INDIRECT TAX BENEFITS (excise duty in particular) ON DIRECT SUPPLIES TO SEZs made by a Vendor who is a sub-contractor of the Main Contractor

In relation to the subject matter, the mechanics of the transaction may be as under;

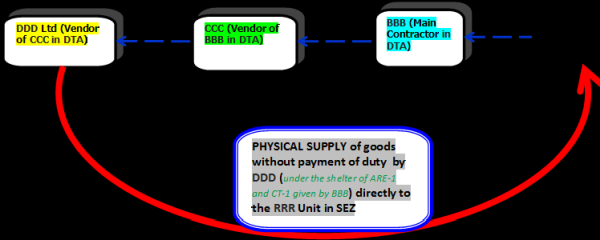

The customer is RRR Ltd., (a SEZ unit in Jamnagar SEZ … hereinafter ‘RRR-SEZ Unit’) who has placed order for procurement of goods from BBB (a unit in DTA). And in-turn BBB has placed an order on CCC Ltd (a unit in DTA).

The scope of CCC comprises of;

a) items that are manufactured by CCC in its factory at say ‘Vadodara’. That such manufactured items shall be dispatched by CCC under its excise invoice without payment of duty under the cover of Form ARE-1 read with Form CT-1 given by BBB). The excise invoice of CCC shall state the buyer as BBB and the consignee as RRR Unit in SEZ, Jamnagar. In the process, BBB ensures to get the necessary endorsement in Form ARE-1 by the specified officer in SEZ Unit and shall arrange to submit the same towards proof of export to its excise authorities within 45 days to help discharge their liability of excise duty under the CT-1 / Bond. And BBB shall also arrange to send an acknowledged copy of the proof of export to us (i.e., CCC) for our record purposes pls.

OUR COMMENTS: It is opined that this procedure is very much in line with the requirements of the Law of the land.

b) items that are bought-outs for CCC. And for this CCC places order on a Vendor (DDD) in Vadodara. That such manufactured items shall be dispatched by DDD under its excise invoice without payment of duty under the cover of Form ARE-1 read with Form CT-1 given by BBB. The excise invoice of DDD shall state the buyer as CCC and the consignee as RRR Unit in SEZ, Jamnagar. In the process, BBB ensures to get the necessary endorsement in Form ARE-1 by the specified officer in SEZ Unit and shall arrange to submit the same towards proof of export to its excise authorities within 45 days to help discharge their liability of excise duty under the CT-1 / Bond. And BBB shall also arrange to send an acknowledged copy of the proof of export to the Vendor (i.e., DDD) for their record purposes pls.

OUR COMMENTS: In principle, it is opined that this procedure is grossly in line with the requirements of the Law of the Land. However, the Vendor DDD may refuse to remove goods without payment of excise duty. In this regards DDD may take the plea of Rule 27 of the SEZ Rules which states that excise duty exemption as allowed to a SEZ UNIT is available to the Main Contractor appointed by such Unit. The said rule is silent as to the duty exemption available to the sub-contractors. DDD for this matter, compares the said Rule 27 with Rule 10 of the SEZ Rules, wherein Rule 10 of the SEZ Rules specifically mentions that excise duty exemption as allowed to a Developer or Co-developer is also available to the Contractors including sub-contractors appointed by such Developer or Co- Developer. Therefore, in lieu of the relevancy of said Rule 27 for dispatches to a UNIT in SEZ, the Vendor DDD opines CCC acts in the capacity of sub-contractor and therefore the duty exemption is not available and hence refuses to dispatch the goods from its factory under excise invoice without payment be it under the shelter of Form ARE-1 read with Form CT-1 to be given by BBB.

o The First reaction- that really whether CCC / DDD … units in DTA have to refer to the SEZ Rules!! Invariably, the provisions in Rule 19 of Central Excise Rules themselves are sufficient and complying the same would serve the very purpose.

o The contention- Even if CCC / DDD … units in DTA, also need to refer to the SEZ Rules … then also it is stated that the Vendor DDD can tread with the provisions enumerated in Rule 19 of Central Excise Rules and dispatch goods directly from its factory to RRR-SEZ Unit under their excise invoice without payment under the cover of Form ARE-1 read with Form CT-1 to be given by BBB. And given the fact that BBB ensures to get the necessary endorsement in Form ARE-1 by the specified officer in SEZ Unit and shall arrange to submit the same towards proof of export to its excise authorities within 45 days to help discharge the liability of excise duty under the CT-1 / Bond and BBB shall also arrange to send an acknowledged copy of such proof of export to the Vendor DDD for their record purposes pls.

Query: that whether the Vendor DDD can dispatch goods from its factory (directly to RRR-Unit in SEZ) under its excise invoice without payment under the cover of Form ARE-1 read with Form CT-1 to be given by BBB (i.e., Rule 19 of the CER read with Notn. No. 42/2001-CE dtd 26.6.2001) … wherein DDD excise invoice shows the buyer as ‘CCC and the consignee as the ‘RRR UNIT in SEZ’.

In this context, a brief analysis of the referred SEZ Rules is made to help clear the mist.

INDIRECT TAX BENEFITS (excise duty in particular) ON SUPPLIES TO SEZs – CONTRACTOR’S / SUB-CONTRACTOR'S PERSPECTIVE

The Scheme providing benefits

Under Section 26, every Developer and Unit is entitled to the following exemptions, drawback and concessions, namely;

· Exemption from customs duty on goods imported into the SEZ

· Exemption from any duty of excise on goods brought from the DTA to the SEZ

· Exemption from service tax on taxable services provided to the SEZ

· Exemption from tax on sale/purchase of goods under the CST Act, etc

Consequently, up-front, a Contractor is eligible for the following benefits;

· If the Contractor is a OEM, it is exempt from Excise duty

· If the Contractor is a seller, it is exempt from CST on its output sale

· If the Contractor is a service provider, it is exempt from its output Service tax

The controversy in the Scheme

IInd Proviso to Rule 10 of the SEZ rules provides as follows

“Provided further that exemptions, drawbacks and concessions on the goods and services allowed to a Developer or Co- Developer as the case may be shall also be available to the contractors including sub-contractors appointed by such Developer or Co- Developer and all the documents in such cases shall bear the name of the Developer or Co Developer along with the contractor and these shall be filed jointly in the name of the Developer or Co-Developer and the contractor”

In addition, Provision to Rule 27(1) of the SEZ rules provides as follows

“exemptions from payment of duty, taxes or cess, drawbacks and concessions on all types of goods and services, required for setting up and maintenance of the factory building, allowed to a Unit shall also be available to the contractors appointed by such Unit and all the documents in such cases shall bear the name of the Unit along with the contractor and these shall be filed jointly in the name of the Unit and the contractor”

These two Rules, would imply that whether the benefits that are accorded to a Contractor on its Revenue side (i.e., on supplies made to the SEZ) would also be available to the Subcontractors of such Contactors as well !!!

If the above principle were to hold well, it would essentially mean that à Exemptions from any duty of excise on goods manufactured by an OEM is also available to a sub-contractor of the Main Contractor appointed by the SEZ Unit/Developer

By going up-front thru’ the said rules (i.e., Rule 10 & Rule 27), a conclusion can be drawn that the said Rules (Rule 27 in particular) restricts the exemptions being provided/extended to a sub-contractor, even though the SEZ Act (Section 26) seldom envisage any such restrictions.

Therefore, the moot question is “Can the Rules travel beyond the Act”

If they cannot, then the duty exemption benefits as restricted under the Rules (Rule 27) on the output taxes (herein excise duty) of the sub-contractor would otherwise be available

The finer point – “Can the Rules travel beyond the Act”, has been examined in the following paras …

It is an established principle that the Rules cannot travel beyond the Act. Some of the judicial decisions endorsing this view have been enumerated below;

• The basis of the statutory power conferred by the Statute cannot be transgressed by the rule making authority. The rule making authority has no plenary power. It has to act within the limits of the power granted to it (Bimal Chandra Banerjee v. State of Madhya Pradesh — AIR 1971 SC 517)

• The Rules, therefore, cannot be so framed which do not carry out the purpose of the chapter and cannot be in conflict with the same (Laghu Udyog Bharti v. UOI — 2006 (2) STR 276 – SC)

• Delegated legislation must be read in the context of the primary/legislative Act and not the vice-versa - In case of a conflict between a substantive provision of an Act and delegated legislation, the former shall prevail” (ITW Signode India Ltd. v. Collector of central excise 2003 (158) E.L.T. 403 (S.C.)

Accordingly, Rule 10 & Rule 27, cannot travel beyond the SEZ Act, in as much as

• It cannot grant / restrict the benefit beyond that which has been contemplated under the SEZ Act

• Thus, it may so appears that Rule 10 / Rule 27 are ultra virus the SEZ Act and hence not valid

• In short, sub-contractors would also be eligible to any output tax exemptions, similar to that which is available to the Main Contactors on their output taxes

Section 51 of the SEZ Act have an overriding effect … which provides that “The provisions of this Act shall have effect notwithstanding anything inconsistent therewith contained in any other law for the time being in force or in any instrument having effect by virtue of any law other than this Act.”

Basis the above, the following can be argued that

• That the SEZ Act overrides all other law

• And that goods brought/consigned from the DTA into the SEZ (be it directly from the Main Contractors or from sub-contractors of Main Contractor) are exempt from excise duty and hence such excise duty exemption is available to the Main Contractor and to the sub-contractor of the Main Contractor as well.

Availability of exemptions to supplies of Main Contractor (OEM)

Supplies by manufacturers who are the Main Contractors to the Unit/Developer would not be liable to excise duty. And to avail this benefit, the Main Contactor must supply the goods directly to the SEZ Unit/Developer

Availability of exemptions to supplies of vendors (OEM) appointed by the Main Contractor

Since Section 26(1)(c) provides exemption to “goods brought from the DTA”, if the vendor (OEM) sells the goods to the Main Contractor but ships / consigns the goods directly to the SEZ, the exemption from excise should be available to such Vendor as well

That is to say, regardless of validity of Rule 10 & 27, the vendor (OEM) who is a sub-contractor can claim the benefit of excise duty exemption.

However, if the vendor (OEM) ships the goods to the Main Contactor, who after taking delivery of the goods ship the same to the SEZ Unit/Developer, then the exemption to the vendor of excise duty is likely to the denied

Important to note that the denial of excise duty exemption to the Vendor (OEM) would apply regardless of the fact that Rule 10 & 27 may be construed to be valid. The reasoning being;

Unlike physical export, where under the CT1 procedure contemplated under Notification 42/2001, the merchant exporter can procure goods without payment of excise duty (or under a claim of rebate) and therefore physically export the goods, this procedure has not been envisaged in the SEZ Act/Rules

Instead, the SEZ Act contemplates exemptions of excise duty only on ‘goods brought from the DTA to the SEZ’

In other words, the goods should be brought from the factory of the vendor (OEM) to the SEZ without the physical intervention of the Main Contractor

Further RULE 30 of the SEZ Rules, 2006 è prescribes the procedure for procurements of goods by a UNIT or Developer from the Domestic Tariff Area (DTA).

DTA Supplier supplying goods (note 1) to a Unit or Developer shall clear the goods, as in the case of exports, either under bond or as duty paid goods under claim of rebate on the cover of ARE-1 referred to in notn no. 42/2001-CE dtd 26th June 2001 (… as amended) in quintuplicate bearing running serial number beginning from the first day of the financial year.

Note 1- that the words used herein above are ‘supplying’ and not ‘selling’. Hence, supplies of goods from DTA unit (herein DDD) to the unit in SEZ unit (herein RRR-Unit in SEZ) shall qualify for excise duty exemption under said Rule 30 of the SEZ Rules, 2006 read with Rule 19 of the CER and notification no. 42/2001-CE dtd 26th June 2001 … as amended

CONCLUSION:

In this regard, it can be concluded that DDD can supply goods directly to RRR Unit in SEZ without payment of duty under bond provided DDD follows the procedure laid down in the Rule 30 of the SEZ Rules,2006. Rule 30 of the SEZ Rules provides the procedure for procurement of goods from the Domestic Tariff Area (hereinafter referred to as ‘DTA’). The said rule provides that the DTA supplier supplying goods to a SEZ Unit shall clear the goods, as in case of exports, either under bond or duty paid goods under the claim of rebate on the cover of ARE-1. Further, the said rule also provides the procedure to be followed by the SEZ unit while procuring the goods from the DTA Suppliers. Thus, from the above said Rule it is clear that the DTA Supplier has to clear the goods under the cover of ARE-1 to the SEZ Unit as if the same is exported either without payment of duty under Bond or on payment of duty under the claim of rebate.

Therefore, in the present case, we are of view that DDD being a DTA Supplier can clear the goods directly to RRR Unit in SEZ without payment of duty under bond under the cover of ARE-1. Further, with respect to the fact that DDD is the sub-contractor of the sub-contractor of the RRR, it is stated that the said fact would not make any difference as long as the goods are directly cleared from the factory of DDD by following the procedure laid down in the Excise Laws with respect to removal of goods without payment of duty under bond for the purpose of export and the procedure laid down in the Rule 30 of the SEZ Rules.

CAclubindia

CAclubindia