Introduction

To close the loop on combating money laundering, the Ministry of Corporate Affairs (MCA) came up with the Companies (Significant Beneficial Ownership) Rules, 2019, which facilitates identification of the individuals who are holding ultimate beneficial interest in the companies.

The objective is to identify the ultimate beneficial individual or group of individuals who have control or ownership of the company disregarding the intermediate shareholding by non-individual persons.

Beneficial Interest

The concept of beneficial interest arises when a person is beneficiary of shares of the company but whose name is not entered in the Register of Members (RoM). In this scenario there are two types of interests that are identified, one is legal interest vested with the registered holders of the shares, who is also referred to as the 'registered or ostensible member'. Another is a beneficial interest vested with the beneficial owner or the beneficial member. One can conclude that, a beneficial interest is the right to receive benefits on shares held by another party.

One normally observed practice while incorporation of wholly-owned subsidiary companies is, subscribing the shares through a person or persons, who are generally in the employment of the company, who act as the nominee of the company to fulfill the criteria of minimum number of members. Upon incorporation, the company becomes a beneficial owner and nominee becomes a registered member of the subsidiary company.

By way of the Companies (Amendment) Act, 2017, in section (89) following subsection (10) was inserted which provides for meaning of the term 'beneficial interest':

'(10) For the purposes of this section and section 90, beneficial interest in a share includes, directly or indirectly, through any contract, arrangement or otherwise, the right or entitlement of a person alone or together with any other person to-

(i) exercise or cause to be exercised any or all of the rights attached to such share; or

(ii) receive or participate in any dividend or other distribution in respect of such share.'

Under this scenario the persons holding legal interest and beneficial interest have to submit the declaration to that effect in Form MGT 4 and MGT 5, respectively, and in turn the company has to submit form MGT 6 with the Registrar of Companies (RoC), within 30 days.

Significant Beneficial Owner

As per Section 90 of the Companies Act, 2013 ('Act'), Significant Beneficial Owner ('SBO') means,

'Every individual, who acting alone or together, or through one or more persons or trust, including a trust and persons resident outside India, holds beneficial interests, of not less than twenty-five per cent. or such other percentage as may be prescribed, in shares of a company or the right to exercise, or the actual exercising of significant influence or control as defined in clause (27) of section 2 of the Act'.

As per the definition provided in the Act, the Government is empowered to prescribe other holding percentage for the determination of the SBO. Accordingly, the Companies (Significant Beneficial Owners) Rules, 2019 ('SBO Rules') defines SBO as follows:

'Significant Beneficial Owner in relation to a reporting company means an individual referred to in sub-section (1) of section 90, who acting alone or, together, or through one or more persons or trust, who possesses one or more of the following rights or entitlements in such company, namely:-

• Holds indirectly, or together with any direct holdings, not less than ten percent of the shares;

• Holds indirectly, or together with any direct holdings, not less than ten percent of the voting rights in the shares;

• Has right to receive or participate in not less than ten percent of the total distributable dividend, or any other distribution, in a financial year through indirect holdings alone, or together with any direct holdings;

• Has right to exercise or actually exercises, directly or indirectly, significant influence or control, in any manner other than through direct holdings alone.'

Difference between 'Beneficial Interest' and SBO

The major difference between two concepts is that the beneficial interest holder may or may not be individual; however, SBO will always be an individual.

One normally observed practice of beneficial interest is, holding control in wholly-owned subsidiary companies through a person or persons who act as the nominee of the company to fulfill the criteria of minimum number of members.

The persons holding legal interest and beneficial interest have to submit the declaration to that effect in Form MGT 4 and MGT 5, respectively, and in turn the company has to submit form MGT 6 with the Registrar of Companies, within 30 days. The same was not the case with regards to SBO until the notification of the SBO Rules.

In case of beneficial/legal interest, the company has to file return with RoC only upon receipt of necessary declarations. However, in case of SBO, it is the collaborative exercise by both the Company and SBO.

Important Terms:

1. Control shall include the right to appoint majority of the directors or to control the management or policy decisions exercisable by a person or persons acting individually or in concert, directly or indirectly, including by virtue of their shareholding or management rights or shareholders agreements or voting agreements or in any other manner.

2. Reporting Company means a company incorporated under this Act or under any previous company law.

3. Majority Stake: Majority Stake means:

a) holding of more than 50% of the equity share capital in

the body corporate; or

b) holding of more than 50% of the voting rights in the body corporate; or

c) having the right to receive or participate in more than 50% of the

distributable dividend or any other distribution by the body corporate.

4. 'Significant Influence' means the power to participate, directly or indirectly, in the financial and operating policy decisions of the reporting company but is not control or joint control of those policies'.

5. 'Person Acting Together' (PAT): If any individual, or individuals acting through any person or trust, act with a:

•

common intent; or

• purpose of exercising any rights or entitlements; or

• exercising control; or

• significant influence,

over a reporting company, pursuant to an agreement or understanding, formal or informal, such individual, or individuals, acting through any person or trust, as the case may be, shall be deemed to be 'acting together'.

For determining PAT, the persons who form part of promoter and prompter group needs to be consider as 'persons acting together'.

6. 'Shares': As per the Rules, apart from the equity shares, the instruments in the form of Global Depository Receipts (GDR), Compulsorily Convertible Preference Shares (CCPS) or Compulsorily Convertible Debentures (CCD) shall also be treated as 'shares'.

It is pertinent to note that before arriving to percentage of holding, rights or entitlement, one have to work out the calculation for GDR, CCPS and CCD.

Relevance of Indirect Holding, Right and Entitlement

As per the definition it is evident that the individual should not be considered to be a SBO, if he does not have any holding, right or entitlement indirectly. Therefore, in order to be a SBO, a person must have an indirect holding, right or entitlement and where the individual has only direct holding, right or entitlement, he shall not be termed as SBO.

This is because, when individual hold shares, right or entitlement directly his identity is well disclosed to the company. Therefore, application of these rules is such cases will be of no use, as the provisions have been framed to identify the ultimate beneficial owners.

Determining 'Direct Holding'

An individual shall be considered to hold shares, right or entitlement directly in the reporting company if he satisfies any of the following criteria:

a) The shares in the reporting company representing such right or entitlement are held in the name of the individual. It means the name of individual who is holding shares, rights or entitlement is also entered in the Register of Members (RoM) of the company.

b) The individual holds or acquires a beneficial interest in the shares of the reporting company under sub-section (2) of section 89, and has made a declaration in this regard to the reporting company. It means the beneficial owner and the registered owner have already disclosed their respective interest to the Company in Form MGT 4 and MGT 5, respectively.

Identifying 'Indirect Holding'

An individual shall be considered to hold shares, right or entitlement indirectly in the reporting company, if he satisfies any of the following criteria:

1. Where the member of the reporting company is a body corporate (other than LLP)

SBO is the individual who

a)

holds majority stake in that member; or

b) holds majority stake in the ultimate holding company of that member;

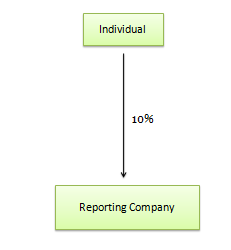

Illustration: 1)

In the given case, the Individual is not treated as SBO as there is no indirect shareholding in the Reporting Company.

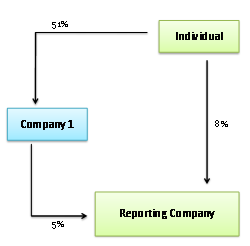

2)

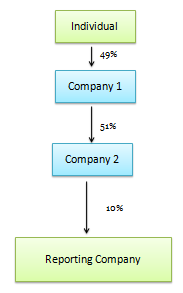

In the above case, the Individual's direct holding in the Reporting Company is 8%. Individual is also holding 5% through 'Company 1'. Individual's 5% holding in the Reporting Company through 'Company 1' shall be treated as Indirect Holding as the Individual is holding majority stake in Company 1. Accordingly, Individual will be treated as SBO for Reporting Company as his indirect holding together with direct holding is more than 10%.

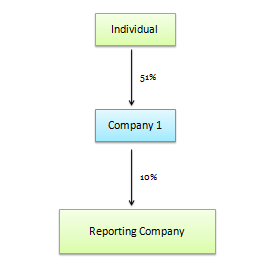

3)

In the above case, the Individual's direct holding in the Reporting Company is Nil. Individual is holding 10% through 'Company 1'. Individual's 10% holding in the Reporting Company through 'Company 1' shall be treated as Indirect Holding as the Individual is holding majority stake in 'Company 1'. Accordingly, Individual will be treated as SBO for Reporting Company.

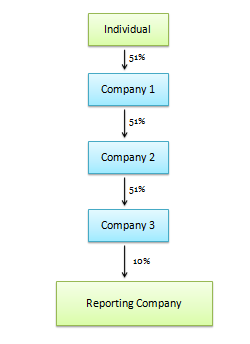

4)

In the above case, the Individual's direct holding in the Reporting Company is Nil. Individual is holding 10% through 'Company 3'. Individual's 10% holding in the Reporting Company through 'Company 3' shall be treated as Indirect Holding as the Individual is holding majority stake in the ultimate holding company i.e. 'Company 1'. Accordingly, Individual will be treated as SBO for Reporting Company.

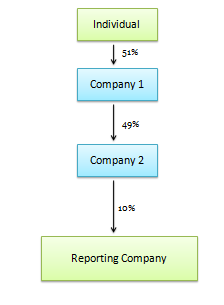

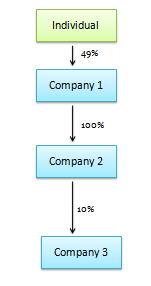

5)

In the above case, the Individual's direct holding in the Reporting Company is Nil. Individual is holding 10% through 'Company 2'. Individual's 10% holding in the Reporting Company through 'Company 2' shall not be treated as Indirect Holding as the 'Company 1' is not holding majority stake in 'Company 2'. Accordingly, Individual will not be treated as SBO for Reporting Company.

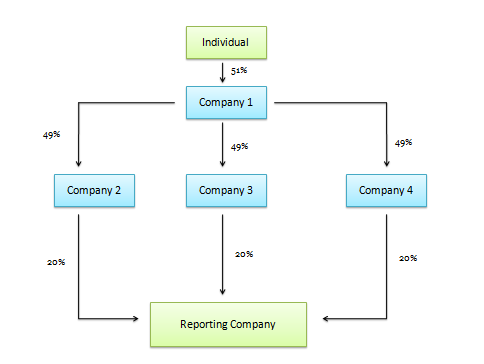

6)

In the above case, the Individual's direct holding in the Reporting Company is Nil. Individual is holding 60% through 'Company 2, 3 and 4'. Individual's 60% holding in the Reporting Company through 'Company 2, 3 and 4' shall not be treated as Indirect Holding as the 'Company 1' is not holding majority stake in the 'Company 2, 3 and 4'. Accordingly, Individual will not be treated as SBO for Reporting Company.

7)

In the above case, the Individual's direct holding in the Reporting Company is 10%. Individual is holding 5% through 'Company 2'. Individual's 5% holding in the Reporting Company through 'Company 2' shall not be treated as Indirect Holding as the 'Company 1' is not holding majority stake in the 'Company 2'. Accordingly, individual will not be treated as SBO for Reporting Company.

8)

In the above case, the Individual's direct holding in the Reporting Company is Nil. Individual is holding 10% through 'Company 2'. Individual's 10% holding in the Reporting Company through 'Company 2' shall not be treated as Indirect Holding as the Individual is not holding majority stake in the 'Company 1'. Accordingly, individual will not be treated as SBO for Reporting Company.

9)

In the above case, the Individuals' direct holding in the Reporting Company is Nil. Individuals' are holding 10% through 'Company 1'. Individuals' 10% holding in the Reporting Company through 'Company 1' shall be treated as Indirect Holding as the Individual 1, together with Individual 2 and 3, is holding majority stake in the 'Company 1', with common intent/ purpose of exercising control over the 'Company 1'. Accordingly, Individual 1 along with individual 2 and 3 will be treated as SBO for Reporting Company.

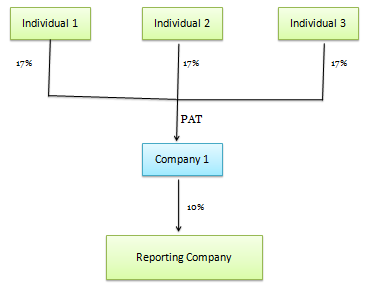

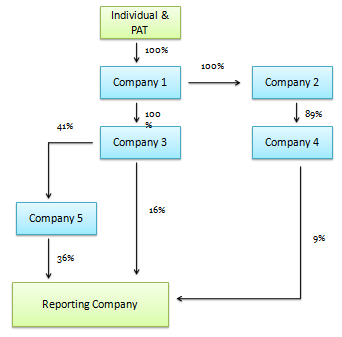

10)

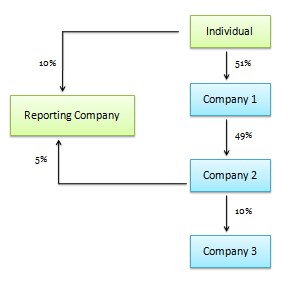

In the above case, the Individual & PAT's direct holding in the Reporting Company is Nil. Individual & PAT's are holding 61% through 'Company 3, 4 and 5'. Individual & PAT's 25% (16+9) holding in the Reporting Company through 'Company 3 and 4' shall be treated as Indirect Holding. As the 'Company 1' is holding majority stake in 'Company 3 and 4' and in turn Individual & PAT holds majority stake in 'Company 1'.

However, Individual & PAT's 36% holding in the Reporting Company through 'Company 5' shall not be treated as Indirect Holding. As the 'Company 3' is not holding majority stake in 'Company 5'.

2. Where the member of the reporting company is a Hindu Undivided Family (HUF) (through Karta)

SBO is the individual who is the Karta of the HUF

Illustration:

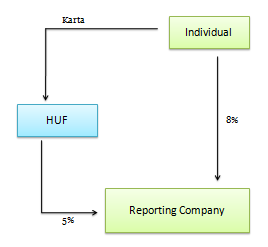

1)

In the above case, the Individual's direct holding in the Reporting Company is 8%. Individual is also holding 5% through 'HUF' of which he is Karta. Individual's 5% holding in the Reporting Company through HUF shall be treated as Indirect Holding as the Individual is Karta of HUF. Accordingly, individual will be treated as SBO for Reporting Company as his indirect holding together with direct holding is more than 10%.

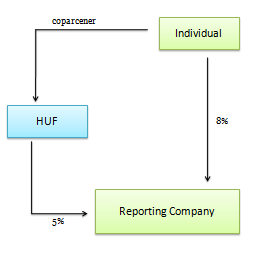

2)

In the above case, the Individual's direct holding in the Reporting Company is 8%. Individual is also holding 5% through 'HUF' of which he is coparcener. Individual's 5% holding in the Reporting Company through 'HUF' shall be treated as Indirect Holding as the Individual is Coparcener of 'HUF' and deemed to be acting together with Karta for common intent/ purpose. Accordingly, individual will be treated as SBO for Reporting Company as his indirect holding together with direct holding is more than 10%.

3. Where the member of the reporting company is a partnership entity (through partners)

SBO is the individual who

a) is a

partner; or

b) holds majority stake in the body corporate which is a partner of the

partnership entity; or

c) holds majority stake in the ultimate holding company of the body corporate

which is a partner of the partnership entity.

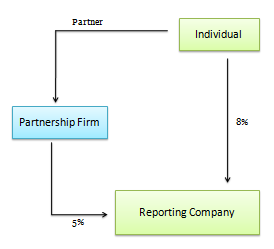

Illustration: 1)

In the above case, the Individual's direct holding in the Reporting Company is 8%. Individual is also holding 5% through 'Partnership Firm' of which he is Partner. Individual's 5% holding in the Reporting Company through 'Partnership Firm' shall be treated as Indirect Holding as the individual is Partner of 'Partnership Firm'. Accordingly, Individual will be treated as SBO for Reporting Company as his indirect holding together with direct holding is more than 10%.

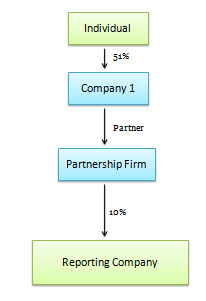

2)

In the above case, the individual's direct holding in the Reporting Company is Nil. Individual is holding 10% through 'Partnership Firm'. Individual's 10% holding in the Reporting Company through 'Partnership Firm' shall be treated as Indirect Holding as the Individual is holding majority stake in 'Company 1' which is Partner of 'Partnership Firm'. Accordingly, Individual will be treated as SBO for Reporting Company.

4. Where the member of the reporting company is a trust

SBO is the individual who

a) is a

trustee in case of a discretionary trust or a charitable trust;

b) is a beneficiary in case of a specific trust;

c) is the author or settler in case of a revocable trust

Illustration:

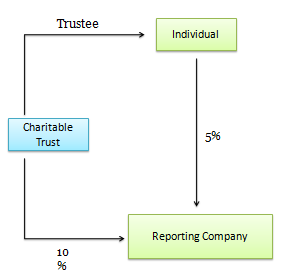

1)

In the above case, the Individual's direct holding in the Reporting Company is 5%. Individual is also holding 5% through 'Charitable Trust' of which he is Trustee. Individual's 10% holding in the Reporting Company through 'Charitable Trust' shall be treated as Indirect Holding as the Individual is Trustee of 'Charitable Trust'. Accordingly, Individual will be treated as SBO for Reporting Company as his indirect holding together with direct holding is more than 10%.

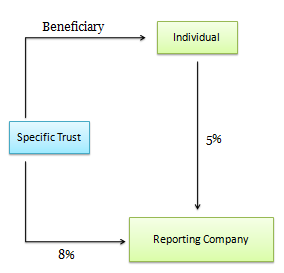

2)

In the above case, the Individual's direct holding in the Reporting Company is 5%. Individual is also holding 5% through 'Specific Trust' of which he is Beneficiary. Individual's 8% holding in the Reporting Company through 'Specific Trust' shall be treated as Indirect Holding as the Individual is Beneficiary of 'Specific Trust'. Accordingly, Individual will be treated as SBO for Reporting Company as his indirect holding together with direct holding is more than 10%.

5. Where the member of the reporting company is a Pooled Investment Vehicle or an entity controlled by the Pooled Investment Vehicle

SBO is the individual who

a) is a

general partner; or

b) is an investment manager; or

c) is a Chief Executive Officer where the investment manager of such pooled

vehicle is a body corporate or a partnership entity.

Declaration of beneficial interest by SBO

a) Initial Disclosure: Every individual who is holding Significant Beneficial Ownership in a reporting company is required to submit a declaration in Form BEN-1 to the reporting company within 90 days from February 8, 2019.

b) Continual Disclosure: Every individuals', who subsequently becomes Significant Beneficial Owner/ or where their significant beneficial ownership undergoes any change shall file a declaration in Form BEN-1 to the reporting company, within 30 days of acquiring such significant beneficial ownership or any change therein.

The SBO rules required submission of fresh disclosures and reporting, every time, when there is any change. At this point it is important to note that, disclosure will be required even for a minor change, which is detrimental to the Government's initiatives of ease of doing business and may set India back on world banks Doing Business Report.

Instead of any change MCA should specify some percentage like 2% change or any change which affects individual's status as SBO. The stakeholders are highly looking forward for necessary amendment to the rules in this regards.

Obligations of Reporting Company:

a) Identification of SBO: Every reporting company is required to take necessary steps to find out if there are any individuals' who are the SBO in relation to that reporting company, and if so, identify them and cause such individuals' to make a declaration in Form BEN-1.

Every reporting company should in all cases where its member, other than an individual, holds not less than 10% of its shares, voting rights or right to receive or participate in the dividend or any other distribution payable in a financial year, give notice to such member, seeking information in Form BEN- 4.

b) Return of SBO: The return of significant beneficial owners is required to be file by the reporting company with the RoC in Form BEN- 2 in respect of declaration received from SBO, within a period of thirty days from the date of receipt of such declaration.

c) Register of SBOs: Every company is required to maintain a register of SBOs in Form BEN- 3, which shall remain open for inspection by any member of the company.

Non Applicability

The rules are not applicable to the extent the shares of the reporting company are held by:

a) IEPF authority;

b) It's holding reporting company; however, the details of such holding

reporting company shall be reported in Form BEN-2;

c) The Central Government, State Government or any local Authority;

d) Reporting company; or a body corporate; or an entity, controlled by the

Government;

e) SEBI registered Investment Vehicles such as mutual funds, alternative

investment funds etc.;

f) Investment Vehicles regulated by Reserve Bank of India, or Insurance

Regulatory and Development Authority of India, or Pension Fund Regulatory and

Development Authority.

Illusion in case of subsidiary companies: as mentioned above, the conditional exemption is given for subsidiary companies to the extent of shares held by holding reporting company. However, for taking advantages of exemption, the subsidiary company is required to report the details of shares held by holding reporting company to the RoC in Form BEN 2.

After availing the exemption, the subsidiary company is neither required to seek information from its members in Form BEN 4 nor required to wait for receipt of disclosure in Form BEN 1. This would have been good news but it may not be useful for some subsidiary companies. This is evident from the following illustration.

In the above case, consider 'Company 2' as a Reporting Company. Take a scenario where 'Company 2' decides to take advantages of Non Applicability clause of SBO Rules. For taking advantages of non-applicability clause of the SBO Rules, 'Company 2' being subsidiary company of 'Company 1', required to file Form BEN- 2 with RoC reporting the holding of 'Company 1'.

Take other scenario where 'Company 2' decides to do the voluntary compliance of SBO Rules. While complying with the SBO rules voluntarily, one can find out that, the Individual is not holding majority stake in 'Company 1', which is holding company of 'Company 2'. Accordingly, individual will not be treated as SBO for 'Company 2' and there is no need to fie return of SBO with RoC.

In case of the second scenario, it is advisable, to do the voluntary compliances of SBO Rules and avoid filling of return of SBO in Form BEN-2.

Conclusion

It may be concluded that the SBO rules will ensure greater transparency in corporate world, as the mandate of the rules is to look through the entire maze of intermediate entities and identify the ultimate individual owners of the company.

However, there may be possibility of not having any SBO for any particular company. This can be extensively observed in case of listed entities, where promoters tend to exercise control over the listed entities by holding shares in between 26-49% through one or more intermediaries. This is possible because, large number of non-promoter shareholders generally do not show interest in controlling the management of the company.

The recent rules issued by MCA is amply cleared that all the individuals holding significant beneficial ownership have to declare their holding to the company and in turn the company to ROC. The requirements of these rules are ambitious step by MCA towards curbing the black money, which is used as an investment in equity through the shell companies, where the real owners hide behind a smokescreen. However, the success of such an initiative needs to be seen.

CAclubindia

CAclubindia