In the times of the increasing health care costs and a galore of health issues, a health cover has become the cushion for your health and finances. A health insurance premium may feel like a burden, but it will save you from the unexpected storm. Whenever there is a medical emergency, a health insurance offers you a helping hand by reducing your cash outflow.

Health insurance helps you fight against the rising medical costs, and provides an immediate resource in times of illness or an accident. Medical policies can be purchased based on the age of an individual, this is to ensure that the most suitable plan is provided to the applicant.

For example, personal health insurance plans from Apollo Munich Health Insurance offer extensive pre and post-hospitalisation coverage (60 Days before and 180 days after) as well as daily cash for hospital stay. Cash plans are usually top-up plans that can be purchased separately. Cash is payable under various conditions including, hospitalization, accident, ICU treatment, day care, etc.

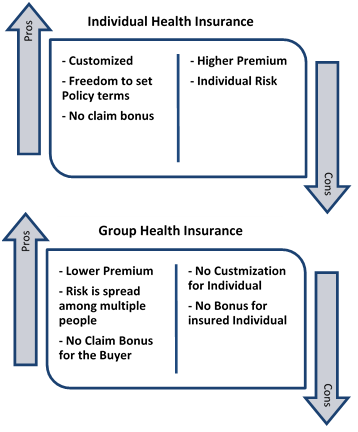

Such benefits help an individual get optimum coverage. In an individual health insurance, the applicant is insured individually and the sum assured is entirely and exclusively applicable to them. It is advisable for people to opt for personal health insurance even if there is a health benefit available through the employer. This cover may work as a bridge cover when you are losing group coverage and when you would like to add benefits that are not provided in the employer’s plan. Also, when your company’s health cover is not sufficient, your individual plan offers you the needed additional safety net.

When to Buy Individual Health Plan?

If you are in your twenties, your financial liabilities will be relatively limited, which makes it ideal to buy an individual health insurance. It makes a lot of sense to buy an individual health insurance that covers both pre and post hospitalization charges. It is also important to ensure that you take a plan that offers the benefit of a lifetime renewal feature which ensures that the policy will continue providing a cover for many years to come. Your policy purchased in the twenties will provide a cover even after retirement.

When to Buy Family Floater Health Plan?

Apart from the individual health insurance plan, there is a family floater health insurance plan. A family floater plan, covers health insurance for family members, for coverage of a fixed sum. This policy includes spouse and kids as well, and the fixed coverage can be shared among all the members.

It is relatively cheaper, depending on the age of the eldest insured member of the family, as compared to a personal health insurance and reduces the hassle of maintaining separate policies for every member of the family.

Family Floater vs. Individual Health Plan

A. Premiums

The total premium of an individual health plan (taken separately for each family member) would be higher since all the family members will have separate health covers and will need to pay their premium. Whereas, under a family floater plan, the same cover is available to the spouse and kids (assuming they are younger) which is why the premiums are reasonably lower.

B. Buying The Plans

For an individual health plan, you can buy separate plans for each member though the premium could be exorbitantly higher than a family floater plan. On the other hand, a family floater plan will apply to the buyer including the spouse and child. The plan excludes children above the age of 21 years.

In personal health insurance, the plan is separate for each individual, and it has no effect on the claim of other members on their specific plans. Whereas, a family floater plan is combined with the family and thus, the risk is shared by all. In the case of a claim, if you use a total coverage, you cannot claim for any other members of the family.

C. Shared Sum Insured

Both the policies serve the fundamental purpose of providing an insurance cover to the insured. In an individual plan, each individual has a specific sum insured, whereas, in a family floater plan, the same sum insured is shared by all insured family members. Both the options have pros and cons which need to be weighed before choosing the policy. The most useful and suitable policy should be selected for obtaining the best benefits.

CAclubindia

CAclubindia