An individual salaried person with small share market transactions filed wrong ITR and skipped reporting capital gains/losses for which his case was picked up for scrutiny.

Case Study: Incorrect ITR Filing for Stock Market Loss

An individual's salary was Rs 386,400 and has a stock market income which he incurred a short-term loss of Rs 2,765 from selling shares.

But,

The individual incorrectly filed ITR 1 instead of ITR 2, which is not the appropriate form for salary income and capital gains.

For incorrect reporting, his case was selected for income tax scrutiny.

Why was the case selected?

This error led to their case being selected for income tax assessment because the sales and purchases were not properly shown in ITR 1.

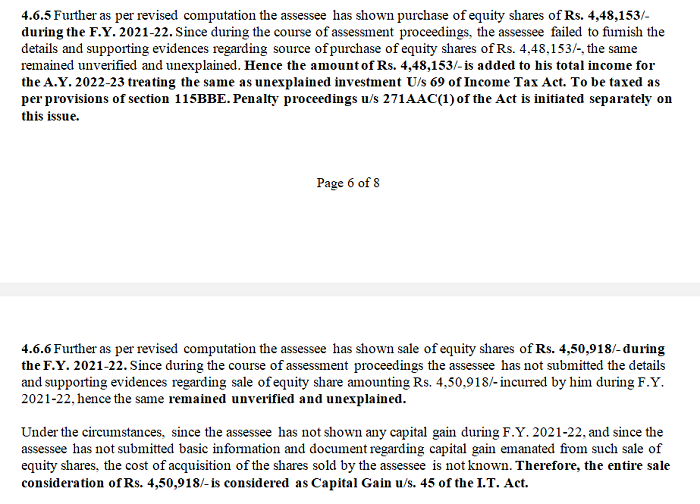

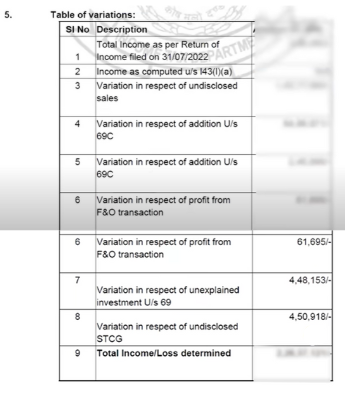

The Income Tax Officer added both the full sale value Rs 4,50,918 and the purchase value Rs 4,48,153 to the individual's income, imposing a 60% tax under Section 115BBE and a 10% penalty on the purchase, without providing the benefit of the cost.

Normally, only the net profit after deducting cost should be taxed, but in this case, the department ignored demat statements and treated the entire sale and purchase transactions as unverified.

The Income Tax Department argued that supporting evidence, such as bank statements for payments, was not furnished, despite the demat statement being provided.

Lesson from the case

Filing the wrong ITR form or ignoring small losses can result in huge tax demands and penalties, creating unnecessary harassment.

CAclubindia

CAclubindia