For homeowners in India, the Equated Monthly Installment (EMI) is a major financial commitment. However, the tax benefits on a home loan can provide significant relief. The key question is: are these benefits available under both tax regimes? This is important for your financial planning: substantial deductions are available under the old tax regime, but they are completely removed under the new tax regime. Choosing the right one can result in substantial tax savings.

A comparative analysis of home loan tax deductions under the old and new tax regimes.

Old Tax Regime

The old tax regime is more advantageous for homeowners, as it allows them to claim significant deductions on their home loan.

Deduction on Interest Paid (Section 24(b))

a. Self-Occupied Property (including ready but vacant homes):

- Maximum interest deduction: ₹2 lakh per year.

b. Let-Out or Rented Property:

- Maximum interest deduction: No upper limit (full amount is deductible).

- Any resulting loss from the property can be used to reduce your overall taxable income, capped at ₹2 lakh per year.

Deduction on Principal Repayment (Section 80C)

- Principal Repayment: Deductible under Section 80C, up to ₹1.5 lakh per year.

- Stamp Duty & Registration: Also deductible under Section 80C in the year they were paid.

- Important Note: Both of these share the same ₹1.5 lakh annual limit with other investments (like PPF, EPF, and insurance).

Additional Deductions for First-Time Homebuyers

| Feature | Section 80EE | Section 80EEA |

| Deduction Amount | Up to ₹50,000 | Up to ₹1.5 Lakh |

| Type of Benefit | Extra interest deduction (over ₹2L limit) | Extra interest deduction (over ₹2L limit) |

| Eligibility | First-time homebuyers | First-time homebuyers of affordable housing |

| Property Value Limit | Specific conditions | ₹45 Lakh or less |

| Loan Sanction Period | Apr 1, 2016 - Mar 31, 2017 | Apr 1, 2019 - Mar 31, 2022 |

| Current Status | Expired | Expired (but may still be claimed on active loans) |

Joint Home Loan

If you have a joint home loan, each co-owner and co-borrower can claim the tax deductions individually. This means the total benefit is effectively doubled, with each person eligible to claim:

- Up to ₹2 lakh for home loan interest under Section 24(b)

- Up to ₹1.5 lakh for the principal repayment under Section 80C

Click Here To Know - Home Loan Tax Benefits For FY 2024-25

New Tax Regime

The new tax regime offers lower tax rates but removes nearly all home loan deductions. Key changes include:

- No Section 80C benefit: You cannot claim any deduction for the principal repayment of your home loan.

- No Self-Occupied Interest Deduction: The ₹2 lakh deduction for interest on a home you live in is not available.

- Limited Let-Out Property Deduction: For a rented property, you can only deduct interest up to the amount of rental income you earn. You cannot use any property loss to reduce your salary or other income.

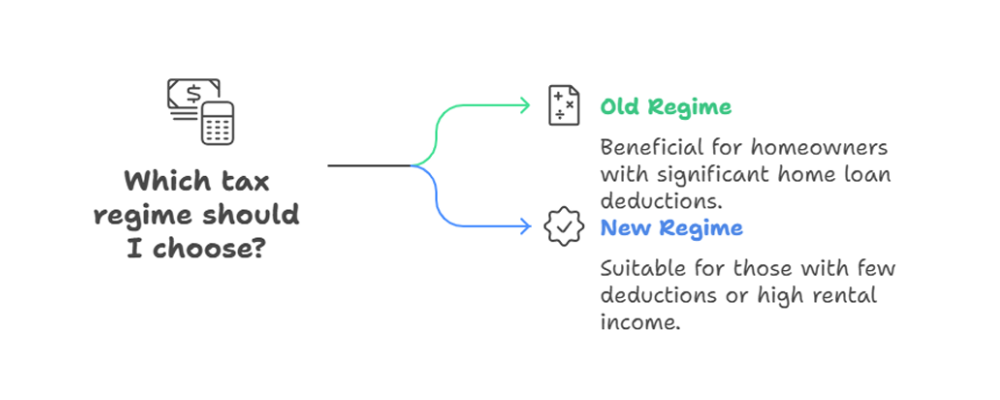

Deciding Between the Old and New Tax Regimes

The optimal tax regime hinges on the ability to claim deductions.

- Choose the Old Regime if you have a large home loan. The deductions for interest (Section 24) and principal (80C) will likely outweigh the new regime's lower rates.

- Choose the New Regime if you have few deductions (e.g., no home loan or investments) or if your let-out property's interest expense exceeds its rental income.

Always calculate your tax both ways using an online calculator to confirm the best choice.

FAQs

Individuals can claim up to Rs.50,000 per annum u/s 80EE on interest paid, in addition to the Rs.2 lakh allowed u/s 24(b) of the Income Tax Act.

Yes. It’s not required for the taxpayer to stay in the property to claim the deduction.

Yes, if both individuals are paying the loan instalments, each of them can claim the deduction separately.

CAclubindia

CAclubindia