This Series will cover the most important Topic- 'Transitional Provisions'. This topic is very much relevant at this stage for all existing assesses who are migrating into GST and wish to have smooth transition.

If, by chance, you didn't come across our previous write-ups in this set of series, those are just one click away on this link GST Simplified.

Update: After a long battle of patience, pursuance and performance, CGST, IGST, UTGST and Compensation Bills have been accorded presidential assent and has become an Act w.e.f. 12th April, 2017. However, its applicability will be notified by Government of India. Now ball is in the States' court who has to legislate their respective SGST Acts.

What 'Transition' is all about ?

Whenever a new levy or new scheme of taxation is introduced, it may completely overwrite the existing tax laws and rewrite rules of the game. That's what will happen when GST is introduced. Entire scheme of Indirect Taxation will undergo radical overhaul. So to cope up with that change, transitional provisions are created in new law to ensure smooth and hassle-free adoption of new scheme of taxation to safeguard interests of existing taxpayers.

Transition can be split into 2 parts:

1. Systemic Transition

2. Regulatory Transition

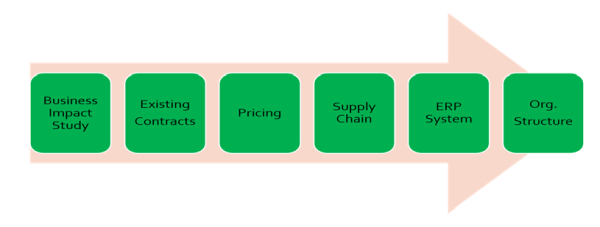

Systemic Transition is about changes in System, process and business structure. Any existing businesses have to revisit their ongoing contracts, internal procedures and go back to their Board room to adapt to new product & marketing strategies which concurs new scheme of Taxation i.e. GST. A deep analysis needs to be undertaken to accommodate any anticipated changes on account of widening tax base, rationalization of tax rates, phasing out of tax exemptions, integrated credit structure and automated compliance system. This will necessitate redesign of ERP system which is not only an Accounting system but one of efficient ways of managing business. Systemic transition is more of case-to-case process and has to be looked separately for different industry verticals.

Systemic Transition will embrace following key aspects:

Let's now move on to Regulatory Transition ('RT' in short) which is governed by GST Law. Sections 139-142 of The CGST Act, 2017 read with consequent Draft Rules deal into Transitional provisions which are discussed below

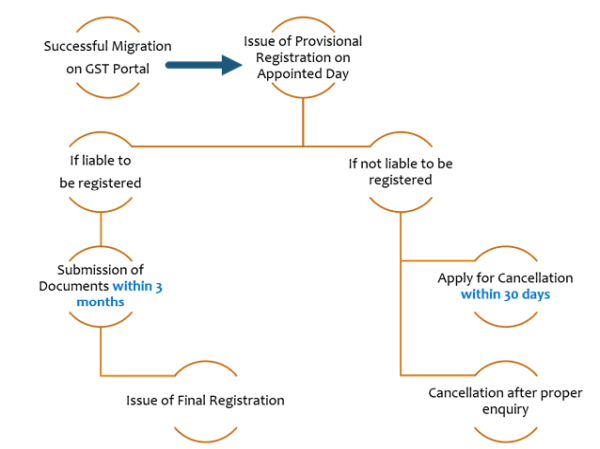

A. Migration of Existing Taxpayers (Section 139)

The migration of existing taxpayers into GST is already undergoing with aggressive push from Government. Provisional IDs have already been issued to taxpayers from State VAT Authorities/ Excise Authorities/Service tax Authorities as the case may be. There would be one Provisional ID for one PAN based registration for each State. That is, if there are multiple locations in single state, only Single Provisional ID is being issued. Not going into much details on migration, below process explains activities post introduction of GST:

Note: There is no provision for migration of registration as Input Service Distributor and the same needs to be applied afresh in GST regime.

B. Transitions- Input Tax Credit (Section- 140)

This is the most important transition because it is where money in form of Credits is involved. This lays down provisions about credits which can be carried forward in different situations subject to conditions thereto. The basic conditions you will find in each situation are as under:

Tax paid on such inputs or input services or capital goods is eligible as Credit in both existing laws as well as GST law'.

Assessee is registered person in GST law. If someone applied for cancellation of registration post-migration, no credits will be allowed.

Which transitional Credits can be availed in GST ?

|

Credits Available |

Available to whom |

Remarks/Conditions |

|

Carried forward in Last Return before GST |

Existing Taxpayer |

� Filed returns for last 6 months before GST � Credit does not relate to goods manufactured and cleared with exemption |

|

Unavailed Cenvat Credit on Capital Goods |

Existing Taxpayer |

For e.g. 50% credit pending to be availed in subsequent F.Y. |

|

Credit of Duties on Inputs/WIP/FG in Stock on Appointed Day |

Registered Person in GST and not eligible for Credit in existing law like: • Exempted Taxpayer, • Works Contractor • First Stage/Second Stage Dealer • Registered Importer • Depot of Manufacturer • Composition Taxpayers |

• Such goods used for making taxable supply • Registered person in possession of invoice /other prescribed documents evidencing payment of duty under the existing law • Such Invoices issued in last 12 months from appointed day • Not eligible for abatement in GST |

|

Credits carried forward in Last Return & Credit of Duties on Inputs/Goods in Stock |

Registered Person dealing in exempted and taxable goods/services in existing law, for which no exemptions are there in GST. |

|

|

Credit on Inputs/input services received post-GST but duty/taxes paid before GST |

Registered Person in GST |

Invoice of such inputs/input services recorded in books within 30 days of appointed day. |

|

Credit of input services received before GST and invoices received |

Input Service Distributor |

Invoice raised by ISD |

|

Credit carried forward in Last return before GST |

Registered person having Centralized Registration in Service tax |

Credit can be transferred to any of registered premises coming under Centralized registration and now separately registered in GST |

|

Credit on Input services reversed on account of non-payment of consideration |

Registered Person |

Can be re-claimed if payment made within 3 months from appointed day. |

Application is required to be submitted by Every Registered Person availing credit by way of Carry forward in return or credit on inputs/goods lying in Stock in Form GST TRAN-1, within 60 days of the appointed day.

C. Transition- Job Work

Applicability if:

- Inputs/goods/semi-finished goods are sent to job worker by principal before appointed date.

- Finished goods are sent outside factory for testing purposes

- such goods are lying with job worker or Testing laboratories as on the appointed date.

Provision in Current Laws

As per provision in Central Excise law, Cenvat credit is allowed on such inputs sent to job worker for further processing and not required to be reversed goods returned back within 6 months or removed form premises of job worker if exemption has been claimed under Notification No. 214-86- CE.

Benefit in GST Law

Now existing taxpayers can obtain benefit of transition and as per GST law, those 6 months shall be counted from appointed date. This is big relief for Principal Manufacturer who gets job work done on their inputs.

D. Misc. Transitional Provisions

Other key provisions are discussed below:

|

Situation |

Provisions |

Remarks |

|

Duty paid goods returned back in GST regime |

• Refund can be claimed if returned from Unregistered person • Shall be Supply if returned by registered person |

Such Goods are removed not earlier than 6 months from appointed date |

|

Price Revision in pursuance of contract entered before GST |

Issue Supplementary Invoice/Credit Note under GST Regime |

• If SI/CN issued within 30 days of price revision. • Recipient to reverse ITC in case of Credit Note |

|

Refund claim filed for Duty/Tax paid before GST |

To be refunded in cash |

Refund claim can filed |

*Appointed Day/Date: It means the day or date when GST Law comes into force.

The author can also be reached at nmjhanwar@gmail.com.

CAclubindia

CAclubindia