Tax Deduction at source is a way by which leakage of revenue to Government is ensured to some extent. Like direct Tax, TDS is also implemented for Indirect Tax.

")

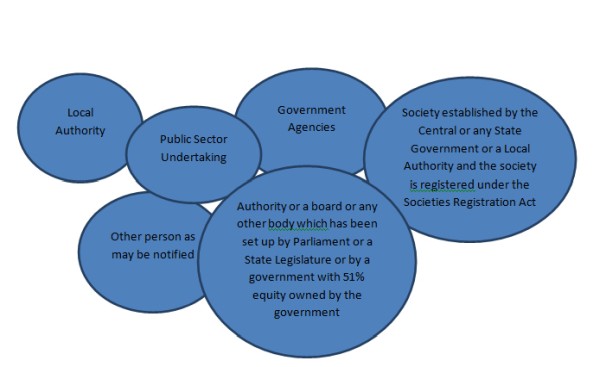

Following persons are liable to deduct tax under GST Law

- Local Authority

- Government Agencies

- Public Sector Undertakings

- Society established by the Central or any State Government or a Local Authority and the society is registered under the Societies Registration Act, 1860

- An authority or a board or any other body which has been set up by Parliament or a State Legislature or by a government, with 51% equity owned by the government

- Other person as may be notified by the Government

Rate of TDS

TDS is to be deducted at 2%on payments made to the supplier of taxable goods or services or both, where the total value of such supply under an individual contract, exceeds Rs. 2,50,000/-.

Non applicability of TDS

Tax is not required to be deducted if Location of supplier (LOS) and Place of Supply (POS)[BOTH] are different from the Location of recipient (LOR).

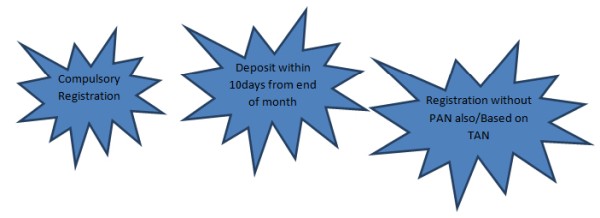

Registration Requirements

- Compulsory registration without any threshold limit

- Registration can be obtained based on PAN or TAN

Date of deposition of TDS

TDS shall be deposited to Government within 10 days from the end of the month in which tax is deducted.

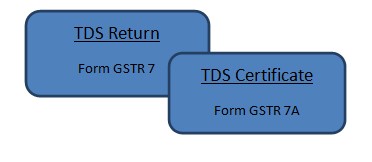

Filing of TDS Return and Issue of TDS Certificate

TDS return (Form GSTR-7) within 10 days from the end of the month.

Person deducting tax has to issue the TDS certificate in form GSTR-7A to the concerned person within 5 days of depositing the tax to the government.

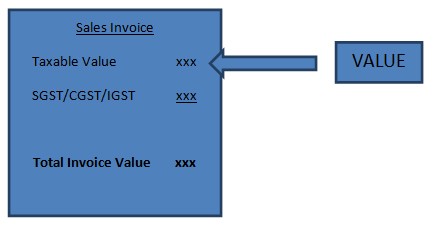

Value on Which TDS needs to be deducted

Value of supply is to be taken as the amount excluding the tax indicated on the invoice. This means TDS shall not be deducted on the CGST, SGST or IGST component of invoice.

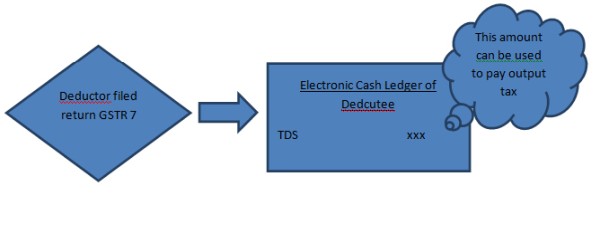

Automatic Reflection of TDS

Once the deductor files the return, the TDS shall be reflected automatically in the electronic cash ledger of deductee. The deductee can claim credit of this tax deducted and use it for payments of other taxes.

CAclubindia

CAclubindia