This article has been updated with latest amendments till July 2018

The income tax Act prescribes a specific mode for calculation of income and taxability in the case of Association of Persons.

Let's first discuss what is an Association of Persons.

An association of persons means an association in which two or more persons join in a common purpose or common action. The term person includes any company or association or body of individuals, whether incorporated or not. An association of persons may have companies, firms, joint families as its members - M.M Ipoh v CIT [1968] 67 ITR 106(SC).

Now lets see how income of Association of Persons (AoP)/ Body of Individuals(BoI) is determined.

Computation of Income of AoP

The total income under the different heads i.e. Income from house property, Profits or gains of business or profession, Capital gains, and income from other sources shall be worked out ignoring incomes exempt under Sections 10 to 13A.

From this make adjustments for the following:

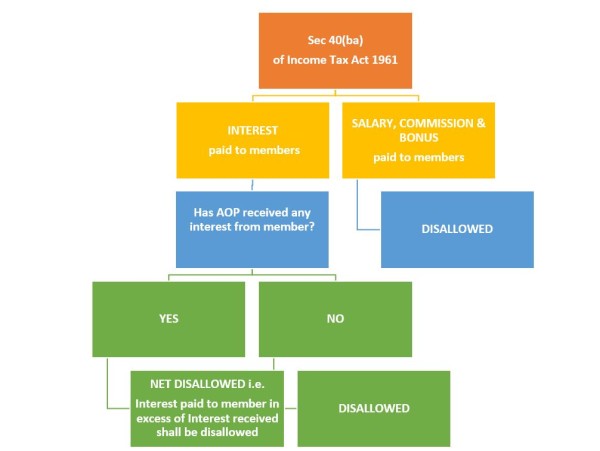

i. If salary, commission, bonus or remuneration is paid by AoP/BoI to members, it will be added back. It may be noted that remuneration paid for actual services is also disallowed. This is due to the express provision in Section 40(ba).

ii. If interest is paid by AoP/BoI to members, it will be added back. But the following should be kept in mind:

Additional points to be kept in mind while disallowing interest:

Where interest is paid by an AoP/BoI to any member who has also paid interest to the AoP/BoI, the amount of interest to be disallowed shall be limited to the amount by which the payment of interest by the AoP/BoI to the member exceeds the payment of interest by the member to AoP/BoI.

If individual is member in representative capacity:

(a) Interest paid by the AoP/BoI to such individual or by such individual to AoP/BoI except as member in a representative capacity, shall not be taken into account;

(b) Interest paid by the AoP/BoI to such individual or by such individual to the AoP/BoI as member in a representative capacity and interest paid by the AoP/BoI to the person(s) so represented to the AoP/BoI, shall be taken into account.

Let me elucidate with an example:

Mr. William is a member of an AoP on behalf of his HUF i.e. in representative capacity. AoP pays interest on capital Rs. 1,50,000 to Mr. William in individual capacity. This amount will be deductible for the AoP as Mr. William is member in representative capacity but payment is made in individual capacity. Had Mr. William received interest on behalf of his HUF, such payment would've been disallowed in the hands of AoP.

If individual is member in individual capacity:

Interest paid by the AoP/BoI to such individual shall not be taken into account, if such interest is received by him on behalf, or for the benefit, of any other person.

Example: Mr. Varun is a member of an AoP i.e. in individual capacity. He receives interest on capital Rs. 1,50,000 made by his wife. This means he has received interest in representative capacity. Hence it will be allowed in the hands of AoP. Had Mr. Varun been a member on behalf of his wife, such interest received would have been disallowed by virtue of Section 40(ba).

Also, deductions under Sections 80G, 80GGA, 80GGC, 80-IA, 80-IAB, 80-IB, 80-IC, 80-ID, 80-IE and 80JJA are to be adjusted (if any).

Total income thus obtained is taxed either at rates applicable to individual or at the maximum marginal rate, or a rate higher than maximum marginal rate.

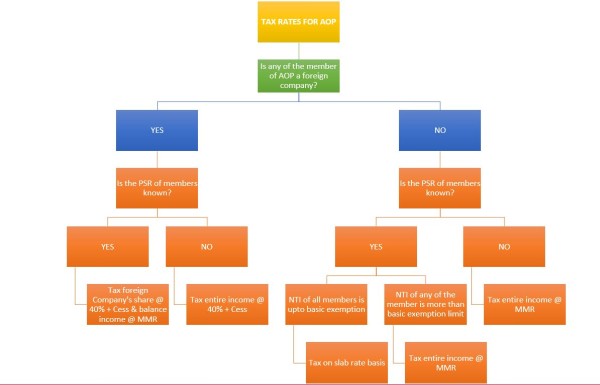

Calculation of Tax of AoP

Tax of AoP/BoI shall depend on whether shares of members are determinable or not.

Shares of members are determinable:

a. If no member of AoP/BoI has income exceeding maximum amount not chargeable to tax:

The tax is chargeable on the total income of an AoP/BoI at the same rate as is applicable in the case of an individual.

b. If any member of AoP/BoI has income exceeding maximum amount not chargeable to tax:

In this case, AoP is taxed at maximum marginal rate.

And finally, if the total income of any member of the AOB/BOI (whether or not it exceeds the maximum amount not chargeable to tax in the case of an individual) is chargeable to tax at a rate higher than the maximum marginal rate, tax shall be charged

i. on that portion of the total income of the AOP/BOI which is relatable to such member at such higher rate

ii. and the balance of the total income of the AOP/BOI shall be taxed at the maximum marginal rate, 33.99%.

Let me illustrate the third point above with an example:

RAY Ltd (a foreign Company taxed at 40% + cess), Mr. Mark and Ms.Vidya are members of an AoP sharing profits in 9:5:6. Personal incomes of the members are as follows:

RAY Ltd- Nil

Mr. Mark - Rs. 30,000

Ms. Vidya - Rs. 13,000.

Taxable income of AoP is Rs. Rs. 2,30,000( including Rs. 70,000 long term capital gains)

Here, tax of AoP is determined as under:

|

Particulars |

Amount |

Share of Members |

||

|

RAY Ltd |

Mr. Mark |

Ms. Vidya |

||

|

Long term capital gains |

70000 |

31500 |

17500 |

21000 |

|

Other Income |

160000 |

72000 |

40000 |

48000 |

|

Total |

230000 |

103500 |

57500 |

69000 |

Here, Rs. 72,000 being share in 'other income' of RAY Ltd is taxed at maximum marginal rate.

Tax liability of AoP:

On Rs. 72,000 at 40% + cess (RAY Ltd being a foreign company) Rs. 29,664

On balance Rs. 1,58,000 (Rs.2,30,000- Rs.72,000)

- At 20% + cess on LTCG, Rs. 70,000 Rs.14,420

- At max marginal rate on balance Rs. 88,000 Rs.29,911

Total tax Rs. 73,995

B. Shares of members are indeterminable:

Tax is charged on the total income of the AOP/BOI at the maximum marginal rate. However, if any member is charged at a higher rate than the maximum marginal rate, the income shall be taxed at such a higher rate.

Calculation of Tax of members:

The assessment of the members of AOP or BOI depends on whether the AOP or BOI is chargeable to tax at the maximum marginal rate or rates applicable to individual or is not chargeable to tax at all.

Let's discuss it here below:

(i) Where AOP or BOI is chargeable to tax at a maximum marginal rate or any higher rate, the share of profit of a member is not included in his total income.

(ii) Where AOP or BOI is taxed at rates applicable to the individual, the share of profit of a member from AOP or BOI is to be included in the total income of the member. But, the member is entitled to a rebate of tax on the entire share of profit at the average rate of tax applicable to total income.

(iii) Where AOP or BOI is not chargeable to tax at all, the share of profit of a member from AOP or BOI is included in his total income and he will pay tax on it. He is not entitled to any rebate of tax on such profits.

NOTE : MMR currently is 30% + 15% Surcharge + 3% Education cess = 35.535%

SOME IMPORTANT CASE LAWS ON 'ASSOCIATION OF PERSONS'

- Land inherited by three brothers is compulsorily acquired by the State Government. Whether the resultant Capital Gain would be assessed in the status of 'Association of Persons' or in their individual hands - GOVINDBHAI MAMAIYA (2014) (SUPREME COURT)

- AOP is an association in which two or more persons join in for a common purpose. However, in the given case, the property came into possession of assessees by operation of law i.e. through inheritance. There is no business involved. The basic test for making an assessment in the status of AOP is absent. Hence income shall be taxable in their individual hands and not in the status of AOP.

- Whether rental income from plinths inherited by individual co-owners from their ancestors be assessed in the hands of AOP or in their individual hands - SUDHIR NAGPAL (2012) (PUNJAB & HARYANA H.C.)

- High Court observed that merely accruing of income jointly to two or more persons would not constitute them as an AOP. They need to satisfy the basic condition of joining for a common purpose. Thus, income shall be assessed in the status of individual and not AOP.

This article has been updated with latest amendments till July 2018

CAclubindia

CAclubindia