We are back with next GST Simplified Series. If you have missed any of our previous write-ups you can discover them here GST Simplified.

Series#2 explains aspects of Levy, Rates & Supply under GST.

Update: CGST, IGST, UTGST Bills have been passed in Lok Sabha on 29.03.2017. Any reference of sections and provisions in this write-up relates to CGST Bill as passed in Lok Sabha.

Levy under GST (Section 9)

Every tax law has a charging section which provides for levy of tax on certain premise. Section 9 provides as under:

- GST shall be levied on intra-state supply of goods or services or both

- GST shall apply on value as determined as per law.

- Rates to be notified, Maximum rate capped at 20%

- Supplier shall collect and pay the tax to the Government.

- Alcoholic liquor for human consumption is kept out of levy.

- Enabling provision to levy GST on Petroleum Products (5 items) on later date.

In normal course, Supplier shall collect and pay GST, however, there is enabling provision of applying reverse charge mechanism i.e. where Recipient of supply is liable to pay tax under following situations:

- Specified categories of supplies(in line with current Service tax law)

- Supply is made by unregistered person to registered person (in line with current VAT laws)

Each and every underlined item is relevant to effectuate levy of GST. Intra-State as already discussed in Series#1 is supply where location of supplier and place of supply is in same State. Let's discuss other terms.

What is 'Supply' (Section-7)

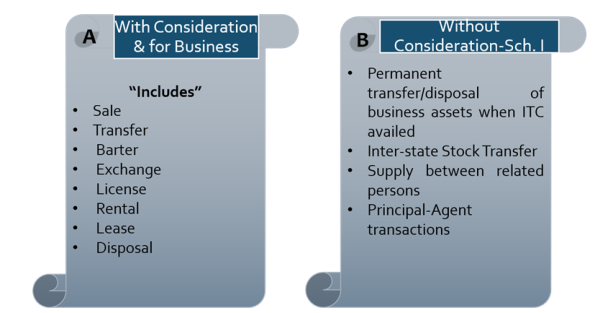

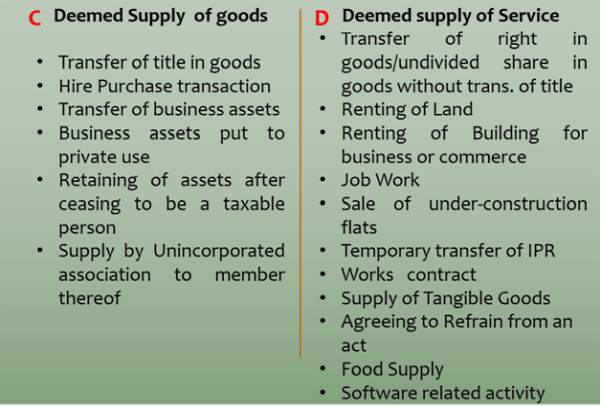

Currently, taxable event for Service tax, Central Excise and VAT is provision of service, manufacture of goods and sale of goods respectively. With GST coming in, this phenomenon will change completely and 'Supply' will trigger levy of GST. CGST bill defines 'Supply' to its widest extent in following 4 parts:

- If made for consideration in course or furtherance of business

- If made without consideration as per Schedule-I

- Deemed supply of Goods as per Schedule-II

- Deemed supply of services as per Schedule-II

Thread-bare of aforesaid points:

Apart from above, Import of service shall be treated as 'supply' in following cases:

- for a consideration whether or not in course or furtherance of business.

- Import by taxable person from a related person or from any of his other establishments outside India, in the course or furtherance of business.

On going through the detailed definition of supply, it is undisputable that scope of 'Supply' is quite wide to cover under its ambit various transactions. This is in line with agenda of Government to widen the tax base.

CGST Bill also contains the negative List of activities which will not be treated as supply and hence, not liable to GST, briefed as under:

- Gifts by an employer to an employee upto Rs. 50,000/- in a financial year

- Services by an employee to employer in course of or in relation to employment

- Services by Court or Tribunal

- Any Services related to deceased viz. funeral, crematorium etc.

- Functions performed by a person in sovereign capacity- M.P., M.L.A., Constitutional post

- Specific activities undertaken by Government, Local Authority engaged as public authorities.

- Sale of land & building

- Actionable claims, other than lottery, betting and gambling

Analysis

Once GST is in place, the impact of expanded scope of 'supply' as taxable event in GST vis-à-vis current laws is explained here below:

Stock Transfer: As you are aware that registration in GST shall be State-wise with provision of more than one registration in a State based on different business verticals. Registration in each state shall be treated as distinct person for GST. Under current tax scenario, inter-state or intra-state stock transfers are subjected to levy of Excise Duty on removal of Goods. The same is not subject to VAT/ CST. In GST, Stock transfers will be treated as Supply and liable to GST. Although, input tax credit can be availed by Stock Transferee but it will block the working capital of business. Plus, there would be issues on value on which GST will be applicable.

Renting of land &Residential space: Currently renting of only commercial space is liable to service tax, while renting of land and residential space is negative list items. As per CGST bill passed in Loksabha, both these activities will now be treated as deemed supply and exigible to GST. This will have denting impact on real estate & logistics sectors.

Currently exempted but GST Law silent: There are various services like provided by RBI, Foreign Diplomatic mission, toll fees, space selling in print media, interest on loans/deposits, health care services, advocates, educational institutions and charitable activities which are currently exempted from service tax. However, CGST Bill is silent on their taxability.

There may be possibility of these being exempted by way of Notification. Interestingly, Services by foreign diplomatic mission was covered under negative list in Revised GST Law but it has been removed in CGST Bill.

Works Contract & Food Supply: As of now, assessee pays both VAT as well as service tax on these transactions, leading to overlapping of tax levy on same value. Treating Works contract and food supply as composite supply and deeming them as supply of service in GST, litigation on its classification of these activities as goods or services or both has been put on rest. But the vital question here is – Works contract and food supply are treated as Deemed sale of goods by Article 366(29A) of Constitution of India. So, treating these items as deemed service in GST will not render them contradictory to the Constitution of India ?

Supply of Tangible Goods: This is another transaction wherein classification of it under 'goods' or under 'services' haunts industry. Transfer of right to use goods is leviable to VAT whereas, transfer of goods without transferring right is leviable to service tax. In GST, the entire transaction is treated as deemed service obviating need to classify as 'goods' or 'services'.

GST on Cross-border Transaction: Recently the Government has widened its tax base by making B2C Cross border 'Online Information & Data base retrieval service' liable to service tax. Whereas other B2C transactions of import of Service remains exempted. However, GST has travelled one step further to tax all B2C transactions of import of service if made with consideration. Possibly Reverse charge will apply on it and this will surely impact overseas service providers. Further, related party cross border transactions have also been made taxable.

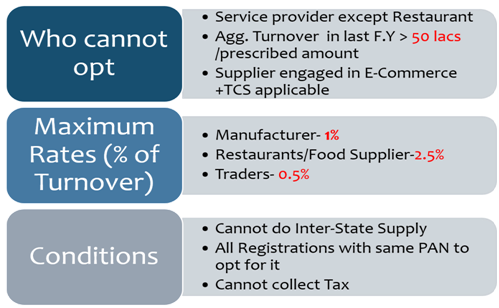

Composition Levy (Section 10)

This is quite well known concept wherein Small scale industries taxpayers are provided an option to simply pay certain % of total turnover with minimal record keeping and compliances. The scheme under GST is outlined as under:

Rates under GST

This is most interesting issue wherein everyone is keeping their eyes on. What will be the Rates under GST ? Which Product will be taxable under which category? As of now following 4 Slabs have been zeroed in meeting of GST Council:

|

Rates |

Expected Category |

|

5% |

Common use items |

|

12% |

Standard rates |

|

18% |

Services to be taxed under this slab |

|

28% |

Luxury/Sin Goods |

Additionally, GST Compensation Cess will be imposed on luxury cars, aerated drinks, pan masala and tobacco products to compensate States for loss of revenue post implementation of GST. However, Finance Minister has many a times assured that rate categorization will more or less be similar to existing structure to avoid any high disruption atleast at initial stage.

Before parting

There has been a deliberation on how GST is 'One Nation One Tax' amid various tax slabs. In my opinion, in country as diversified like India, one rate cannot apply on all items. Otherwise this will severely impact the entire economy. Even 4 Slab structure + Zero-rated structure is commendable provided all States do minimum deviations in their rate structure to roam towards Dream GST.

To be continued.

The author can also be reached at nmjhanwar@gmail.com

CAclubindia

CAclubindia