Background:

As per the Board's Circular No.108/02/2009-ST, dated 29.01.2009, Services provided by the Builders/developers prior to 01st July 2010 were not taxable but after 01st July 2010 Construction services provided by the Builders/developers is taxable including the flats given to the land owner.

Applicability:

The Service tax is applicable on Under Construction Property (on the bookings/agreement made before construction completes) not for the completed contract. The reason for exclusion of completed construction from the purview of the service tax is that, there is no element of service relating to the construction after completion of construction which is held by the Karnataka high court in the case of Confederation of real estate developers association of India & ANR vs. UOI 2012-13. As it becomes transfer of title in immovable property and thereby not falling in the definition of service, hencewe discuss only consideration received partly or fully before issuance of completion-Certificate by the competent authority.

Exemption available:

1. A single residential unit otherwise than as a part of a residential complex.

2. Low- cost houses up to a carpet area of 60 square metres per house in a housing project approved by competent authority

3. Post-harvest storage infrastructure for agricultural produce including a cold storages for such purposes

4. Mechanised food grain handling system, machinery or equipment for units processing agricultural produce as food stuff excluding alcoholic beverages.

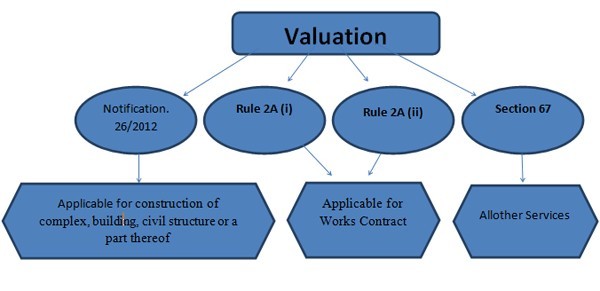

Valuation of Services under different methods.

There are four ways to determine the taxable value of the service provided by construction Industry.

Notes:

a. Rules mentioned above is under Service Tax (Determination of Value) Rules, 2006.

b. Condition for Notification 26/2012 valuation is that the value of land is included in the amount charged from the service receiver.

Let us take one example and will work on the all the methods.

XYZ Pvt Ltd. Construct and sold the building following are the amount received and cost incurred details:

Gross amount charged: Rs. 75,00,000

Cost of the land: Rs. 25,00,000

Material consumed: Rs. 15,00,000

Labour charges paid: Rs. 5,00,000

CENVAT credit on Input: Rs. 1,05,000

CENVAT Credit on Inputs services: Rs. 15,450

CENVAT Credit on Capital Goods: Rs. 2,250 (Assume total Rs.5,500,50% is already availed)

|

PARTICULARS |

Valuation Methods |

|||

|

Relevant Notification/Rule/ provision |

Notification 26/2012 |

Rule 2A (i) |

Rule 2A (ii) |

Section 67 |

|

Gross Amount Charged |

75, 00,000 |

75, 00,000 |

75, 00,000 |

75, 00,000 |

|

Less: - # Exemption of 75% |

56, 25,000 |

NIL |

NIL |

NIL |

|

Less: - Cost of Land |

NIL |

25, 00,000 |

25, 00,000 |

25, 00,000 |

|

Less: - Value of Material |

NIL |

15, 00,000 |

NIL |

NIL |

|

Taxable Value |

18, 75,000 |

35, 00,000 |

50, 00,000 |

50, 00,000 |

|

Service Tax thereon (12.36%) |

2, 31,750 |

4, 32,600 |

⃰ 2, 47,200 |

6, 18,000 |

|

Less: - CENVAT Credit on Input |

NIL |

NIL |

NIL |

1,05,000 |

|

Less: - CENVAT Credit on Input Services |

15,450 |

15,450 |

15,450 |

15,450 |

|

Less :- CENVAT Credit on Capital Goods |

2250 |

2250 |

2250 |

2250 |

|

Service Tax Payable |

2, 14,050 |

4, 14,900 |

2, 29,500 |

4, 95,300 |

Notes:

A. Valuation as per the Notification 26/2012 there are two types of scenario for determining the taxable amount

1. For residential unit having carpet area up to 2000 square feet or where the amount charged is less than rupees one crore then exemption is 75% (# this option is considered for the above example.

2. For other than the above exemption is 70%

B. Under Rule 2(ii) there are three categories of works on which different % of taxable services to be determined

1. In the Case of works contract entered into for execution of original works40% is taxable (⃰ this option is considered for the above example)

2. In case of works contract entered into for maintenance or repair or reconditioning or restoration or servicing of any goods is taxable at 70%

3. In case of other works contracts is taxable at 60%

Original works means:

(i) All new constructions;

(ii) All types of additions and alterations to abandoned or damaged structures on land that are required to make them workable;

(iii) Erection, commissioning or installation of plant, machinery or equipment or structures, whether pre-fabricated or otherwise;

Reverse charge under Rule 6(3) of CENVAT CREDIT Rules, 2004

Under the above rule the question of reversal of input services arises when the service provider or manufacturer of goods opting not to maintain separate accounts in respect of Exempted and taxable services/ Goods.

Now let us learn the rule 6(3) with the below Illustration:

Illustration: M/s Smart builder Pvt ltd sold the flat for Rs 75,00,000 and also constructed a single residential unit ( Negative list entry) for Rs 25,00,000, The company availed CENVAT Credit of Rs 8,50,000 in respect of aforesaid services, The Company opting not to maintain separate accounts for the above transaction what is the amount of Reversal of CENVAT credit?

Solution:

Option-1 Pay 6% on the exempted services Rs 25,00,000*6%= Rs 1,50,000

Option-2 Proportionate basis:(Value of exempted services/Value of taxable services+ Value of exempted services)* CENVAT credit Availed

(Rs 25,00,000/Rs 25,00,000+Rs 75,00,000)*Rs 8,50,000 = Rs 2,12,500

As per the above workings Option-1 is beneficial to service provider, hence he can choose the same for the reversal of CENVAT.

Point of Taxation

Point of taxation under Works Contract which qualifies as continuous supply of service (as per the Notification No 28/2011 ST) would arise as follows:

The tax liability arises based on the accomplishment of the stage of the work as specified in the contract or date of invoice as per the contract terms or the date on which money is received, whichever is earlier.

Important Issues in construction industry in respect of service tax.

Joint Development Agreement : (JDA)

JDA refers to a Scenario where the owner transfers his undivided interest in the land, against which the builder agrees to compensate the owner with a built up area.

This type of transactions are covered under the service tax net because under the service tax even the consideration received in kind also a consideration for the purpose of service tax.

Land cost:

The land cost is not subject to Service tax. However if the assessee opts to pay tax under option I i.e. as per the notification No 26/2012 then the land value must be included.

Deposits:

Collection of Statutory deposits like Electricity, water at actuals are not services they are just reimbursements. Hence no service tax on the same as per Rule 5(2) Of service tax determination of value Rules, 2006 is applicable.

By: Ravi Kumar

Email:ravikumar.rpng@gmail.com

CAclubindia

CAclubindia