1. Cigarette Industry in India

India is the second largest producer of Tobacco in the world (after China).India is also the second largest exporter of Tobacco/ Tobacco products in the world with exports of more than $1 Billion. Out of the annual tobacco production of ~ 800 million kgs, over 60% is exported. Geographically speaking, 80% of raw tobacco production comes from Andhra Pradesh, Gujarat and Karnataka. Cigarettes exports constitute a major portion of India's tobacco product exports.

Currently, the biggest player in India's cigarette industry is ITC, with a market share of 72% (i.e. every 3 out of 4 cigarettes in India). Godfrey Phillips holds 12% market share, with the rest occupied by small manufacturers.

ITC's major cigarette brands include Wills Navy Cut, Gold Flake Kings, Gold Flake Premium lights, Gold Flake Super Star, Insignia, India Kings, Classic (Verve, Menthol, Menthol Rush, Regular, Citric Twist, Ice Burst,Mild & Ultra Mild), 555, Silk Cut, Scissors, Capstan, Berkeley, Bristol, Lucky Strike, Players, Flake and Duke & Royal

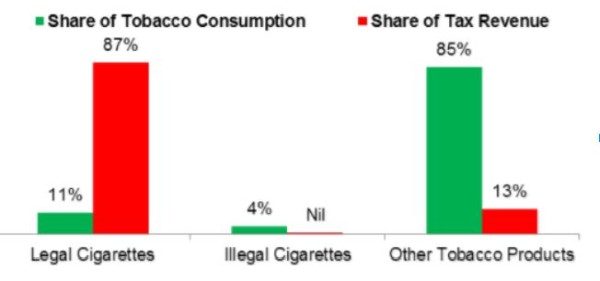

Out of the total tobacco consumers (domestic), cigarette smokers account for 11% and the remaining 89% are those who smoke 'bidi' and chew tobacco. However, 87% of the revenue from tobacco products is from sale of cigarettes.

2. Taxation on Cigarettes in India

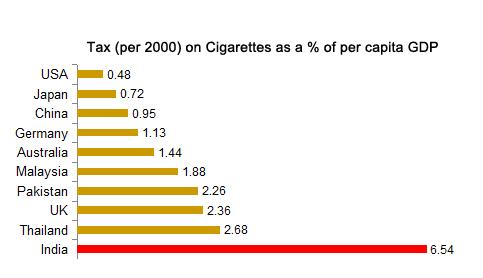

Taxes rates on cigarettes in India is one of the highest in the world. The below graph shows that the tax on cigarettes in India as a % of per capita GDP is 14 times that of USA.

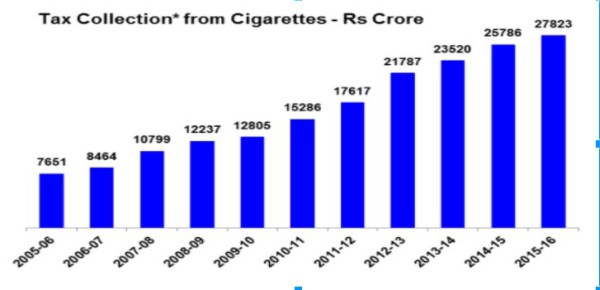

Pre-GST, the Tobacco Industry contributed significantly to the government treasury by way of Central Tax (i.e. Excise Duty) and State Taxes (i.e. VAT and Entry Tax). The tax revenue collected from tobacco products was more than Rs. 31,000 cr annually (out of which, Rs. 27,823 cr was from cigarettes)

Despite having just 11% share of total tobacco consumption, legal cigarettes contribute 87% of tax revenue.

Until 1987, cigarettes were taxed under an ad-valorem structure (i.e. based on a % of the estimated value of transaction), which had many drawbacks. It resulted in valuation disputes (due to fraudulent suppression of values by keeping costs at unrealistically low levels) with huge amount of litigation and which also discouraged value addition and improvement in product quality, which aided smuggling.

In view of the above problems related to ad-valorem duty, a length-based specific duty structure was introduced during the year 1987, which ensured transparency and efficiency in tax collection/ administration.

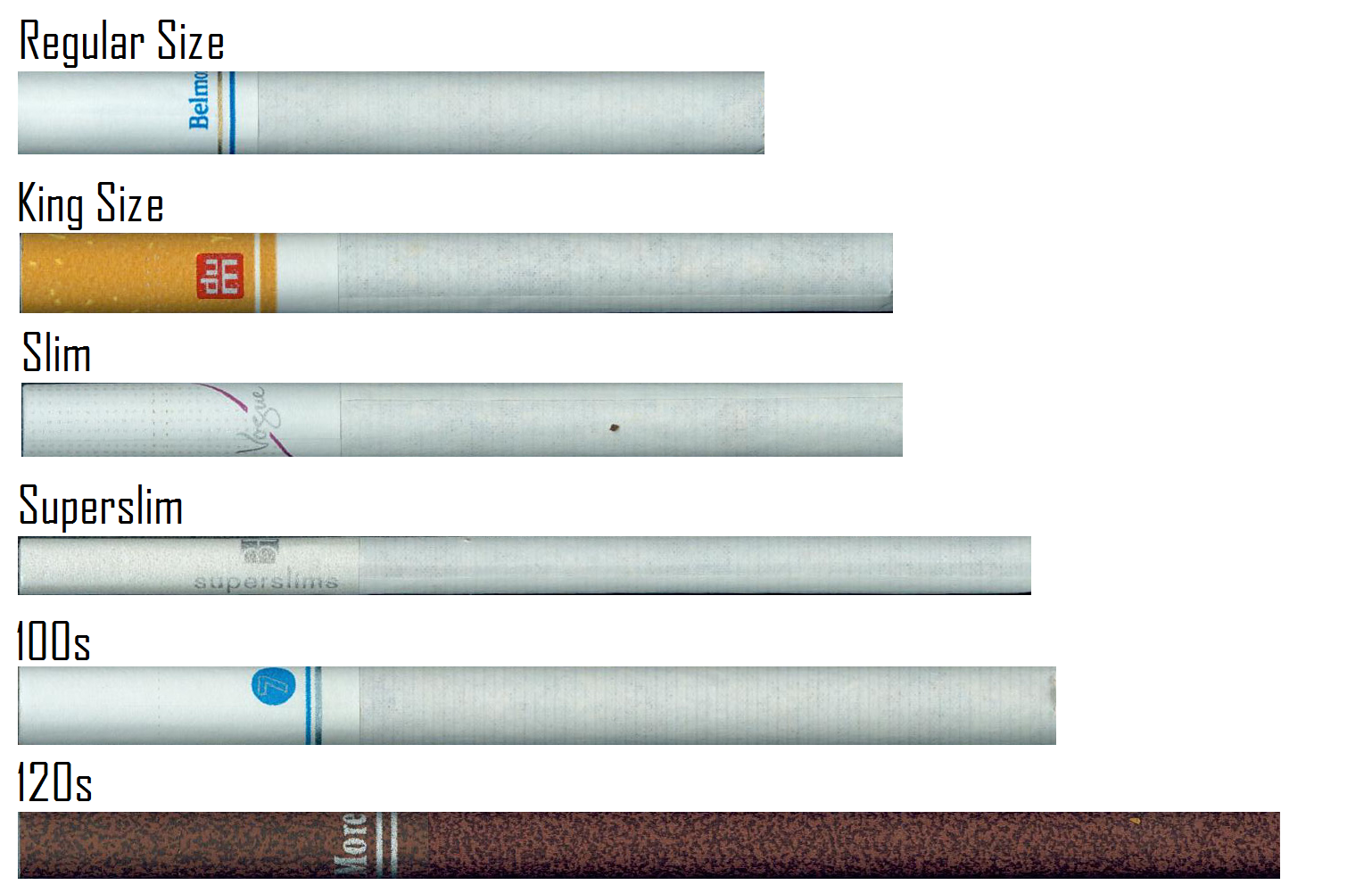

Cigarettes come in various lengths/ sizes (i.e. 64mm, 69mm, 74mm, 84mm, 100mm, 120mm, etc)

The normal size of some of the popular cigarettes manufactured by ITC (ie, Gold Flake Lights and Gold Flake Kings) is 84mm (ie, king size).

In the past, owning to high rates for lengthy cigarettes, cigarette companies have reduced the length to keep prices at a uniform rates (such that the volumes are not affected)

3. Pre-GST Regime

- India had a complex structure to tax cigarettes under the Pre-GST regime - based on the length and filter.

- To understand the impact of GST on cigarettes, it may be useful to have a broad understanding of the Pre-GST regime taxation on cigarettes. Under the erstwhile system, cigarettes used to attract Central Excise and State VAT and local entry taxes.

- India has heavily taxed cigarettes because it is classified as a demerit/ sin good. With the passage of each annual budget (Finance Act), we could expect the tax on cigarettes to increase.

- As per the Tobacco Institute of India ('TII'), Excise duty on cigarettes (under the erstwhile tax regime) have cumulatively gone up by 131% over the last 6 years.

- Basic Excise Duty ('BED') and Additional Excise Duty ('AED') is imposed on cigarettes. The below tables show the the increase in the BED and AED over the past few years:

Basic Excise Duty on Cigarettes #:

|

Finance Act, 2012 |

Finance Act, 2013 |

Finance Act, 2014 |

Finance Act, 2015 |

Finance Act, 2016 |

Finance Act, 2017 |

||

|

Tariff Item |

Cigarettes |

Rate of duty per thousand sticks (INR) |

|||||

|

2402 2010 |

Non Filter < 65mm |

509 |

509 |

990 |

1,280 |

1,280 |

1,280 |

|

2402 2020 |

Non Filter |

1,463 |

1772 |

1,995 |

2,335 |

2,335 |

2,335 |

|

2402 2030 |

Filter < 65mm |

509 |

509 |

990 |

1,280 |

1,280 |

1,280 |

|

2402 2040 |

Filter 65 to <70mm |

1,034 |

1249 |

1,490 |

1,740 |

1,740 |

1,740 |

|

2402 2050 |

Filter 70mm-75mm |

1,463 |

1772 |

1,995 |

2,335 |

2,335 |

2,335 |

|

2402 2090 |

Others |

2,373 |

2,875 |

2,875 |

3,375 |

3,375 |

3,375 |

# Basic excise duty is levied under the First Schedule to the Central Excise Tariff Act, 1985

Additional Excise Duty on Cigarettes in India*:

|

Finance Act, 2013 |

Finance Act, 2014 |

Finance Act, 2015 |

Finance Act, 2016 |

Finance Act, 2017 |

||

|

Tariff Item |

Cigarettes |

Rate of duty per thousand sticks (INR) |

||||

|

2402 2010 |

Non Filter < 65mm |

70 |

70 |

70 |

215 |

311 |

|

2402 2020 |

Non Filter |

110 |

110 |

110 |

370 |

541 |

|

2402 2030 |

Filter < 65mm |

70 |

70 |

70 |

215 |

311 |

|

2402 2040 |

Filter 65 to <70mm |

70 |

70 |

70 |

260 |

386 |

|

2402 2050 |

Filter 70mm-75mm |

110 |

110 |

110 |

370 |

541 |

|

2402 2090 |

Others |

180 |

180 |

180 |

560 |

811 |

* Levied under Seventh Schedule to the Finance Act, 2005, as amended from time to time

- In addition to the above, a National Calamity Contingency Duty ('NCCD') of INR 90-235 per thousand sticks is also levied depending upon the length of the cigarette. (NCCD is levied under the Seventh Schedule to the Finance Act, 2001)

- Apart from the above taxes imposed by the Central Government, the State Governments too imposed taxes on cigarettes.

- The State VAT on Cigarettes varied from State to state. Given below are the rates of VAT on cigarettes prevalent in various states during the Pre-GST regime:

|

State |

VAT Rate |

|

Karnataka |

20% |

|

Maharashtra |

35% |

|

Delhi |

20% |

|

Tamil Nadu |

30% |

|

Kerala |

30% |

4. GST Regime

In order to simplify the existing tax system and to prevent cascading effect of taxes (i.e. tax on tax), GST was introduced with effect from 1 July 2017 (which has subsumed VAT, Excise duties such as BED and AED)

Under the GST regime, cigarettes are taxed at 28%

This is in line with the Fitment committee recommendations that the GST rates on cigarettes maybe kept at 28% (in line with the weighted average VAT rate of 28.7%)

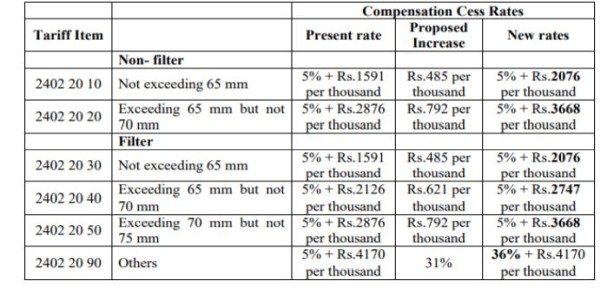

In addition, the committee also recommended that a Compensation Cess maybe levied on cigarettes at rates equal to 1.05 times the specific excise duty rates [net of natural calamity contingency duty ('NCCD')]

On 28 June 2017, the GOI notified the compensation cess rates as below @:

|

Tariff Item |

Cigarettes |

Ad-valorem Cess |

Compensation Cess per thousand sticks |

|

2402 2010 |

Non Filter < 65mm |

5% |

1,591 |

|

2402 2020 |

Non Filter 65 to <70mm |

5% |

2,876 |

|

2402 2030 |

Filter < 65mm |

5% |

1,591 |

|

2402 2040 |

Filter 65 to <70mm |

5% |

2,126 |

|

2402 2050 |

Filter 70mm-75mm |

5% |

2,876 |

|

2402 2090 |

Others |

5% |

4,170 |

@ Compensation cess rates were notified vide Notification No 1/2017 - Compensation Cess (Rate), dated 28 June 2017 under section 8(2) of the Goods and Service Tax (Compensation to States) Act, 2017

- However, this method of setting compensation cess did not take into account the cascading effect of tax in the earlier regime (ie, VAT was being charged on the value including excise duty).

- Given the above, the tax incidence on cigarettes in GST regime came down as compared to the earlier regime and as a result, the stocks of cigarette companies soared. While the government has welcomed the reduction of tax incidence on items of mass consumption, it has sought to discourage it in case of sin goods/ demerit goods such as cigarettes.

- Thus, w.e.f 18 July 2017 the GST council increased the compensation cess rates on cigarettes as mentioned below

5. Increase in the Compensation Cess on Cigarettes *

The Compensation Cess rates on cigarettes were increased with effect from 00 hours of 18 July 2017 as below:

* Vide Notification No. 3/2017 - Compensation Cess (Rate) dated 18 July 2017 (Refer Press Release dated 17 July 2017

Cigarette industry body, TII has appealed to the GST council to review the recent increase in cess on cigarettes and roll back the tax to the revenue neutral rate. It has contended that the steep increase would adversely affect tobacco farmers and the legal cigarette industry and would encourage smuggling and illicit cigarette trade in the country. Further, it has also argued that such increase is significantly higher than the estimated reduction in the tax incidence on cigarettes under the GST regime

The immediate impact on increase in the Cess would be that cigarette makers would increase the prices to protect margins. Such price increase would be anywhere upto 10%- 20% based on category. (Refer Illustration)

6. Impact on share prices

The demand for cigarettes are not totally price-inelastic as increase in prices (due to steady increase in excise duty for cigarettes) has adversely affected the volume of sales over the past few years.

Shares of cigarette manufacturers tanked on 18 July 2017, with the shares of ITC being the worst hit, its stock falling as much as 13% (over 60% of ITC's revenues comes from cigarette business). The shares of other cigarette manufacturers such as Godfrey Phillips and VST Industries also fell sharply by 5% and 8% respectively.

7. Illustration of Tax (per stick) on Cigarettes (Pre GST vs. GST Regime)

|

Gold Flake Kings - 84mm |

|||

|

Particulars |

Pre-GST |

GST Regime Prior to 18 July 2017 |

GST Regime 18 July 2017 onwards |

|

Factory Cost + Margin (A) |

5.50 |

5.50 |

5.50 |

|

Basic Excise Duty (B) @ Rs. 3,375 per thousand sticks |

3.38 |

0 |

0 |

|

Special Excise Duty (C) @ Rs. 811 per thousand sticks |

0.81 |

0 |

0 |

|

Natural Calamity Cess (D) @ Rs. 235 per thousand sticks |

0.24 |

0.24 |

0.24 |

|

GST @ 28% (E) = (A) * 28% |

0.00 |

1.54 |

1.54 |

|

GST Compensation Cess (F) = 5%/ 36% + Rs. 4,170 per thousand sticks |

0.00 |

4.445 |

6.15 |

|

Total Cost (including excise/ GST) (G) = Sum of A to F |

9.92 |

11.72 |

13.43 |

|

Distributors Commission @ 10% (H) = G*10% |

0.99 |

1.17 |

1.34 |

|

Total Cost (I) = (G) + (H) |

10.91 |

12.89 |

14.77 |

|

VAT @ 28.7% (J) = (I) * 28.7% |

3.13 |

0 |

0 |

|

GST @ 28% (on value added)(K) =H*28% |

0.00 |

0.33 |

0.38 |

|

Retail Price (L) = I + J + K |

14.0 |

13.2 |

15.1 |

|

Total Tax paid (Excise + VAT + GST) (M) |

7.55 |

6.55 |

8.30 |

|

Effective Rate of Tax (N)= M/L*100 |

53.78% |

49.53% |

54.82% |

Conclusion:

We can observe the following from the above: The effective rate of tax on cigarettes has changed from ~50% to ~55% due to the increase in the overall taxes (i.e. from Rs. 6.55/- to Rs. 8.30/- per stick) as summarized below:

Tax per stick of cigarette:

|

Nature of Tax |

Pre-GST |

GST Regime Prior to 18 July 2017 |

GST Regime 18 July 2017 onwards |

|

Excise Duty (BED + AED) |

4.18 |

- |

- |

|

NCCD |

0.24 |

0.24 |

0.24 |

|

VAT |

3.13 |

- |

- |

|

GST |

- |

6.31 |

8.06 |

|

Total Tax |

7.55 |

6.55 |

8.30 |

- Cigarette prices may have to be increased by 7-8% (i.e. from Rs. 14 to Rs. 15.1) due to the increase in the cess and would cause an additional burden to the consumers. As on 31 December 2017, cigarettes prices have been increased significantly and is selling at Rs. 17/- per stick

- The increase in prices may adversely affect the volume of cigarettes sold and may affect the profit margins of cigarette manufacturers (analysts estimate that the YoY volumes to drop by 5% and 2% in FY18 and FY19 respectively)

CAclubindia

CAclubindia