Income from house property is one of the five heads of income under which a taxpayer is required to compute and pay taxes. It includes rental income from property, deemed rent (if the property is not let out), and other related aspects.

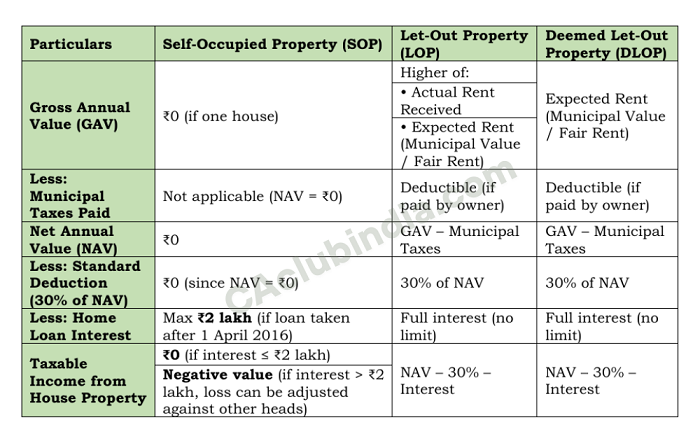

Types of House Property

- Self-Occupied Property (SOP) - Used for own residence.

- Let-Out Property (LOP) - Rented to others.

- Deemed Let-Out Property (DLOP) - More than one property (not rented out).

Calculation of Income from House Property

Here's how you can aim for zero tax on Rs 17 lakh rental income in FY 2025-26:

Opt for the New Tax Regime (Section 115BAC):

- The New Tax Regime for FY 2025-26 (AY 2026-27) has been revised to offer a higher tax-free limit.

- Under the new regime, income up to Rs 12 lakh can be effectively tax-free due to the increased rebate under Section 87A.

- More importantly for rental income, the new regime still allows for a standard deduction of 30% of the Net Annual Value (NAV) of your let-out property under Section 24(a).

Leverage the Standard Deduction (Section 24(a)):

This is the most crucial deduction for rental income. A flat 30% of your Net Annual Value (NAV) is allowed as a deduction, regardless of your actual expenses on repairs or maintenance.

Calculation

- Gross Annual Value (GAV) = Rs 17,00,000 (your total rental income)

- Less: Municipal Taxes paid (if any) - Let's assume for this example that municipal taxes are negligible or already accounted for in the Rs 17 lakh, or you can deduct them if you pay them.

- Net Annual Value (NAV) = GAV - Municipal Taxes

- Standard Deduction = 30% of NAV

If your gross rental income is Rs 17 lakh, applying the 30% standard deduction:

- Taxable rental income before other deductions = Rs 17,00,000 - (30% of Rs 17,00,000)

- Taxable rental income = Rs 17,00,000 - Rs 5,10,000 = Rs 11,90,000

Combine with the New Tax Regime's Tax Slabs and Rebate:

For FY 2025-26, the new tax regime has the following slabs:

- Up to 4,00,000: Nil

- Rs 4,00,001 - Rs 8,00,000: 5%

- Rs 8,00,001 - Rs 12,00,000: 10%

- Rs 12,00,001 - Rs 16,00,000: 15%

- Rs 16,00,001 - Rs 20,00,000: 20%

- Rs 20,00,001 - Rs 24,00,000: 15%

- Above Rs 24,00,000: 30%

The rebate under Section 87A in the new tax regime has been increased to Rs 60,000. This means if your total taxable income is up to Rs 12 lakh, your tax liability becomes zero.

Example:

| Gross Rental Income | Rs 17,00,000 |

| Less: Municipal Taxes | Rs 1,00,000 |

| Less: Standard Deduction (30%) | Rs 5,10,000 |

| Less: Home Loan Interest | Rs 2,00,000 |

| ess: 80EEA Deduction | Rs 1,50,000 |

| Taxable Rental Income | Rs 17,00,000 - Rs 1,00,000 - Rs 5,10,000 - Rs 2,00,000 - Rs 1,50,000 = Rs 7,40,000 |

With additional deductions like Section 80C (Rs 1.5 lakh), health insurance, NPS, etc., the taxable income can potentially be brought below Rs 5 lakh (where no tax is due under the new tax regime).

Points to be noted:

- This scenario is most suitable if primary income comes from rental earnings. However, if you have additional income sources—such as a salary, business profits, or other capital gains—that increase your total taxable income beyond Rs 12 lakh (after deductions), you will be taxed according to the new regime's slab rates.

- To benefit from the New Tax Regime, one must explicitly select it while filing your Income Tax Return. If you opt for the old regime instead, the tax calculations and deductions will differ, making it far more challenging to reduce your tax liability to zero on Rs 17 lakh. Under the old regime, you would need significant deductions under Sections 80C, 80D, and full home loan interest claims (for a let-out property) to achieve minimal or no tax.

- If one has additional sources of income, compare both tax regimes thoroughly. The new regime provides lower tax rates but restricts most deductions. On the other hand, the old regime allows more deductions (such as Section 80C, 80D, and full home loan interest for let-out properties) but imposes higher tax rates in certain income brackets. Choose the option that minimises your overall tax liability based on your income and eligible deductions.

CAclubindia

CAclubindia