income exceeds Rs.1 crore, surcharge is payable at the rate of 12% of income tax

(ii) Domestic company:

(a) In case of a domestic company, whose total income is > Rs. 1 crore but ≤ Rs. 10 crore:

Where the total income exceeds Rs. 1 crore but does not exceed Rs. 10 crore, surcharge is payable at the rate of 7% of income-tax

(b) In case of a domestic company, whose total income is > Rs.10 crore:

Where the total income exceeds Rs. 10 crore, surcharge is payable at the rate of 12% of income-tax

(iii) Foreign company:

(a) In case of a foreign company, whose total income is > Rs. 1 crore but ≤ Rs. 10 crore:

Where the total income exceeds Rs. 1 crore but does not exceed Rs. 10 crore, surcharge is payable at the rate of 2% of income-tax

(b) In case of a foreign company, whose total income is > Rs.10 crore:

Where the total income exceeds Rs. 10 crore, surcharge is payable at the rate of 5% of income-tax.

Residence & Scope of Total Income

(a) CBDT to prescribe the manner of computation of period of stay for an Indian citizen, being a member of the crew of a foreign bound ship leaving India [Section 6(1)]

Basis for determining the period of stay in India for an Indian citizen, being a member of the crew of a foreign bound ship leaving India [Notification No. 70/2015, dated 17.8.2015]

According to Rule 126, in case of an individual, being a citizen of India and a member of the crew of a ship, the period or periods of stay in India shall, in respect of an eligible voyage, not include the period commencing from the date entered into the Continuous Discharge Certificate in respect of joining the ship by the said individual for the eligible voyage and ending on the date entered into the Continuous Discharge Certificate in respect of signing off by that individual from the ship in respect of such voyage.

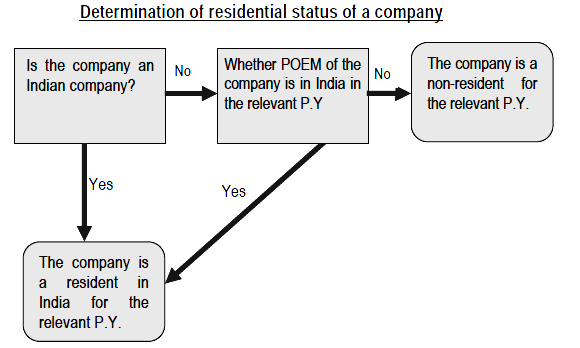

(b) Residential status of a company to be determined on the basis of “Place of Effective Management” [Section 6(3)] Effective from: A.Y. 2016-17

Explanation to section 6(3) defines “place of effective management” to mean a place where key management and commercial decisions that are necessary for the conduct of the business of an entity as a whole are, in substance made.

Incomes which do not form part of Total Income

“Yoga” included as a specific category in the definition of “charitable purpose” [Section 2(15)] Effective from: A.Y.2016-17

Conditions to be satisfied “advancement of any other object of general public utility” to constitute a “charitable purpose” [Section 2(15)] Effective from: A.Y.2016-17

(i) The definition of “charitable purpose” under section 2(15) has been amended to provide that the advancement of any other object of general public utility shall not be a charitable purpose, if it involves the carrying on of any activity in the nature of trade, commerce or business, or any activity of rendering any service in relation to any trade, commerce or business, for a cess or fee or any other consideration, irrespective of the nature of use or application, or retention, of the income from such activity, unless:

(1) such activity is undertaken in the course of actual carrying out of such advancement of any other object of general public utility; and

(2) the aggregate receipts from such activity or activities, during the previous year, does not exceed 20% of the total receipts, of the trust or institution undertaking such activity or activities, for the previous year.

(ii) In effect, an additional condition has been inserted that such activity has to be undertaken in the course of actual carrying out of such advancement of any other object of general public utility. Further, in the place of an absolute limit of Rs.25 lakhs, a limit based on percentage of total receipts has been specified upto which receipts from an activity in the nature of trade, commerce or business is permissible without affecting the “charitable status” of the trust or institution.

Increase in the maximum limit for exemption of transport allowance: The maximum limit upto which transport allowance can be claimed as an exemption by an employee to meet his expenditure for the purpose of commuting between the place of his residence and the place of his duty has been increased from Rs. 800 p.m. to Rs. 1,600 p.m. In case of a blind or deaf and dumb or orthopedically handicapped employee with disability of lower extremities, the maximum limit has been revised from Rs. 1,600 p.m. to Rs. 3,200 p.m.

To read the full article: Click here

Click here to view/access classes on Law, Ethics & Communication

CAclubindia

CAclubindia