What is GST

"Goods and Services Tax" would be a comprehensive indirect tax on manufacture, sale and consumption of goods and services throughout India, to replace taxes levied by the Central and State governments.

GST is a tax that we need to pay on supply of goods & services. Any person, who is providing or supplying goods and services is liable to charge GST.

GST is a consumption based tax/levy. It is based on the “Destination principle.” GST is applied on goods and services at the place where final/actual consumption happens.

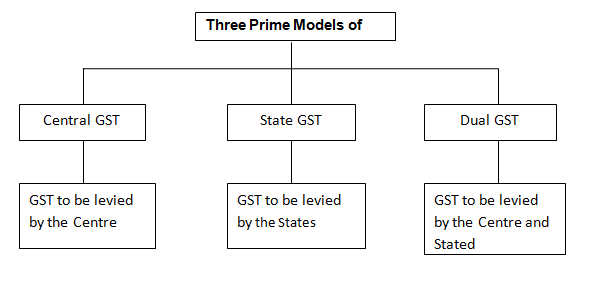

Models of GST

There are three prime models of GST

Expected model of GST in India:

In India, the GST model will be “dual GST” having both Central and State GST component levied on the same base.

For example, if a product have levy at a base product of Rs. 1000 and the rate of CGST and SGST are 10% then in such case both CGST and SGST will be charged on Rs. 1000 i.e. CGST will be Rs. 100 and SGST will be Rs.100.

The significant features of Dual GST are as under:

1. There will be Central GST to be administered by the Central Government and there will be State GST administered by the State Governments.

2. Central GST will replace existing CENVAT and Service tax and the State GST will replace State VAT.

3. The proposed GST will have two components – Central GST and State GST – the rates of which will be prescribed separately keeping in view the revenue considerations, total tax burden and the acceptability of the tax.

4. Certain components of petroleum, liquor and tobacco are likely to be outside GST structure.

Further, State Excise on liquor may also be kept outside the GST.

As per the proposed GST regime, the input of Central GST can be utilized only for the payment of CGST and the input of State GST can be utilized only for payment of SGST.

Subsuming of Existing Taxes

|

Sl. No. |

Subsumed under CGST |

Subsumed under SGST |

|

1 |

Central Excise Duty |

VAT / Sales tax |

|

2 |

Additional Excise Duties |

Entertainment tax (unless it is levied by the local bodies). |

|

3 |

Excise Duty-Medicinal and Toiletries Preparation Act |

Luxury tax |

|

4 |

Service Tax |

Taxes on lottery, betting and gambling. |

|

5 |

Additional CVD |

State Cesses and Surcharges (supply of goods and services) |

|

6 |

Special Additional Duty of Customs - 4% (SAD) |

Entry tax not in lieu of Octroi |

|

7 |

Surcharges |

|

|

8 |

Ceses |

What will be out of GST?

• Levies on petroleum products;

• Levies on alcoholic products;

• Taxes on lottery and betting;

• Basic customs duty and safeguard duties on import of goods into India;

• Entry taxes levied by municipalities or panchayats;

• Entertainment and Luxury taxes;

• Electricity duties/ taxes;

• Stamp duties on immovable properties;

• Taxes on vehicles.

Benefits of GST implementation

• The tax structure will be made lean and simple.

• In the long run, the lower tax burden could translate into lower prices on goods for consumers.

• The Suppliers, manufacturers, wholesalers and retailers are able to recover GST incurred on input costs as tax credits. This reduces the cost of doing business, thus enabling fairer prices for consumers.

• It can bring more transparency and better compliance.

• Number of departments (tax departments) will reduce which in turn may lead to less corruption.

• Companies which are under unorganized sector will come under tax regime.

GST rate Worldwide

GST rates of some countries are given below.

|

Country |

Rate of GST |

|

Australia |

10% |

|

France |

19.6% |

|

Canada |

5% |

|

Germany |

19% |

|

Japan |

5% |

|

Singapore |

7% |

|

Sweden |

25% |

|

India |

27% ^ |

|

New Zealand |

15% |

|

Pakistan |

18% |

|

Malaysia |

6% |

|

Denmark |

25% |

^ Proposed rate.

Conclusion

The taxation of goods and services in India has, hitherto, been characterized as a cascading and distortionary tax on production resulting in mis-allocation of resources and lower productivity and economic growth.

Under the new structure, all different stages of production and distribution can be interpreted as a mere tax pass-through, and the tax essentially ‘sticks’ on final consumption within the taxing jurisdiction.

CAclubindia

CAclubindia