Applicability: If the company has:

|

Net Worth of Rs. 500 crore |

In any of the closure of FY in 2013-14, 2012-13 & 2011-12 |

|

|

Turnover of Rs. 1000 crore |

||

|

Net Profit of Rs. 5 crore |

Then the company will have to spend 2% of its Average Profit Before Tax (earned in 2013-14, 2012-13 & 2011-12) in the year 2014-15

Even if the company has made a loss in the current year but the average PBT is > 5 crore then it has to carry out CSR activities.

Calculation of Profits for CSR:

|

Net Profit Before Tax (earned in India) |

XXX |

|

|

Less: |

Dividends Received from companies on whom Section 135 is applicable and are carrying out CSR Activities (i.e. 2% of Avg.PBT) |

(XX) |

|

Net Profit for CSR Activities |

XXX |

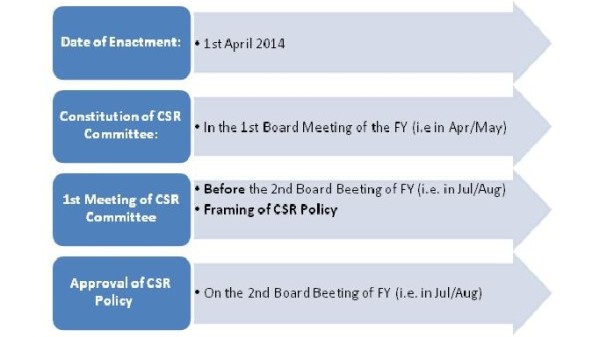

CSR Committee & Policy Timelines:

CSR in Cash or Kind?

- The company cannot provide its own goods and services in charity if it is engaged in selling such goods or services in its ordinary course of business.

- Therefore if a company gives its own products for charity then it cannot be counted as CSR Activities.

Can a company giving away used fixed assets for charity qualify as CSR?

- The company can give its used Fixed assets towards charity (office furniture/ desktops/laptops etc.) and it can be counted for CSR purpose only if VALUATION has been done on a Fair Value Basis.

- Companies may expend a maximum of 5% of its CSR expenditure in 1 FY towards Capacity Building measures, i.e. to build CSR capacities (training of persons to carry out CSR expenditure) of their own personnel as well as those of their Implementing agencies through Institutions with established track records.

CAclubindia

CAclubindia