Indian tax law requires employers to deduct TDS from the salaries of non-resident employees working in India. This deduction, governed by Section 192, is mandatory for any taxable wage, irrespective of where it is received. While the employee's residential status determines if the salary is taxable, the employer's responsibility to deduct TDS is clear once it is. Complying with these rules is a fundamental part of managing cross-border payroll and meeting legal obligations.

Applicable Section and Taxability

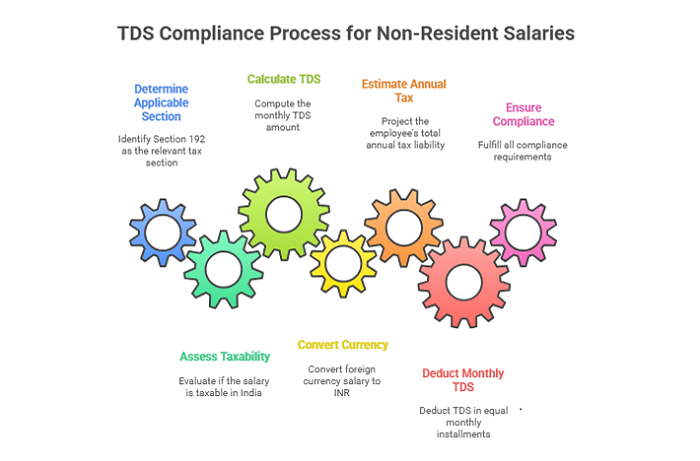

Applicable Section: Tax on salary paid to non-residents must be deducted under Section 192, not Section 195 (which applies to other income like interest, royalties, or capital gains).

Taxability: The salary is taxable in India if it is earned for services rendered here. This qualifies as income accruing in India, irrespective of the place of payment or receipt. The employee's residential status is the key factor in determining this taxability.

TDS Calculation & Timing: The TDS is required to be deducted monthly, computed using the standard individual income tax slab rates.

How TDS is Calculated?

Currency Conversion: When salary is paid in a foreign currency, it must be converted to Indian Rupees using the State Bank of India's telegraphic transfer (TT) buying rate applicable on the date of the tax deduction.

Calculation Method: The employer estimates the non-resident's total annual tax liability based on their projected salary. The TDS is then deducted in equal monthly installments based on this estimate.

Non-Taxable Salary: Salary received for services rendered outside India is generally not taxable in India, barring any specific provisions in the Income Tax Act or an applicable Double Taxation Avoidance Agreement (DTAA).

Other Key Points

No Basic Exemption: Unlike other TDS provisions, there is no minimum threshold for deducting tax on salary. TDS under Section 192 must be applied to any amount that is taxable in India.

Refund Process: If a non-resident employee is due a tax refund upon leaving India, and the employer had borne the tax liability, the refund can be directly issued to the employer.

Key Compliance Requirements for the Employer

The employer has four primary compliance obligations:

- Obtain a TAN: Possess a valid Tax Deduction and Collection Account Number (TAN).

- Timely Tax Deposit: Deposit all deducted tax with the government within the stipulated deadlines.

- File Quarterly Returns: Submit TDS returns for salary payments quarterly using Form 24Q.

- Issue Form 16: Provide the non-resident employee with a TDS certificate in Form 16 after the end of the financial year.

Summary Table

| Payment Type | Applicable Section | TDS Rate | Taxable in India |

| Salary to Non-Resident | Section 192 | Slab Rate | If for services in India |

| Other payments (NRI) | Section 195 | Varies | If income arises in India |

In summary, all salaries paid for services rendered in India to non-resident employees are subject to TDS under Section 192 at standard slab rates, placing the responsibility for correct deduction and compliance on the employer. Given the complexities involving residential status, source rules, and potential Double Taxation Avoidance Agreement (DTAA) implications, seeking guidance from a tax professional is strongly recommended to ensure accurate tax liability assessment and full regulatory adherence.

FAQs

Is TDS applicable on salary paid to non-resident employees?

Yes, TDS is applicable if the salary is for services rendered in India, irrespective of whether the payment is made in India or abroad. The employer must deduct TDS under Section 192 at the applicable income tax slab rates for each month the salary is paid.

Who is responsible for deducting TDS on salary paid to non-residents?

Any employer (individual, firm, company, etc.) paying salary to a non-resident is required to deduct TDS under Section 192 if the salary income is taxable in India.

How is TDS calculated for non-resident salary?

TDS is calculated on the estimated annual salary of the employee after considering allowable exemptions and deductions. The total tax liability is divided by 12, and the monthly TDS is deducted from the salary payment.

Is TDS required for salary paid for services rendered outside India?

No, salary paid for services rendered outside India is generally not taxable in India, and therefore TDS is not required on such payments.

What happens if the non-resident doesn't have a PAN?

If a non-resident employee does not furnish a PAN, TDS should be deducted at the higher of the prescribed rate or 20% under Section 206AA.

CAclubindia

CAclubindia