Republished with Amendments up to September 2018

Managerial Persons covered are Managing Director, Whole-time Director, Part time Directors and managers who shall be paid remuneration subject to and in accordance with provisions of Section 197 of the Companies Act, 2013. As compared to various sections and chapters viz section 198, 309, etc of Companies Act, 1956 which deals with Managerial remunerations separately, the new Act has solved this issue by consolidating all provisions under a single provision of 197.

Applicability of the Provisions of Section 196 to whom:

Section 196 deals with the appointment of Managerial Personnel and is applicable to private companies and public companies both while section 197 which deals with remuneration payable to managerial personnel is applicable to public companies only. Schedule V is partly applicable to private companies (i.e. in relation to Part I that deals with appointment) and partly not applicable to private companies (i.e. Part II that deals with remuneration)

DEFINITION AND COMPOSITION OF WORD MANAGERIAL REMUNERATION :

The managerial remuneration shall be payable to a person appointed within the meaning of section 196 of the Companies Act, 2013. Under the Companies Act, 2013 the provisions of payment of managerial remuneration are governed by Section 197, 198, 199 and Schedule V. The word remuneration is defined under section 2 (78) of Companies Act, 2013 which says that “remuneration”

means any money or its equivalent is given or passed to any person for services rendered by him and includes perquisites as defined under the Income Tax Act, 1961. Section 17(2) of Income Tax Act, 1961 has given an inclusive definition of the term “perquisite”. This clause comprises of eight sub-clauses followed by two provisos, and they deal with the following perquisites:

1. Value of rent-free accommodation provided to the assessee by his employer.

2. Value of any concession in respect of rent respecting any accommodation provided to the assessee by his employer.

3. The value of any benefit or amenity granted or provided free of cost or at a concessional rate to employee directors; or to employees who have a substantial interest and certain specified employees with some exceptions.

4. Sums paid by the employer in respect of any obligation which, but for such obligation, would have been payable by the assessee.

5. Sums payable by the employer to effect an assurance on the life of the assessee– employee or to effect a contract for an annuity.

6. W.E.F assessment year 2010-11, value of securities / sweat equity shares allotted or transferred by the employer or former employer to the employee.

7. W.E.F assessment year 2010-11 a contribution made by an employer to an approved superannuation fund to the extent it exceeds Rs 1 lakh.

8. Value of any other fringe benefit or amenity as may be prescribed.

9. The first proviso states that certain medical benefits are not treated as perquisites in certain specific situations.

Any expenditure incurred by the Company to affect any insurance on the life of, or to provide any pension, annuity or gratuity for, any of the persons aforesaid or spouse or child shall be included in managerial remuneration.

We can say that definition of remuneration, as well as perquisites, are inclusive in nature and hence it covers every amount that the company pays or spends for or for the benefit of a Director, in whatever form and by whatever name.

Moreover, any remuneration for services rendered by any such director which are of professional nature shall not be included in the managerial remuneration. Further, a director may receive remuneration by way of a fee for each meeting of the Board, or a committee thereof attended by him.

Where if insurance is taken by a company on behalf of its Key Managerial Personnel for indemnifying against any liability in respect of any negligence, default, misfeasance, breach of duty or breach of trust for which they may be guilty in relation to the company, the premium paid on such insurance shall not be treated as part of remuneration. But if such Key Managerial Personnel is found guilty then such insurance shall be treated as income part of remuneration.

If a manager or any director enjoys benefit or amenity without the company incurring any expenditure therefor, such benefit or amenity may not be included in the managerial remuneration.

An Independent director shall not be entitled to receive stock option. However, in the case of other directors, Stock options would be part of remuneration.

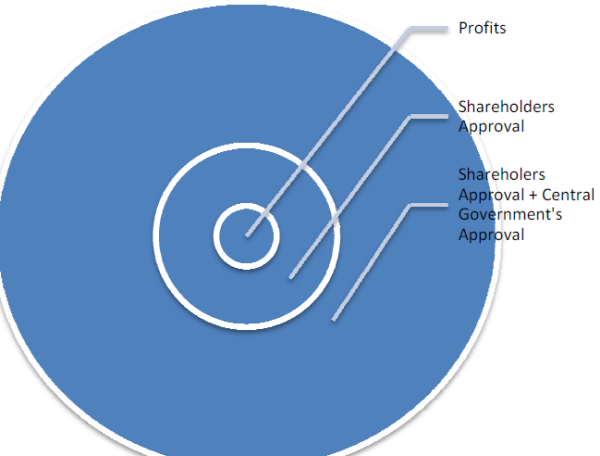

THREE WAYS TO MANAGERIAL REMUNERATION:

1. Automatic Route by Profits.

2. Shareholders’ Approval Route for more.

3. Shareholders’ and Central Government for even more.

REMUNERATION ALLOWED TO MANAGERIAL PERSON:

Section 197 of the Companies Act, 2013 provides a way to pay managerial remuneration in case of Company’s having adequate profits. A Public Company can pay remuneration to its directors including Managing Director s and Whole-time Directors, and its managers which shall not exceed 11% of the net profit as calculated in a manner laid down in section 198 of the Companies Act, 2013. Wherein a Company in which there is one Managing Director; Whole-time Director or manager the remuneration to be payable shall not exceed 5% of net profits and where there are more than one of such Directors remuneration payable shall not exceed 11 % of the net profit.

MAXIMUM REMUNERATION PAYABLE BY A COMPANY TO ITS MANAGERIAL PERSONNEL:

If a Company wants to pay remuneration in excess of the above limit payable then a Company shall have to follow Schedule V of the Companies Act, 2013.

Updated as on September 2018

Part II of Schedule V (earlier Schedule XIII) – Remuneration Payable by a company in case where is no profit or inadequacy of profit without central government is detailed below:

(A)

|

S.No

|

Where Effective Capital is

|

Limit of yearly remuneration payable shall not exceed (Rupees)

|

|

1

|

Negative or less than 5 crores

|

60 lacs

|

|

2

|

5 crores or above but less than 100 crores

|

84 lac

|

|

3

|

100 crores and above but less than 250 crores

|

120 lacs

|

|

4

|

250 crores and above

|

120 lacs plus .01% of the effective capital in excess of Rs.250 crores

|

The above limits shall be doubled if the resolution passed by the shareholders is a special resolution. That for a period less than one year, the limits shall be pro-rated.

(B) No approval is required if all the conditions are fulfilled:

A company with inadequate profit may pay to its managing director or whole-time director 200% of the above mentioned managerial remuneration if shareholders have given their approval through a special resolution.

Where the managerial person who is not holding Rs 5 lacs worth of shares or more or an employee or a director of the company not related to any director or promoter at any time during the two years prior to his appointment as a managerial person, In such cases, the company can pay to him up to maximum of 2.5% of the “current relevant profits” and up to 5% with the approval of shareholders by a special resolution.

For the purpose of this section, “current relevant profit” means profit calculated under section 198 but without deducting the excess of expenditure over income as defined in section 4(1) of section 198 relating to all usual working charges in respect of those years during which the managerial person was not an employee, director or shareholder of the company or its holding and subsidiary companies.

However, Section IV Part II of Schedule V states that a managerial person shall be eligible for the following perquisites which shall not be included in the computation of the ceiling on remuneration specified in Section II and Section III:—

(a) Contribution to provident fund, superannuation fund or annuity fund to the extent these either singly or put together are not taxable under the Income-tax Act, 1961 (43 of 1961);

(b) Gratuity payable at a rate not exceeding half a month’s salary for each completed year of service; and

(c) Encashment of leave at the end of the tenure.

Looking at clause (a) above, it is clear that any contribution made to provident fund, superannuation fund or annuity fund in excess of taxable limits under IT Act, 1961 shall not be included for the purpose of calculation of managerial remuneration in the event of inadequate profits or nil profits. The law herein clearly prescribes what value of perquisites shall not be considered as part of remuneration in cases of inadequate profits. Further, had the intent of law been to include only taxable amount of perquisites in the definition of ‘remuneration’ under section 2(78), then this clause would have been rendered meaningless. Thus, one can safely presume that where the intent was to specifically cover taxable value of perquisites law has been drafted clearly.

Therefore, to conclude, for the purpose of calculation of remuneration:

i. in the event of adequacy of profits – the entire value of perquisites as per IT Act, 1961 will have to be considered.

ii. in the event of inadequacy of profits of nil profits - only the taxable amount of perquisites should be considered. This is relevant only in case of managerial person.

While an expatriate managerial person shall be eligible for the following which shall not be considered in the definition of remuneration under Schedule V:

a) Children’s education allowance

b) Holiday package studying outside India or family staying outside India

c) Leave travel concession

If any of such directors receive any amount in excess of limits mentioned under the provisions of the Act, he shall refund such sums to the company and until such sum is refunded, hold it in trust for the company.

Further, if a Company wants to pay remuneration exceeding Schedule V of the Act then it shall require a Central Government approval.

Section 197 of the Company Act 2013 also does not bar a managing or whole-time director of a company to receive compensation from its holding company or subsidiary provided the same should be disclosed in the director’s report.

Meaning of Effective Capital:

For the purpose of Section 197 of Companies Act’ 2013, the term “Effective Capital” means:

• The aggregate of paid up share capital (excluding share application money pending allotment),

• Share premium,

• Reserves and Surplus excluding Revaluation Reserve,

• Long term loans and deposits repayable after one year, as reduced by –

• The aggregate of investments (except investments made by an investment company whose principal business is dealing in shares, stocks, debentures or any other securities),

• Accumulated losses, and

• Preliminary expenses not written off

This is also important to know as to when the effective capital should be calculated for the purpose of payment of managerial remuneration. In this regard, the following should be noted:

1. If the appointment of managerial person is made in the year in which the company is incorporated, then the effective capital should be calculated on the date of appointment of such managerial person.

2. In case other than above, the effective capital should be calculated on the last day of the Financial Year immediately preceding the Financial Year in which the appointment of managerial person is made.

PROFIT OR INADEQUATE PROFIT IN SPECIAL CIRCUMSTANCES –

In certain special circumstances, a company suffering from no profit or inadequate profit may pay managerial remuneration in excess of limits specified in Section II above and that too without the approval of Central Government. Those circumstances are specified below:

1. 1. The company paying managerial remuneration in excess of maximum specified limits is either a foreign company or a company who has got approval of its shareholders in this regard and the total managerial remuneration payable by such company is within the permissible limits of Section 197 of Companies Act’2013.

2. Where the company is:

• A newly incorporated company and is in existence for last seven years from the date of its incorporation, or

• A sick company in respect of which a scheme for revival and rehabilitation has been ordered by BIFR or NCLT for a period of five years from the date of sanction of revival scheme

• It may pay managerial remuneration up to two times of the amount specified in Section II, given above.

3. Where such excess managerial remuneration is fixed by BIFR or NCLT, subject to fulfilment of certain additional conditions apart from that given in Section 197 of Companies Act’2013

RESTRICTION ON INDEPENDENT DIRECTOR:

Section 197(5) of the Act 2013 specifically permits different fees to be paid to Independent Directors, there is no such enabling provision with respect to profit related commission. This means profit related commission may be paid uniformly to all non-executive directors. A company may pay such commission within the limit of 1% or 3% of the net profits, as the case may be. Further, Independent Directors cannot be granted stock options.

A company in or resident in India, to make payment in rupees to its non WTD who is resident outside India and is on visit to India for the company’s work and is entitled to payment of sitting fees or commission or remuneration, and travel expenses to and from and within India, in accordance with the provisions contained in the company’s MOA & AOA or in agreement entered into by it or in any resolution passed by the company in general meeting or by Board, provided the requirements of any law, rules, regulations, directions applicable for making such payments are duly complied with.

MINIMUM REMUNERATION IN CASE OF LOSSES DURING THE TENURE OF MANAGERIAL PERSONNEL:

According to Departmental Clarification regarding amendments made by the Companies (Amendment) Act, 1988 as revised w.e.f. 1993, the Approval of Central Government shall not be required in case of loss or inadequacy of profit during the tenure of Managerial Person were the appointment was made and minimum remuneration paid was strictly in accordance with Schedule XIII of the 1956 Act.

DEVALUATION AND MANAGERIAL REMUNERATION:

A non-resident Indian may occupy the position of managerial person in certain companies, it has been examined by foreign exchange, taxation, Company Law and other aspects and was accordingly decided as a matter of policy that, in case of devaluation of currency there was a need to compensate such non-resident managerial persons to maintain these remittances at the pre-devaluation level and such increase in remuneration is allowed even if the resultant increased remuneration exceeds the statutory limits imposed by the Companies Act.

REMUNERATION PAYABLE TO A MANAGERIAL PERSON IN TWO COMPANIES:

Subject to the provisions of sections I to IV, a managerial person shall draw remuneration from one or both companies, provided that the total remuneration drawn from the companies does not exceed the higher maximum limit admissible from any one of the companies of which he is a managerial person.

PENALTY CLAUSES:

If any person contravenes the provisions of section 197, he shall be punishable with fine which shall not be less than one lakh rupees and may extend to five lakhs rupees If a company or any officer of a company or any other person contravenes any of the provisions of this Act or the rules made thereunder, the company and every officer of the company who is in default or such other person shall be punishable with fine which may extend to ten thousand rupees, and where the contravention is continuing one, with a further fine which may extend to one thousand rupees for every day after the first during which the contravention continues.

Update till September 2018

CAclubindia

CAclubindia