Applicability :

Individual and HUF

Taxability:

Any sum of money,aggregate value of which exceeds Rs.50,000 /- is received during the previous year without consideration,

by an Individual or a HUF from any persons on or after 01.04.06 then the whole of the aggregate of such sum will be taxable.

Exceptions :

Gifts received from the following persons not taxable :

1) Relative

2) On the occasion of the marriage

3) Under a will or by way of inheritance

4) In comtemplation of death of the payer

5) Any local authority

6) Trust or Institution u/s 10(23C)

7) Trust or Institution u/s 12AA

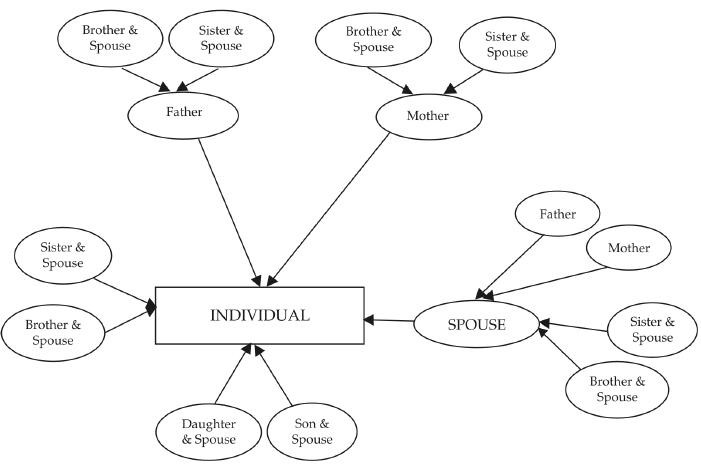

Relative means:

a) Spouse of the Individual

b) Brother or sister of the individual

c) Brother or sister of the spouse of the individual

d) Brother or sister of either of the parents of the individual

e) Any lineal ascendant or decendant of the individual

f) Any lineal ascendant or decendant of the spouse of the individual

g) Spouse of the person referred to in clauses (b) to (f) above

Gift of more than Rs. 50,000/- can be received from

below mentioned relatives without any taxes

Notes:

1. Subject to clubbing provisions applicable for Gift received from Spouse and Father-in-Law.

2. The individual can receive gifts without attracting tax also from lineal ascendents and decendents of the individual other than those mentioned in the above chart.

CAclubindia

CAclubindia