If you have received a GST demand, you normally have the option to appeal it. You can wish to appeal against it in the Appellate Tribunal (GSTAT) and can temporarily halt the recovery of the outstanding amount by following these steps:

Pay the Pre-Deposit

As per Section 112(8) of the GST Act, you must make a pre-deposit of a certain percentage of the disputed amount. This is a mandatory step to initiate the appeal process.

To make the payment, you need to go -> the Payment section of the GST portal and select Liability Register. Here, you can complete the payment process.

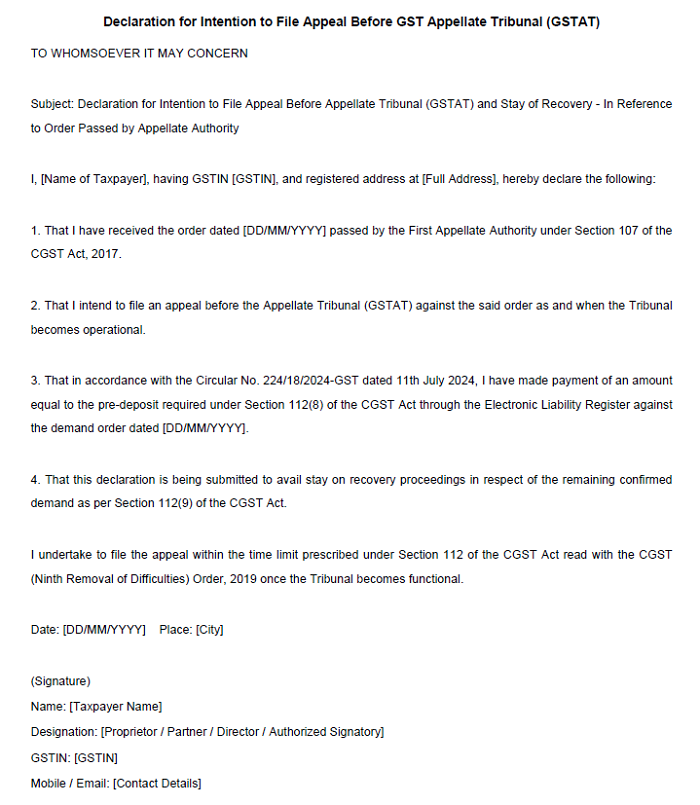

Submit a Declaration

After making the pre-deposit, you are required to prepare a declaration stating your intention to file an appeal.

This declaration should be addressed to the jurisdictional officer (the tax officer who is responsible for your case) stating your intention to file an appeal once the GSTAT becomes operational.

Stay of Recovery

Once you have completed the pre-deposit and submitted the declaration, the recovery of the remaining GST demand will be stayed. This is covered u/s 112(9) of the GST Act.

This means that the tax authorities cannot take any further action to recover the outstanding amount until your appeal is decided.

CAclubindia

CAclubindia