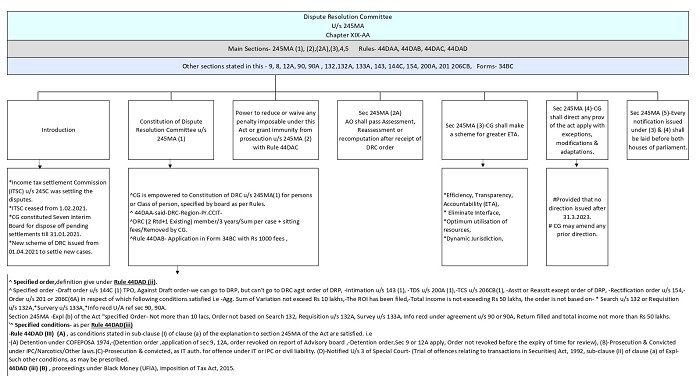

Introduction

The central government has constituted the Income-tax settlement commission for settlement of cases, which ceases to operate with effect from 1st of February, 2021. An applications was submitted under section 245C for settlement of cases to ITSC, on or after 1st February 2021 no application can be made. The central government In order to settle existing applications as on 31.01.2021, constituted seven interim boards for settlement vide notification No.91 of 2021 dated 10.08.2021. The pending cases/applications are being resolved or adjudicated through the interim board for settlement, it is also necessary to prevent tax disputes in future and settle the issues at initial stage. In its continuation, to provide early tax certainty to small and medium taxpayers , with effect from 1st April , 2021 new scheme of Dispute Resolution has been formulated for constitution of one or more Resolution Committee(s) (DRS). DRC focus mainly on small and medium taxpayers to resolve their tax disputes in a faceless, efficient, and taxpayer-friendly manner. DRC functions under Ministry of Finance, Government of India. 18 DRCs correspond exactly to the 18 Pr. CCIT regions; each is the designated electronic resolution body under Section 245MA. Taxpayers file Form 34BC via the Income Tax e‑filing portal, under the e‑DRS Scheme, 2022. Jurisdiction and contact details (including email addresses) for each DRC are accessible through the Income Tax Department portal.

Each of the 18 Pr. CCIT regions has an associated DRC. Here are the details

|

Pr. CCIT Region |

Headquarters |

States Covered |

Email (Form 34BC submission) |

|

1. Gujarat |

Ahmedabad |

Gujarat |

ahmedabad.dispute.rc1@incometax.gov.in en.wikipedia.org+13taxguru.in+13goodreturns.in+13taxconcept.net |

|

2. Karnataka & Goa |

Bengaluru |

Karnataka, Goa |

bengaluru.dispute.rc1@incometax.gov.in |

|

3. Madhya Pradesh & Chhattisgarh |

Bhopal |

MP, Chhattisgarh |

bhopal.dispute.rc1@incometax.gov.in |

|

4. Odisha |

Bhubaneswar |

Odisha |

bhubaneswar.dispute.rc1@incometax.gov.in |

|

5. North-West Region (Punjab, Haryana etc.) |

Chandigarh |

Punjab, Haryana, HP, JK & Ladakh, Uttarakhand |

chandigarh.dispute.rc1@incometax.gov.in |

|

6. Tamil Nadu & Puducherry |

Chennai |

TN, Puducherry |

chennai.dispute.rc1@incometax.gov.in |

|

7. Delhi |

Delhi |

Delhi |

delhi.dispute.rc1@incometax.gov.in |

|

8. North-East Region |

Guwahati |

NE States (Assam, etc.) |

guwahati.dispute.rc1@incometax.gov.in |

|

9. Andhra Pradesh & Telangana |

Hyderabad |

AP, Telangana |

hyderabad.dispute.rc1@incometax.gov.in |

|

10. Rajasthan |

Jaipur |

Rajasthan |

jaipur.dispute.rc1@incometax.gov.in |

|

11. UP (West) & Uttarakhand |

Kanpur |

West UP, Uttarakhand |

kanpur.dispute.rc1@incometax.gov.in |

|

12. Kerala |

Kochi |

Kerala |

kochi.dispute.rc1@incometax.gov.in |

|

13. West Bengal & Sikkim |

Kolkata |

West Bengal, Sikkim |

kolkata.dispute.rc1@incometax.gov.in |

|

14. UP (East) |

Lucknow |

East UP |

lucknow.dispute.rc1@incometax.gov.in |

|

15. Mumbai |

Mumbai |

Mumbai region |

mumbai.dispute.rc1@incometax.gov.in |

|

16. Nagpur |

Nagpur |

Maharashtra (Nagpur) |

nagpur.dispute.rc1@incometax.gov.in |

|

17. Bihar & Jharkhand |

Patna |

Bihar, Jharkhand |

patna.dispute.rc1@incometax.gov.in |

|

18. Pune |

Pune |

Maharashtra (Pune) |

pune.dispute.rc1@incometax.gov.in |

Additionally, there's a Pr. CCIT region for International Taxation based in Delhi and Bengaluru, covering international tax matters.

Click here to download: Dispute Resolution Committee u/s 245MA Chapter XIX-AA

Section 245MA

The sub-section (1) of section 245MA of income-tax Act, 1961 states that the central government shall constitute, one or more dispute resolution committees, as may be necessary i.e. it is upto the discretion of Central government that they shall constitute one or more committees, the committees shall be constituted in accordance with the rules made under this Act.

- The board will specify the persons or class of persons whose case will be resolved by the DRC.

- These persons or classes of persons who may opt for dispute resolution under this chapter in respect of dispute arising from any variation in the specified order in his case and who fulfils the specified conditions.

The sub-section (2) of section 245MA of the Act, states that the Dispute Resolution Committee, subject to such conditions, as may be prescribed, shall have the powers to reduce or waive any penalty imposable under the Income-tax Act, 1961 or grant immunity from the prosecution for any offence punishable under this Act in case of a person whose dispute is resolved under this chapter i.e. Chapter XIX-AA. Followed by Rule 44DAC.

Sub-section (2A) of section 245MA of the Act, Notwithstanding anything contained in section 144C, upon receipt of the order of the Dispute Resolution Committee under this section, the Assessing Officer shall, -

(a) In a case where the specified order is a draft of the proposed order of assessment under sub-section (1) of section 144C, pass an order of assessment , reassessment or re computation; or

(b) In any other case, modify the order of assessment , reassessment, or re computation,

In conformity with the directions contained in the order of the Dispute Resolution Committee within a period of one month from the end of the month in which such order is received.

An eligible assessee (being any person in whose case variation arises as a consequence of order of Transfer Pricing Officer (TPO) and any non-resident or a foreign company) may opt for approaching either the Dispute Resolution Panel under section 144C or the DRC under section 245MA. Accordingly, the A.O. shall pass the final order in conformity with the order by the DRC within a period of one month from the end of the month in which order is received.

Sub-section (3) of section 245MA- The Central government may make a scheme, by notification in the official gazette, for the purposes of dispute resolution under this chapter, so as to impart greater efficiency, transparency and accountability (ETA) by-

(a) Eliminating the interface between the Dispute Resolution Committee and the assesse in the course of dispute resolution proceedings to the extent technologically feasible;

(b) Optimizing utilisation of the resources through economies of scale and functional specialization;

(c) Introducing a dispute resolution system with dynamic jurisdiction.

Sub-section (4) of section 245MA- The central government may, for the purposes of giving effect to the scheme made under sub-section (3), by notification in the official gazette, direct that any of the provisions of this Act shall not apply or shall apply with such exceptions, modifications and adaptations as may be specified in the said notification.

Provided that no such direction shall be issued after the 31st day of March , 2023 :

[Provided further that the Central government may amend any direction, issued under this sub-section on or before the 31st day of March, 2023 , by notification in the official gazette]

Sub-section (5) of section 245MA- Every notification issued under sub-section (3) and (4) shall, as soon as may be after the notification is issued, be laid before each House of Parliament.

Now, let us discuss the explanation of "Specified order" & "Specified Conditions" given under section 245MA.

Explanation (b) for the purpose of Section 245MA of "Specified Orders"-

"Specified Orders" means such order, including draft order, as may be specified by the Board, and-

(i) Aggregate sum of variations proposed or made in such order does not exceed ten lakh rupees;

(ii) Such order is not based on search initiated under section 132 or requisition under section 132A in the case of assesse or any other person or survey under section 133A or information received under an agreement referred to in section 90 or section 90A;

(iii) Where return has been filed by the assesse for the assessment year relevant to such order, total income as per such return does not exceed fifty lakh rupees.

Explanation (a) for the purpose of Section 245MA of "Specified Conditions"-

"Specified conditions" in related to a person means a person who fulfils the following conditions, namely-

(I) Where he is not a person-

(A) In respect of whom an order of detention has been made under the provisions of the Conservation of Foreign Exchange and Prevention of Smuggling Activities Act, 1974 (52 of 1974);

Provided that-

(i) Such order of detention , being an order to which the provisions of section 9 or section 12A of the said Act do not apply, has been revoked on the report of the Advisory Board under section 8 of the said Act or before the receipt of the report of the Advisory Board; or

(ii) Such order of detention, being an order to which the provisions of section 9 of the said Act apply, has not been revoked before the expiry of the time for, or on the basis of, the review under sub-section (3) of section 9, or on the report of the Advisory Board under section 8, read with sub-section (2) of section 9 , of the said Act; or

(iii) Such order of detention, being an order to which the provisions of section 12A of the said Act apply, has not been revoked before the expiry of the time for, or on the basis of, the first review under sub-section (3) of the said section, or on the basis of the report of the Advisory Board under section 8, read with sub-section (6) of section 12A, of the said Act; or

(iv) Such order of detention has not been set aside by a court of competent jurisdiction;

(B) In respect of whom prosecution for any offence punishable under the provisions of the-

Indian Penal Code (45 of 1860) (Vide Notification No. S.O. 2790(E), dated 16-7-2024, now read as Act No. 45 of 2023) , Now IPC converted into BNS (Bhartiya Nyaya Sanhita),

- the Unlawful Activities (Prevention) Act, 1967 (37 of 1967),

- the Narcotic Drugs and Psychotropic Substances Act, 1985 (61 of 1985),

- the Prohibition of Benami Transactions Act, 1988 (45 of 1988),

- the Prevention of Corruption Act, 1988 (49 of 1988), or

- the Prevention of Money-Laundering Act, 2002 (15 of 2003)

has been instituted and he has been convicted of any offence punishable under any of those Acts;

(C) In respect of whom prosecution has been initiated by an income-tax authority for any offence punishable under the provisions of this Act or the Indian Penal Code (45 of 1860) (Vide Notification No. S.O. 2790(E), dated 16-7-2024, now read as Act No. 45 of 2023) , Now IPC converted into BNS (Bhartiya Nyaya Sanhita) or for the purpose of enforcement of any civil liability under any law for the time being in force, or such person has been convicted of any such offence consequent upon the prosecution initiated by an income-tax authority;

(D) Who is notified under section3 of the Special Court (Trial of Offences Relating to Transactions in Securities) Act, 1992 (27 of 1992);

(II) Such other conditions, as may be prescribed.

Constitution and composition of DRC [Rule 44DAA]: Part IX-AA

Rule [44DAA] (1)- The central government shall constitute a dispute resolution committee for every region of Principal Chief Commissioner of Income tax for dispute resolution, as provided under the chapter XIX-AA of the Act.

(2) Each dispute resolution committee shall consists of three members, as under-

(a) two members shall be retired officers from the Indian Revenue Services (Income-tax), who have held the post of Commissioner of Income tax or any equivalent or higher post for five years or more ; and

(b) one serving officer not below the rank of Principal Commissioner of Income tax or Commissioner of Income tax as specified by the Board.

(3) The member shall be appointed by the Central Government for a period of three years.

(4) The Central Government may fix a sum to be paid as fee to a member, who is retired officer, on a per case basis, along with a sitting fee, so decided by the board.

(5) The decision of the Dispute Resolution Committee shall be by Marjoity.

(6) The Central Government may, by recording reasons in writing and after giving an opportunity of being heard, remove any member from the Dispute Resolution Committee.

Application for resolution of dispute before the DRC [Rule 44DAB]

(1) Person shall make an application to the Dispute Resolution Committee, it shall be made in the Form No. 34BC., who opts for dispute resolution under section 245MA of the Act in respect of dispute arising from any variation in the specified order in his case and who fulfils the specified conditions.

(2) Person shall make an application along with the fee of one thousand rupees.

Rule 44DAC -Power to reduce or waive penalty imposable or grant immunity from prosecution or both under the Act

Sub-rule (1) -The Dispute Resolution Committee shall, upon receipt of intimation as per clause (xix) of sub-paragraph (1) of paragraph 4 of the e-Dispute Resolution Scheme, 2022, and subject to such conditions as it may think fiT to impose for the reasons to be recorded in writing, grant to the person who made the application for dispute resolution under section 245MA of the Act, waiver of penalty imposable or immunity from prosecution or both, in respect of the order which is the subject matter of resolution, if it is satisfied that such person has,-

(i) Paid the tax due on the returned income in full in available; and

(ii) Co-operated with the Dispute Resolution Committee in the proceedings before it.

Sub-rule (2) of Rule 44DAC- Notwithstanding anything contained in the sub-rule (1) , no immunity shall be granted by the DRC in a case where the proceedings for the prosecution for an offence have been initiated before the date of receipt of application, as referred to in clause (i) of sub-paragraph (1) of paragraph 4 of the e-dispute Resolution Scheme, 2022.

Sub-rule (3) of Rule 44DAC- An immunity granted to a person under sub-rule (1) shall stand withdrawn, if such person fails to comply with any of the conditions subject to which the immunity was granted and thereupon the provisions of the Act shall apply as if such immunity or waiver had never been granted.

Definitions for the purpose of this sub-chapter [Rule 44DAD]

Below are the sub-rules and clauses of Rule 44DAD has been stated-

(i) "Dispute Resolution Committee" means the Dispute Resolution Committee constituted under section 245MA of the Act;

(ii) The "specified orders" in related to a dispute under section 245MA of the Act means :

(a) A draft order as referred to in sub-section (1) of section 144C of the Act;

(b) An intimation under sub-section (1) of section 143 of the Act or sub-section (1) of section 200A of the Act or sub-section (1) of section 206CB of the Act, where the assesse or the deductor or the collector objects to the adjustments made in this said order-

(c) An order of assessment or reassessment, except an order passed in pursuance of directions of the Dispute Resolution Panel;

(d) An order made under section 154 of the Act having the effect of enhancing the assessment or reducing the loss; or

(e) An order made under section 201 of the Act or an order made under sub-section (6A) of section 206C of the Act and in respect of which the following conditions are satisfied, namely :-

(A) The aggregrate sum of variations proposed or made in such order does not exceed ten lakh rupees;

(B) The return has been furnished by the assesse for the assessment year relevant to such order and the total income as per such return does not exceed fifty lakh rupees; and

(C) The order in the case of the assesse is not based on,-

(I) Search initiated under section 132 of the Act or requisition made under section 132A of the Act in the case of the assesse or any other person; pr

(II) Survey carried out under section 133A of the Act; or

(III) Information received under an agreement referred to in section 90 or 90A of the Act.

Explanation- For the purposes of clause (e ) of sub-rule (ii) , the variation in the specified order relating to default in deduction or collection of tax at source, shall refer to the amount on which tax has not been deducted or collected in accordance with the Act.

(iii) The " specified conditions" in relation to a person who opts for dispute resolution under section 245MA of the Act, means a person in respect of whom :-

(A) The conditions mentioned in sub-clause (I) of clause (a) of the Explanation to section 245MA of the Act are satisfied;

(B) Proceeding under the Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act, 2015 (22 of 2015) have not been initiated for the assessment year for which resolution of dispute is sought.

(iv) The "specified person" for the purposes of section 245MA of the Act shall be a person who fulfils the specified conditions]

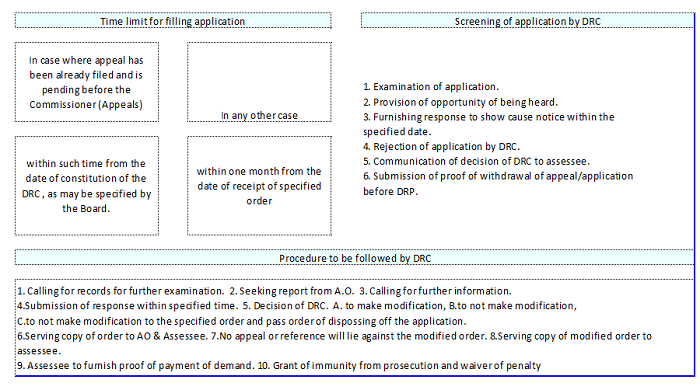

Time limit for filling the application

An application has to be filed -

- In cases where appeal has already been filed and is pending before the Commissioner (appeals) - Time limit is, within such time from the date of constitution of the Dispute Resolution Committee, as may be specified by the Board.

- In any other case- time limit is - within one month from the date of receipt of specified order.

Screening of application by DRC

(1) Examination of application- Step 1 is the DRC shall examine the application with respect to the specified conditions and criteria for specified order. After the examination of the application, where DRC is of the opinion that application should be rejected, DRC has to serve a notice calling upon the assesse to show cause as to why his application should not be rejected, specifying a date and time for filing a response.

(2) Provision of opportunity being heard- Now, assessee can request for an opportunity of being heard. If a DRC receives a request of being heard from the assesse, it has to provide him an opportunity of being heard through video telephony or video conferencing facility, to the extent technologically feasible.

(3) Furnishing response to show cause notice within the specified date- The assesse has to furnish a response to the show cause notice referred to in (i) above within specified time and date or such extended time as may be granted on the basis of the application made in this behalf, to the DRC.

(4) Rejection of Application by DRC- The DRC may, after considering the response furnished by the assessee, reject the application or proceed to decide the application on merits in accordance with the procedure laid out in (V) and (VI) hereinafter. Where no response has been submitted by the assessee, the DRC may reject the application.

Note - In such a case, the assesse may file an appeal to the Commissioner (Appeals). The period taken by the DRC in deciding on the admissions has to be excluded from the period available to file such appeal.

(5) Communication of decision of DRC to assessee - The decision of the DRC that the application for dispute resolution should be allowed to be proceeded with or rejected, has to be communicated to the assessee on his registered email address ;

(6) Submission of proof of withdrawal of appeal/application before DRP - Within 30 days of receipt of the communication that the application is admitted, the assessee is required to submit a proof of withdrawal of appeal filed under section 246A or withdrawal of application before the Dispute Resolution Panel (DRP), if any, to the DRC or convey that there is no aforesaid proceeding pending in his case. If the assessee fails to do so, the DRC may reject the application.

Procedure to be followed by the DRC

(i) Calling for records for further examination- Upon admission of the application and subsequent to the receipt of the response of the assessee , the DRC may call for records from the income-tax authority and further examine, as it may deem fit, with respect to the issues covered in the application.

(ii) Seeking report from Assessing officer - The DRC may seek a report from the Assessing officer on the issues covered in the application or on any other issue arising during the course of proceedings,

(iii) Calling for further information- The DRC may before disposing off the application, call for further information from the assessee or any other person by sending an email to his registered email address;

(iv) Submission of response within specified time- The assessee has to electronically submit its response to the DRC, within the time specified or such time as may be extended by the DRC on the basis of an application in this behalf.

(v) Decision of DRC- After considering the material available on record, including any further information or evidence received from the assessee. Income-tax authority or any other person, the DRC may decide-

(a) To make modifications to the variations in specified order, which are not prejudicial to the interest of the assessee, and decide for waiver of penalty and immunity from prosecution in accordance with the provisions of Rule 44DAC, and pass an order of resolution , accordingly; or

(b) to not make modifications to the variations in the specified order. However, the DRC may decide to waive penalty and grant immunity from prosecution provisions in accordance with the provisions of Rule 44DAC and pass an order of resolution accordingly. Such an order will be treated as an order not prejudicial to the interest of the assessee; or

(c) to not make any modification to the specified order and pass an order disposing off the application. Such an order will be treated as an order 'non prejudicial to the interest of the assessee'.

Within six months from the end of the month in which application for dispute resolution is admitted by the DRC. The order of the DRC for the resolution of a dispute has to be in accordance with the provisions of the Act.

(vi) Serving copy of order to AO and assessee - The DRC has to serve a copy of the order of resolution or order disposing off the application, as the case may be, upon the assessee and also the assessing officer for giving effect to the same, if so required.

(vii) No appeal or reference will lie against the modified order- Where the specified order is an order of the eligible assessee as referred to in section 144C(1), the assessee will not be eligible to file any reference to the DRP or an appeal to the Commissioner (Appeal) against the modified order.

(viii) Serving copy of modified order to assessee- The AO has to serve a copy of the modified order along with notice of demand upon the assessee specifying a date for making payment of demand. No appeal or revision would lie against the modified order.

(ix) Assessee to furnish proof of payment of demand- The assessee has to furnish proof of payment of the said demand to the DRC and also to the AO.

(x) Grant of immunity from prosecution and waive of penalty- The DRC shall, on receipt of confirmation of payment of demand, by an order in writing , grant immunity from prosecution and waiver of penalty if applicable, in accordance with the provisions of rule 44DAC.

Termination of dispute resolution proceedings- The DRC may, at any stage of the dispute resolution proceedings, if considered necessary, for reasons to be recorded in writing and after giving an opportunity of being heard to the assessee, decide to terminate the dispute resolution proceedings if-

(i) The assessee fails to co-operate during the course of dispute resolution proceedings ; or

(ii) The assessee fails to respond to , or submit any information in response to , a notice issued to him; or

(iii) The committee is satisfied that the assessee has concealed any particular material to the proceedings or has given false evidence.

(iv) The assessee fails to pay the demand as required in notice of demand.

Where the dispute resolution proceedings are terminated, the DRC has to intimate the income-tax authority for taking necessary action as per the provisions of the Act.

CAclubindia

CAclubindia