Introduction: The Ministry of Finance had come out with General Anti Avoidance Agreement (GAAR) in this buget. But due to its opposition from many quarters especially the FII’s(Foreign Institutional Investors), Government formed a expert Committee to look in to the GAAR & make some changes to it. The Committee was headed by Dr Parthasarthi Shome. They reviewed the GAAR provisions & came up with suitable suggestions. The Government has incorporated the changes & has issued the new GAAR regulations. Here are some of the changes which are accepted by Government

GAAR is an advanced instrument of tax administration where an entity is taxed if he has made an arrangement of transaction mainly to avoid tax. Some assesses structure a transaction in such a way that maximum tax benefit is available using the existing tax law. Some of these result in Tax mitigation which is permitted. Some are artificial arrangement which result in Tax avoidance. So there must be a distinction between tax avoidance & Tax mitigation. GAAR is invoked if there is such an arrangement made specifically to avoid tax & not to mitigate tax.

GAAR is to be applied only if cases of abusive, Contrived & artificial arrangements. Arrangement is said to be impermissible if the main purpose is to obtain tax benefit & results in misuse of provisions of law, lacks commercial substance or is not entered for bonafide purposes.

Some examples of arrangements lacking commercial substance are:

1. the substance or effect of the arrangements a whole, is inconsistent with, or differs significantly from, the form of its individual steps or a part; or

2. Includes:

a. Round tripping

b. Accommodating party

c. Elements that have effect of offsetting or cancelling each other

d. A transaction which is conducted through one or more persons and disguises the value, location, source, ownership or control of funds which is the subject matter of such transaction

3. it involves the location of an asset or of a transaction or of the place of residence of any party which is without any substantial commercial purpose other than obtaining a tax benefit (but for the provisions of this Chapter) for a party.

Some of the examples of Tax mitigation are the following:

(i) Selection of one of the options offered in law.

For Example–

(a) payment of dividend or buy back of shares by a company

(b) setting up of a branch or subsidiary

(c) setting up of a unit in SEZ or any other place

(d) funding through debt or equity

(f) purchase or lease of a capital asset

(ii) Timing of a transaction, for instance, sale of property in loss while having profit in other transactions.

(iii) Amalgamations and demergers (as defined in the Act) as approved by the High Court.

(iv) Intra-group transactions (i.e. transactions between associated persons or enterprises) which may result in tax benefit to one

If GAAR is evoked then the assessee may be denied of tax benefit or a benefit under a tax treaty.

Some of the major changes made to GAAR on the recommendations of Shome Committee are as follows.

1. Implementation of GAAR is deferred for 3 years. It will be applicable from year A.Y 2016-17.

2. The definition of Connected Person will be the combined definition of Associated Enterprises u/s 92A & Associated person u/s 102.

3. Monetary Threshold limit of Rs 3 Crore will be applicable where the GAAR applies. So only if the Tax is above this limit then only the GAAR applies.

4. Where SAAR (Specific Anti Avoidance Agreement) is applicable then GAAR will not be evoked.

5. If an FII chooses not to avail the benefit of agreement u/s 90 & 90A & subjects himself to the domestic Tax laws , then the GAAR provision will not be applicable to such FII.

6. Where only a part of the arrangement is impermissible, the tax consequences of an impermissible avoidance arrangement – will be limited to that portion of the arrangement.

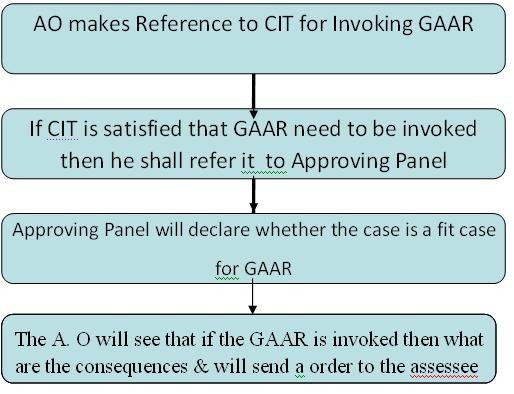

7. The assessing officer will be required to issue a show cause notice, containing reasons, to the assessee before invoking the provisions of Chapter X-A. The assessee shall have an opportunity to prove that the arrangement is not an impermissible avoidance arrangement.

8. The tax audit report may be amended to include reporting of tax avoidance schemes above a specific threshold of tax benefit of Rs. 3 crores or above.

9. The following statutory forms need to be prescribed:-

a. For the Assessing Officer to make a reference to the Commissioner u/s 144BA(1) (Annexe-8)

b. For the Commissioner to make a reference to the Approving Panel u/s 144BA(4) (Annexe-9)

c. For the Commissioner to return the reference to the Assessing Officer u/s 144BA(5) (Annexe-10)

10. Grandfathering of transaction: This is one of the important changes made to the GAAR provisions. Grandfathering of transaction means not to tax the existing investment & in the future. So if an FII is investing in a particular form & it is not permissible, then though It is impermissible arrangement, it would be accepted & GAAR will not be applicable to such investment in future also. It may be noted that such investment may be accepted but not arrangement. That is the arrangement may not be accepted or permitted, though the investment may be permitted.

So investments made before 30 August 2010 will be grandfathered. The Investments made after this date will be under taxed under GAAR.

11. Procedure for invoking GAAR

12. Constitution of Approving Panel: The Approving Panel will look after the procedural aspects of GAAR & how well it is implemented.

The Approving Panel shall consist of:

i. A Chairperson who is or has been a Judge of a High Court;

ii. One Member of the Indian Revenue Service not below the rank of Chief Commissioner of Income-tax; and one Member who shall be an academic or scholar having special knowledge of matters such as direct taxes, business accounts and international trade practices.

A decision of the AP should occur by a majority of members.

Conclusion: The Government has given some major reliefs to the FII’s who are investing in India by giving deferring the GAAR to 2016. This has led to rise in sensex to 20,000 mark, hope this ride wont stop & India continues to attract these FIIs

CAclubindia

CAclubindia