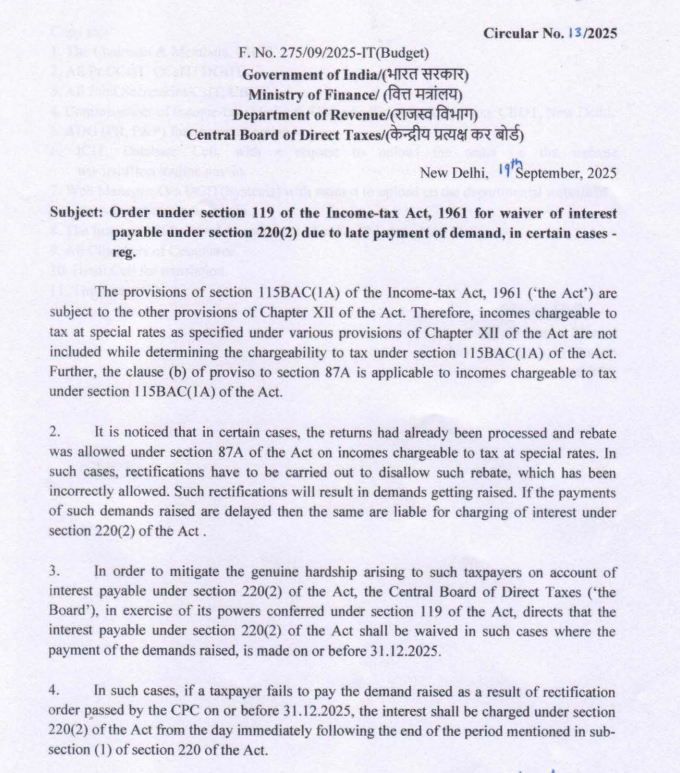

The Central Board of Direct Taxes has issued a circular by extending the deadline until December 31, 2025 for interest relief to taxpayers who were impacted due to errors while claiming Rebate u/s 87A in the new tax regime.

New Tax Regime and Rebate Issues

Section 115BAC(1A) of the Income Tax Act pertains to the New Tax Regime.

Many taxpayers, while filing ITR under the new tax regime, had claimed Rebate u/s 87A.

Within this regime, income is categorized into normal income and special rate income, such as capital gains, lottery winnings, short-term capital gains and long-term capital gains.

Here, Section 87A rebate amounting to Rs 25,000 is available to resident individuals whose total income is within 7 lakh under the new tax regime.

But, on 5th July 2024, the government updated the income tax utility and disallowed the rebate under Section 87A on special rate income.

Issue Faced by Taxpayers

Many taxpayers filed ITRs before 5th July 2024, the system wrongly gave the rebate u/s 87A even their income included special rate income.

Later, the IT department made rectification.

This created:

- Additional Tax Demand (because rebate was wrongly claimed).

- Interest Liability (for delayed payment after July 31, 2024).

Relief Announced by CBDT

Now taxpayers have time till 31st December 2025 to pay the additional demand.

If the additional tax arising due to 87A disallowance is paid before the deadline, no interest u/s 220(2) will be charged.

This waiver applies to demands for

- Assessment Year 2024-25

- Assessment Year 2025-26

Consequence of Non-Payment

If the demand is not paid within 31st December 2025, interest will be applicable from 30 days after the date the demand notice was issued, until the date of payment.

CAclubindia

CAclubindia