GST Being a new baby in the in the India indirect taxation regime, the mistake can happen at any point of time due to various reasons like the non clarity of GST concept and legal provision even with good intention. Section 77 of the CGST Act, and Section 19 of the IGST Act deals with such kind of situation. It says that if the tax paid to the wrong government then the person is required to tax the tax to the concerned government and the amount paid to such wrong Govt is refunded to the concerned person. Below are the two relevant provision:

Section 77 of the CGST Act, (1) A registered person who has paid the Central tax and State tax or, as the case may be, the central tax and the Union territory tax on a transaction considered by him to be an intra-State supply, but which is subsequently held to be an inter-State supply, shall be refunded the amount of taxes so paid in such manner and subject to such conditions as may be prescribed.

(2) A registered person who has paid integrated tax on a transaction considered by him to be an inter-State supply, but which is subsequently held to be an intra-State supply, shall not be required to pay any interest on the amount of central tax and State tax or, as the case may be, the central tax and the Union territory tax payable.

Section 19 of the IGST Act, 19. (1) A registered person who has paid integrated tax on a supply considered by him to be an inter-State supply, but which is subsequently held to be an intra-State supply, shall be granted refund of the amount of integrated tax so paid in such manner and subject to such conditions as may be prescribed.

(2) A registered person who has paid central tax and State tax or Union territory tax, as the case may be, on a transaction considered by him to be an intra-State supply, but which is subsequently held to be an inter-State supply, shall not be required to pay any interest on the amount of integrated tax payable.

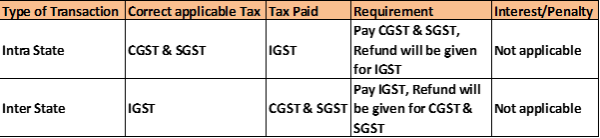

The above two provisions can be summarized in the following manner:

After reading and analyzing the above two provision of the CGST Act and IGST Act. Also, there is a parallel provision in the respective State and Union Act. It is quite clear that one wrong decision can have a big cash flow related provision. The problem goes deeper than the above summarized.

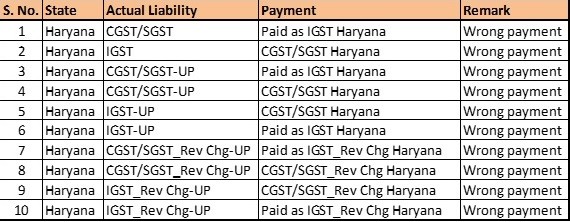

Let’s understand the same on the pretext of event Management Company, suppose an event management company is registered in the following states:

- Haryana

- Uttar Pradesh

Due to non-clarity of the GST provisions the output GST liability can be paid wrongly, below are the few instances of wrong payment:

However, there is no penalty and interest due to the above wrong payment.

Audit Aspect:

A company is subject to different types of audit, however, Statutory Audit, Internal Audit and now GST audit may be very common to the companies.

The above issue does not seem undiscoverable, once these are discovered they may carry the following adjustment:

- Wrong GST paid to be shown as refundable for the government; and

- GST not paid to be shown as payable to the government and required to be paid at the later stage.

CAclubindia

CAclubindia