Q. 1 (a): CNC India Ltd. is engaged in the manufacture of machines. It has supplied one machine to M/s. Advaith India Ltd. At a price of Rs.11,25,000 (excluding excise duty & VAT). Cash discount @ 3% on price of the machinery is allowed to M/s. Advaith India Ltd. Further, following additional amounts as indicated below have been charged from M/s. Advaith India Ltd.

|

Sl. No. |

Particulars |

Rs. |

|

(i) |

Expenses pertaining to installation and creation of the machine at Advaith India factory. (Machine was permanently affixed to earth) |

40,000 |

|

(ii) |

Pre-delivery inspection charges (charges separately by CNC India Ltd.) |

11,250 |

|

(iii) |

Cost of durable and returnable packing (such cost has been amortised and included in the cost of the machine |

5,000 |

|

(iv) |

Warranty Charges charged separately by CNC India. |

1,00,000 |

|

(v) |

Advertisement and publicity charges borne by Advaith |

60,000 |

|

(vi) |

After sales service chargers (charged separately by CNC India Ltd.) |

20,000 |

Advaith India has supplied material worth Rs.50,000 free of charge to CNC India Ltd. for being used in production of machine. Determine the Assessable value for calculation of Central Excise Duty payable thereon from the aforesaid information. There was no opening or closing inventory. CNC India is not eligible for exemption in terms of notification 8/2003 it. 01-03-2003 during the current financial year 2016-17 when the clearance of the machine was effected. Make required assumptions and show the working Notes separately. (Need not calculate Central Excise Duty payable)

Ans. 1(a): Computation of Assessable Value of Machine Supplied by CNC India Ltd

| Rs. | ||||

| Price before discount and taxes | 11,25,000 | Amount payable is after cash discount only |

||

| Less discount @3% | 33,750 | |||

| Price after discount | 10,91,250 | |||

| SL No. | Add Other Expenses chargeable to duty, collected from customer. | |||

| (i) | Expenses pertaining to installation and creation of the machine at Advaith India factory. (Machine was permanently affixed to earth). |

|

Non chargeable as not in connection with sale. | |

|

(ii) |

Pre-delivery inspection charges (charges separately by CNC India Ltd.) |

11,250 |

Chargeable which enhance the marketability |

|

|

(iii) |

Cost of durable and returnable packing (such cost has been amortized and included in the cost of the machine). |

5 |

Non chargeable, assumed not included in the price above |

|

|

(iv) |

Warranty Charges charged separately by CNC India. |

1,00,000 |

Includible as per Section 4(3)(d) |

|

|

(v) |

Advertisement and publicity charges borne by Advaith |

60,000 |

Includible as part of consideration |

|

|

(vi) |

After sales service chargers (charged separately by CNC India Ltd.) |

20,000 |

Includible as part of sale agreement |

|

|

(vii) |

Supply of material worth Rs.50,000 free of charge by customer |

50,000 |

Includible as per Rule 6 of Valuation Rules |

|

|

Assessable Value |

13,32,500 |

|||

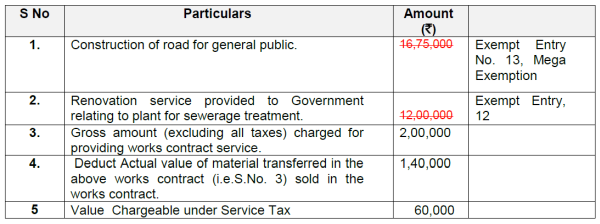

(b) Compute service tax liability (to be paid in cash) from the following particulars of services of M/s. Utkarsh & Co. for the month of October, 2016

|

S.No. |

Particulars |

Amount (Rs.) |

|

1. |

Construction of road for general public. |

16,75,000 |

|

2. |

Renovation service provided to Government relating to plant for sewerage treatment. |

12,00,000 |

|

3. |

Gross amount (excluding all taxes) charged for providing works contract service. |

2,00,000 |

|

4. |

Actual value of material transferred in the above works contract (i.e. Sl.No. 3) (VAT under the relevant state VAT Law has been paid on this value). |

1,40,000 |

|

5. |

Service tax paid on input service (excluding SBC and KKC). |

2,800 |

|

6. |

SBC paid on input services. |

100 |

|

7. |

KKC paid on input services. |

100 |

|

8. |

Excise duty paid on the capital goods, purchased during the year, used in the provision of works contract service. |

2,000 |

|

9. |

Excise duty paid on inputs used in the provision of works contract service. |

10,750 |

M/s. Utkarsh & Co. has paid service tax of Rs. 2, 50,000 during the preceding financial year. Rate of service tax is 15.00 %. (14% + 0.50% Swachh Bharat Cess +0.50 % Krishi Kalyan Cess) Working notes should form part of your answer.

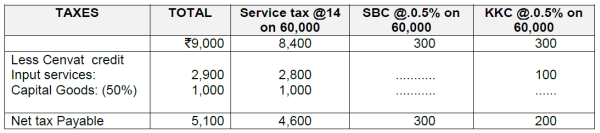

Ans 1 (b): Computation of Service Tax Liability (to be paid in cash) for M/s. Utkarsh & Co. for the month of October, 2016.

Service tax payable:

Notes:

1. No cenvat credit is available on material used in works contract as they are not inputs as per the definition under Rule 2(k) of the Rules, 2004.

2. Only 50% of the credit on capital goods has been taken as it was mentioned that capital goods were purchased are during the year.

3. SBC shall be paid in cash only as no credit is allowed on that.

4. KKC is available as credit but can be used only for paying KKC on output service.

To read the full article: Click here

CAclubindia

CAclubindia