Objective of the Pull-out: -The Objective of the Pull-out is to address both Exporters and Importers in India having Forecasted Foreign Currency Receivables and Payables in their books and requisite hedging of the same using either Rolling 12 months Forwards Contracts or OTMF (Out of the Money Forwards) Options Contracts (Buy Put Contracts, Buy Call Contracts)

Editorial Desk of the Magazine” THE MAVERICK TREASURER” kept the definition of OTMF is when you are keeping the Strike Rate of the Options Contracts at 1 Implied Volatility away in case of Buy Put Contracts or1.5 Implied Volatility away in case of Buy Call Contracts. The purpose of taking OTMF is to make sure that both Buy Put and Buy Call Contracts come up low premiums to pay and subsequent FX line item in the books of Exporters and Importers.

Buy Put is an Options Derivatives Contracts where by an Exporter having the right to sell his Foreign Currency Receivables at an agreed rate with the bank while Buy Call is an Options Contracts where by Importer is having right to buy from Bank at an agreed rate. Net Settlement of both Buy Put and Buy Call along with other Options Derivatives is done at Tokyo Cut which is published at 1130 AM IST or 3.30 PM Tokyo Timings.

In case of Options Contracts agreed rate is known as Moneyness of the Options Contracts which is in the hands of Corporate Treasurer, Banker or Trader. Moneyness of the Options Contracts is further divided into three parts – ATMF (At the Money Forward), OTMF (Out of the Money Forward), ITMF (In the Money Forwards). Well OTMF and ITMF is further divided into 2 parts which is D-OTMF (Deep Out of the money forward)and D-ITMF (Deep In the money forward). Strike Rates of Deep in the Money Forward would be 2 Implied Volatility away from the respective Outrights Rates.

Moneyness for Buy Put Contracts (Exporter Contracts):-

|

Options Moneyness |

Counterparty |

Formula |

|

ATMF ( At the Money Forward) |

Exporter ( IV is Implied Volatility) |

Spot + Premiums |

|

OTMF ( Out of the Money Forward) |

OTMF= ATMF- 1IV |

|

|

ITMF ( In the Money Forward) |

ITMF = OTMF +1 IV |

|

|

D-OTMF ( Deep Out of the Money Forward) |

DOTMF = OTMF -1 IV |

|

|

D-ITMF (Deep In the Money Forward) |

DITMF= ITMF+ 1IV |

Moneyness for Buy CallContracts (Importer Contracts):-

|

Options Moneyness |

Counterparty |

Formula |

|

ATMF ( At the Money Forward) |

Importer ( IV is Implied Volatility) |

Spot + Premiums |

|

OTMF ( Out of the Money Forward) |

OTMF= ATMF+ 1IV |

|

|

ITMF ( In the Money Forward) |

ITMF = OTMF -1 IV |

|

|

D-OTMF ( Deep Out of the Money Forward) |

DOTMF = OTMF +1 IV |

|

|

D-ITMF (Deep In the Money Forward) |

DITMF= ITMF- 1IV |

## Please be note that Risk Management policy of the Corporate, Bank, Proprietary Trading Desk, and Financial Institution should be very robust to understand Moneyness aspects of Options Contracts and associated MTM (Mark to Market) on these Contracts. At the same timeshould understand technicalities of Hedge Accounting guidelines under IFRS, US GaaP.

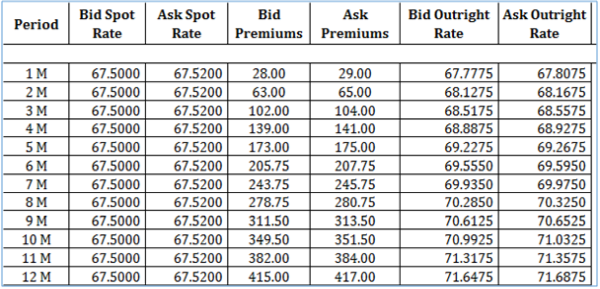

Pricing of Rolling 12 Months Forwards Contracts

Rolling 12 Months Forwards Contracts: -Rolling 12 months forwards contracts are near 12 months contracts like today we are sitting in Feb 2016 henceforth in that sense rolling 12 months is till Feb 2017. Here is the pricing of Rolling 12 Months Forwards Contracts for both Exporters and Importers taken from Thomson Reuters.

Exporter / Importer perspective on Rolling Forwards:-

Sitting today if an exporter would like to sell his Foreign Currency Receivables of say 10 Months period then he would be getting the Outright Rate of 70.9925 or ~ Rs 71/$. If the price at maturity date would be greater than Rs 71 then Exporter would lose and if the price would be lower than he would gain the show. This Gain/ (Loss) on Forwards Contracts is known as Opportunity Cost however would surely hit FX line in P&L.

The reverse holds true for Importers as if the price of at maturity date would be less Rs 71 then Importer would be losing and if the price would be greater than he would be gaining the show. Net Settlement of both Exporters as well as Importers is not in their hands rather depends upon USD/INR rate at the maturity date.

To resolve this issue both Exporters and Importers are advised to take Options Contracts to hedge their ForecastedReceivables, Payables at least for rolling 12 months however they can also hedge their longer tenor receivables, payables using longer tenor Options contracts as well like Cost Reduction Structures, Structured Derivatives which in turn covers

- Range Forwards (Range Forwards Exporters, Range Forwards Importers)

- Seagull (Seagull Exporters, Seagull Importers)

- Digital Options, Knock In Knock out Options Derivatives

- Call Spread (Bull Call Spread, Bear Call Spread)

- Put Spread(Bull Put Spread, Bear Put Spread)

## Reserve Bank of India (RBI) is restricting to have such Cost Reduction Structures or Structured Derivatives till 2 Years rolling period.

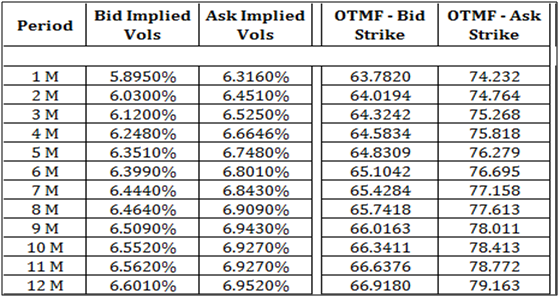

Pricing of Implied Volatilities – Exporters, Importers

The following is the valuation of Exporters and Importers Implied Volatilities taken from Thomson Reuters. Valuation of OTMF Buy Put and Buy Call Contracts done keeping OTMF Buy Put Contracts at 1 Implied Volatility away while OTMF Buy Call at 1.5 Implied Vols away.

Average Implied Volatilities for both Exporters and Importers stand ~ 6.5% for complete 12 months which effectively means there is a great probability that INR would depreciate by at least 6.5% by that time maturity would come henceforth both Exporters and Importers are advised to have Options Contracts in their books which would save themfrom depreciation in INR and off coursesave FX line in their P&L.

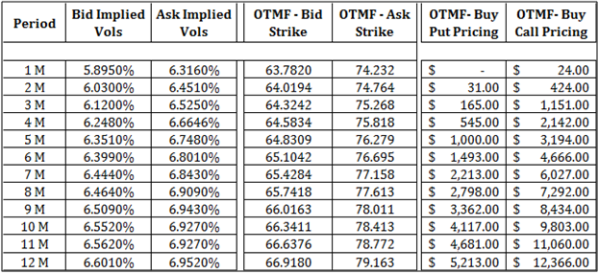

Pricing of Buy Put, Buy Call Options Derivatives Contracts

Points to Ponder:-

- As per Hedge Accounting norms both Exporters and Importers can amortize the aforesaid premiums till the maturity of the Options Derivatives.

- Options helps both Exporters and Importers to cover their upside (Appreciation in USD) and Downside (Depreciation in USD) as markets are getting highly volatile.

Scenario Analysis ~ Forwards Contracts vs Options Derivatives

Suppose an Exporter is taking a 6 Months Forwards Contracts at an agreed price of 69.5550 to cover his USD forecasted receivables. While at the same time Importer is covering his near 6 Months payables at 69.6950.

At the same time there are some Exporterswho are taking OTMF Buy Put at 65.10 and Importers taking OTMF at 76.69 levels to cover their forecasted receivables and payables respectively.

Net Settlement on Maturity (USD Appreciation or INR Depreciation):-Suppose on Maturity INR trading at 70.50/70.55 which effectively means an exporter would be having loss of Rs 1 while Importer would be having the gain in books. If they had taken Options Contracts then Exporter would make Buy Put worthless and sells at market so no loss while Importer would be able to make Buy Call worthless and bought at market.

Net Settlement on Maturity (USD Depreciation or INR Appreciation):-Suppose on Maturity INR trading at 68.50/68.55 which effectively means an exporter would be having gain of Rs 1 while Importer would be having the loss. If they had taken Options Contracts then Exporter would make Buy Put worthless and sells at market so no loss while Importer would be able to make Buy Call worthless and bought at market.

Advice from Editorial Desk:-Editorial Desk of “ The Maverick Treasurer “ recommends usage of Options Contracts to hedge their receivables and payables at least near 12 months. As we understand that markets are getting highly volatile henceforth Options would be able to assist you saving your Downside and Upside.

You are most welcome to connect with Editorial Desk at 91-9899242978, Rahulmagan8@gmail.com or Skype Call ~ Rahul5327. You are also welcome to have the copy of the Magazine by writing at Rahulmagan8@gmail.com keeping subject line as Treasury Magazine – “ The Maverick Treasurer “

CAclubindia

CAclubindia