Notification No. 41/2012-Service Tax

29th June, 2012

This notification shall come into effect on the 1st day of July, 2012. It deals with the export of goods.

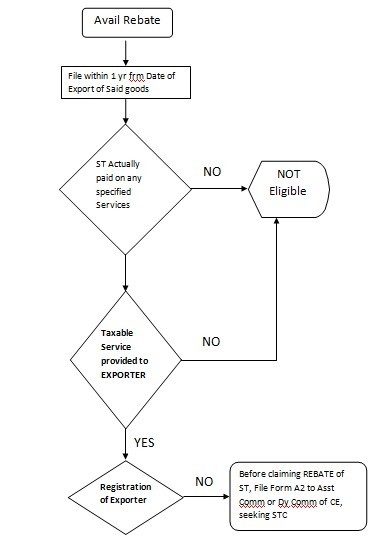

The Central Government grants rebate of service tax paid (hereinafter referred to as rebate) on the taxable services which are received by an exporter of goods (hereinafter referred to as the exporter) and used for export of goods, subject to the extent and manner specified as below :

Provided that:-

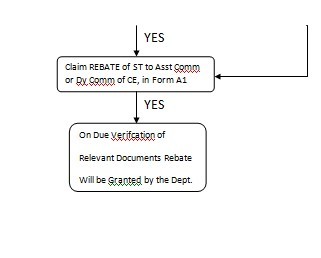

(a) The rebate shall be granted by way of refund of service tax paid on the specified services.

Explanation. — For the purposes of this notification,-

(A) “Specified services” means-

(i) In the case of excisable goods, taxable services that have been used beyond the place of removal, for the export of said goods;

(ii) In the case of goods other than (i) above, taxable services used for the export of said goods; but shall not include any service mentioned in sub-clauses (A), (B), (BA) and (C) of clause (l) of rule (2) of the CENVAT Credit Rules, 2004;

(B) “Place of removal” shall have the meaning assigned to it in section 4 of the Central Excise Act, 1944(1 of 1944);

(b) the rebate shall be claimed either on the basis of rates specified in the Schedule of rates annexed to this notification (hereinafter referred to as the Schedule), as per the procedure specified in paragraph 2 or on the basis of documents, as per the procedure specified in paragraph 3;

(c) the rebate under the procedure specified in paragraph 3 shall not be claimed wherever the difference between the amount of rebate under the procedure specified in paragraph 2 and paragraph 3 is less than twenty per cent of the rebate available under the procedure specified in paragraph 2;

(d) No CENVAT credit of service tax paid on the specified services used for export of goods has been taken under the CENVAT Credit Rules, 2004;

(e) The rebate shall not be claimed by a unit or developer of a Special Economic Zone;

(2) The rebate shall be claimed in the following manner, namely:-

(a) Who can claim ?

Manufacturer- Exporter registered or Unregistered Exporter under the Central Excise Act, 1944.

(b) Exporter who is not so registered under the provisions referred to in clause (a), shall register his service tax code number and bank account number with the customs;

(c) This clause refer to process of obtaining Service Tax Code by filling a declaration in Form A-2 to AC/Dy. Comm of Central Excise.

(d) The exporter shall make a declaration in the electronic shipping bill or bill of export, as the case may be, while presenting the same to the proper officer of customs, to the effect that—

(i) The rebate of service tax paid on the specified services is claimed as a percentage of the declared Free On Board (FOB) value of the said goods, on the basis of rate specified in the Schedule;

(ii) no further rebate shall be claimed in respect of the specified services, under procedure specified in paragraph 3 or in any other manner, including on the ground that the rebate obtained is less than the service tax paid on the specified services;

(iii) Conditions of the notification have been fulfilled;

(e) Rebate under this notification shall be calculated by applying the rate prescribed for goods of a class / description, as a percentage of the FOB value of the said goods.

(f) Amount so calculated will be deposited in the bank account of the exporter.

(g) shipping bill or bill of export on which rebate has been claimed on the basis of rate specified in the Schedule, by way of procedure specified in this paragraph, shall not be used for rebate claim on the basis of documents, specified in paragraph 3;

(h) Where the rebate involved in a shipping bill or bill of export is less than rupees fifty, the same shall not be allowed;

Rebate may be claimed in the following manner:-

CAclubindia

CAclubindia