The advent of Goods and Services Tax marked a classic reform in Indirect Taxation Regime. Government always aspired to keep compliance procedures simple and transparent flow of input tax credit. The Government had a vision to introduce a unique concept of 'Invoice-to-invoice matching' in its Indirect Tax realm. Owing to technical glitches in Government's IT systems, this dream never translated into a reality. The Government continued to make efforts to turn its vision into action. Government is finally set to implement the 'New Return System' from October 2019.

This journey started in May 2018 when the Government made its first public announcement on its plan of introducing 'New Return System'. The proposed system is a refined version of the framework proposed at the inception of GST. Post several discussions amid GST Council and representations from Industry, the relevant forms were placed on GST portal in March 2019. The release of offline tools last month, marks the government's firmness towards attaining its timelines.

The proposed system categorises the taxpayers into two baskets:

• Taxpayers having turnover below Rs 5 crores (forming 93 percent of the total taxpayers) - Option of monthly or quarterly return filing

• Taxpayers having turnover more than Rs 5 crores - Monthly return filing

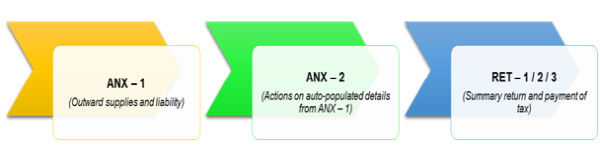

The framework of upcoming monthly / quarterly compliances can be understood below:

The new system will work upon the concept of Upload-Lock-Pay(ULP), facilitating real time uploading as well as acceptance of invoices. It totally links recipient's ITC on supplier's submission of documents along with a flexibility of taking provisional credit on Missing Documents.

Some other important features include:

• Option for a quarterly return filer to choose the form (Normal, Sahaj, Sugam), depending upon the diversity of its supplies

• Visibility of supplier's return filing status to recipient and its linkage with availment of ITC

To view / enroll the course on "New GST Forms" by CA Puneet Bansal: Click here

• Six-digit HSN reporting

• Bifurcation of ITC into inputs, input services and capital goods

• Separate amendment forms

• SMS facility for NIL return filers

It is clearly evident that implementation of 'New Return System' will imprint a complete revamp of compliances under GST. For a taxpayer, it is critical to take a pause and think over on the following points to plan a smooth transition from old to new system.

• Impact of 'Invoice-to-invoice matching' - For example, treatment of ITC for which documents are not at all uploaded by the supplier.

• Integration of ERP to generate data in alignment with new forms - For example, To account for the requirement of six-digit HSN and bifurcation of credits

• Monthly responsibility matrix of compliance personnel - For example, who will be responsible for matching of purchase register with ANX-2 for taking actions on auto-populated documents, following up with suppliers etc.

• Treatment of transitional cases - For example, Supplier missed uploading of an invoice in GSTR - 1 but recipient claimed corresponding ITC in GSTR-3B, how the same will be accounted for in new return formats.

For an in-depth legal and practical understanding of 'New Return System', you may join us in our e-learning certification course 'A Walk Through the New GST Forms'.

To enroll: Click Here

CAclubindia

CAclubindia