As we will be part of the Historic change in the taxation structure of India which is moving from multiple taxes to one tax GST. Now as far as transition phase is concerned, there may be precautions to be observed by the registered persons as well as Professionals. On the basis of issues we have received, following is the list of FAQs on Transitional provisions of GST. The below given responses are in line with law as on 20th June 2017.

1. What about carry forward of credit of Cess (Krishi Kalyan Cess, Swacchh Bharat Cess) to GST Regime?

As specified in the proviso to Section 140 (1) of the Act, the taxable person is allowed to carry forward the credit to the extent admissible as INPUT TAX CREDIT under GST. Definition of Input tax as given in Section 2(62) does not include any cess. So apparently Krishi Kalyan Cess, Education and Secondary & Higher Secondary education cess will not be allowed to be carried forward.

2. What if I belong to Gujarat and I have sold goods worth Rs. 100,000 against 'C' Form to a dealer in Mumbai however I have not received the 'C' form Yet? Normal VAT rate for the goods sold is 5%.

In Such cases, You are required to obtain 'C' forms within 3 months as per rule 12 of the Central Sales Tax. If you could not receive the 'C' forms within such 3 months then while filling the declaration (GST-Tran-1) for carry forward of credit you have to reduce your Input tax credit by Rs. 3,000 (5% of Rs. 100,000 Reduced by 2% of Rs. 100,000).

3. In order to avoid dispute later on, our company avail the credit only after payments have been made to the Input service provider.

As far as transition period is concerned, please avail the credit prior to 30-06-2017. If you have avail the credit, then it may be considered otherwise You will lose the credit forever.

SO BETTER TO RECEIVE A SHOW CAUSE NOTICE AND THEN REVERSE THE CREDIT. LET THE DEPARTMENT FIND THEIR WAY OUT.

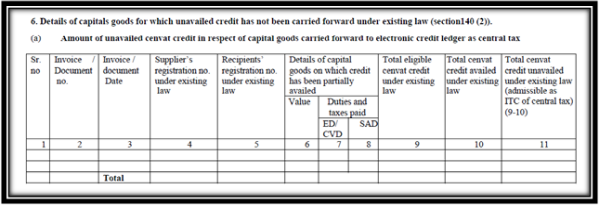

4. We are a manufacturer and we have purchased a machinery in April, 2017 worth Rs. 1 crore on which we have paid Excise duty (ED) of Rs. 15,00,000. We have availed 50 % credit of such ED. 50% is still unavailed. What about carry forward of such credit?

The proviso to Section 140(2) provides for availment of balance credit provided the credit was available under the existing law and is also available under the current law. (There is specific section in GST-TRN-1 as shown below form where you can avail such credit.)

5. We are VAT Registered dealer of 'X Goods' in Gujarat. We do not have any other indirect tax registration. We purchase the 'X Goods' Directly from Manufacturer who issues us excisable invoice however we cannot avail excise credit currently as the same we are not excise registered dealer. Now we are holding 1000 units of 'X Goods' on the appointed day. We already have availed VAT credit for the same.

You will be entitled to take the 100 % credit of all eligible duties and taxes (Includes all excise duties and additional custom duties) in respect of inputs held in stock, inputs contained in semi finished or finished goods held in stock as on the immediately preceding the appointed date. The following conditions must be satisfied:

a. Such inputs are intended for making taxable supplies under GST

b. The registered person is eligible for input tax credit on such inputs under this act.

c. The said registered person is in possession of Invoice evidencing payment of duty under the existing law in respect of such inputs.

d. Such invoice should not be older than 12 months.

e. The supplier of service is not eligible for any abatement under GST.

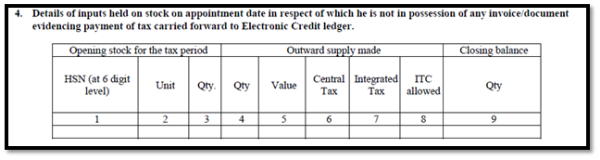

6. We are VAT Registered dealer of 'Y Goods' in Gujarat. We do not have any other indirect tax registration. We purchase the 'Y Goods' from wholesaler who issues us only VAT invoice. Now we are holding 1000 units of 'Y Goods' (Selling price of Rs. 100 per unit) on the appointed day. We already have availed VAT credit for the same.

Your case falls under the provisions of Deemed Credit.

As per Proviso to Section 140(3) read with Rule 1(3)(a) In case where the person does not have duty paid document with him in such case he will be eligible for the credit at the rate of:

a. 60% of CGST where CGST RATE is 9% or more and

b. 40% in all other cases.

So now if 'Y Goods' are rated at 18% GST (9% CGST and 9% SGST) you will be eligible for credit at the rate of 60% x 9% x (1000 units x Rs. 100)= Rs. 5400. However first you will have to pay the tax and then avail the credit by filling Form GST TRN 2.

You will have to file GST TRN 2 at the end of every month (Extract of GST TRN -2 is as follows:

7. We are a dealer of 'Goods X' in Gujarat. Our Supplier resides in Maharashtra. What if They send goods on 29th June 2017 and We receive the same on 3rd July. Shall we be eligible to get the credit in respect of such goods?

As per Section 140(5) - Yes, Provided Following Conditions are satisfied:

a. Tax on such goods are paid before appointed date, i.e. on or before 30th June 2017

b. Receipt of such goods/Services are recorded in the books of recipient within 30 days of appointed date, i.e. on or before 30th July 2017.

c. Furnish GST TRAN 1 within 90 days.

Note: Section 140(5) of speaks about Inputs and Inputs Services in Transit, however It does not make any provisions for Capital Goods in Transit. Therefore The availment of Credit of capital Goods may be disputed by department so suggested that the manufacturer should try to ensure that no capital goods are in transit as on 30th June 2017.

8. We are Service Tax Registered entity. Is there any requirement under GST that my Service tax Return has to be filed within prescribed time to carry forward the credit of existing law to GST? Can I revise such return later on?

Good Point. Yes As per Section 140(8) you will have to file your Service tax return or for that matter any other return within 3 months from the appointed date subject to penalty. I said penalty because as per Service tax provisions you will have to file your return within 25 days however you can file your return late subject to Penalty.

As far as revision is concerned you can definitely revise your return but only within 3 months from the APPOINTED DATE (1st July 2017). Further The credit balance shown in the revise return should be same or less than original return. So the credit amount as per revise return cannot be more than Original Return.

So Be careful while filling your original Return.

9. We have HO in Vadodara and branches in Delhi and Kolkata. We are currently having centralized registration under Service tax. We are having a credit balance of Rs. 10 Crores. Can we distribute such credit to our branches in Delhi and Kolkata as in GST we have to obtain separate registrations for Branches in different states? If Yes, In What proportion?

As per the Third proviso to Section 140(8), the credit can be transferred to any registered person having same PAN for which centralized registration has been obtained. So You can transfer the credit to your branches. Now It is not necessary to distribute the same in any proportion. You can distribute it as per your wish. Nothing with respect to proportion has been specified in the law.

10. We are Jewellers. Some of our stock is lying with the job worker. Any formality on our part?

Yes, You will have to file a declaration in Form GST TRAN 1 within 90 days about the stock lying with your Job worker.

Summary of Forms to be filed:

|

Purpose |

Form Number |

Time Limit |

|

Tax or duty credit carried forward under any existing law or on goods held in stock on the appointed day The amount of credit specified in the application in FORM GST TRAN-1 shall be credited to the electronic credit ledger of the applicant maintained in FORM GST PMT-2 on the Common Portal. |

GSTR-Tran-1 |

Within 90 days from appointed date |

|

Credit in respect of a registered person who was not registered under the existing laws and also not in possession of any document evidencing payment of central excise duty. (subject to conditions) |

GSTR-Tran-2 |

At the end of each of the six tax periods during which the scheme is in operation indicating there in the details of supplies of such goods effected during the tax period. |

The author can also be reached at camayur2@gmail.com

CAclubindia

CAclubindia