BACKGROUND

- When associated enterprises deal with each other =>

- Commercial and financial aspects of the transactions are not influenced by external market sources =>

- Transfer price agreed between associated enterprises does not reflect market forces and the Arm's Length Principle =>

- Tax revenue of the host countries could be distorted due to existence of different tax rates and rules in different countries

RELEVENT SECTIONS AND AUDITING STANDARDS FOR TRANSFER PRICING

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

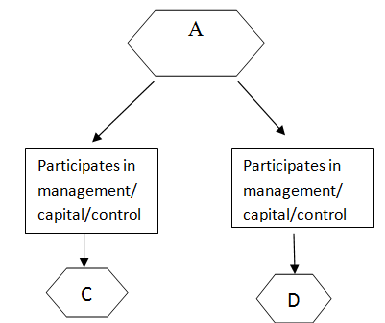

Section 92A : Associated Enterprises

Enterprise which participates:

1. directly or indirectly

2. one or more intermediaries

3. In the management or control of other enterprise

Similarly, an enterprise in respect of which

1. one or more persons

2. who participate in its management or control or capital,

3. directly or indirectly, or

4. through one or more intermediaries

5. are the same persons who participate in

6. a similar manner in the management or control or capital of the other enterprise shall be regarded as an associated enterprise.

In the above situation, C and D are associated enterprises by virtue of A participating in the management or control or capital of both C and D

Broad Definition of Associated Enterprises

Two enterprises shall be deemed to be associated enterprises:

i. One enterprise >= 26% of the voting power of other enterprise

ii. Person or enterprise >= 26% of the voting power in “each such” enterprise, then “each such” enterprises shall be associated enterprises

iii. Lender enterprise gives more than 51% of the book value of the assets of the borrowing enterprise

iv. One enterprise guarantees 10% or more of the borrowing of the other enterprise seeking guarantee

v. When one enterprise has appointed

- More than one-half of the BOD or members of the governing board

- One or more executive directors or executive members of that board

vi. If an Indian enterprise is wholly dependent on the licence granted by a non-resident enterprise for manufacture or processing of goods or articles or business carried out by the Indian enterprise

vii. 90% or more of raw material are supplied by other enterprise and the prices and other conditions related to supply are influenced by the other enterprise.

Section 92F (v): International Transaction

Transaction in which 2 or more associated enterprises,

- either or both of them are non- residents

- in the nature of sale, purchase or lease of tangible or intangible property or provision of services or lending or borrowing money and

- include mutual agreement b/w 2 or more associated enterprises for the allocation or apportionment of any expense incurred in connection with a benefit, service to be provided by one or more such enterprises.

Note: A cross- border transaction may or may not be an international transaction. Conditions to be satisfied are:

1. must be a transaction b/w 2 associated enterprises; and

2. atleast one must be non-resident

3. originates in one country and concludes in another country

SPECIFIED DOMESTIC TRANSACTION: Sec. 92BA

- introduced in Finance Act, 2012

- applicable from A.Y. 2013-14 onwards

Section 92BA

- not being an international transaction

- any expenditure in respect of which payment has been made under

a. Sec. 40A(2)(b)

b. Sec. 80A

c. Sec. 80-IA(8)

d. Sec. 80-IA(10)

- Aggregate of such transactions > 5 crore

Section 40(2)(b)

- Assessing officer is of opinion that such expenditure(interest payments, director’s remuneration, buying goods etc.) is excessive or unreasonable having regard to the FMV of the goods

- So much of the expenditure as is considered by him is unreasonable not allowed as deduction

- Acc. To Fin. Act 2012, no disallowance is attracted in respect of any expenditure being excessive or unreasonable having regard to FMV if such transaction is at arm’s length price as defined in Sec.92F(ii)

- “Persons/entities incurring such expenditure would be subject to SDT.”

- List of persons covered :

i. Relative of the assessee

ii. Individual having substantial interest in the business of assessee

iii. a company, firm, association of persons or Hindu undivided family which a director, partner or member, as the case may be, has a substantial interest in the business or profession of the assessee

Section 80-IA (8)

- Where any goods or services held for the purpose of the eligible business are transferred to any other business carried on by the assessee and

- Consideration, if any, for such transfer as recorded in the accounts of such business does not correspond to the MV, then consequently,

- Profits and gains shall be computed as if transfer had been made at the MV of such goods or services as on that date

Section 80-IA (10): Tax holiday undertakings

i. Tax holiday benefit is disallowed in cases where the assessing officer believes that

ii. Business transacted b/w a taxpayer carrying on an eligible business with a close connection, which results in

iii. More than ordinary profits to the business is to meet the arm’s length price.

iv. Transactions covered under:

- Infrastructure developers

- Telecommunication service providers

- Developer of industrial parks

- Producers or distributors of power

ARM’S LENGTH PRICE: Sec.92F (ii)

- Price at which independent enterprises deal with each other

- ALP is the price which is applied or proposed to be applied in transaction b/w persons other than associated enterprises, in uncontrolled conditions.

Methods to determine ALP : Rule 10B

CUP METHOD:

- Independent enterprises sells the same product as is sold b/w two associated enterprises

- Compares the price charged for property or services transferred in a controlled transaction to the price charged for property or services transferred in a comparable uncontrolled transaction in comparable circumstances

RESALE PRICE METHOD

The price at which property purchased or services obtained by the enterprise from an associated enterprise is resold or are provided to an unrelated enterprise, is identified.

Steps involved

1. Identify the international transaction of purchase or property of services

2. Identify the price at which such property or services are resold or provided to an unrelated party

3. Deduct the normal gross profit from the resale price

4. Deduct expenses incurred in connection with the purchase of goods

SAFE HARBOUR RULES: Sec. 92 CB

In order to reduce the increasing number of transfer pricing audits and prolonged disputes, the Finance (No.2) Act, 2009 w.r.e.f 1.4.2009 inserted a new section 92CB to provide that determination of arm’s length price under section 92C or Section 92CA shall be subject to safe harbour rules.

“Safe harbour” was defined to mean circumstances in which the income-tax authorities shall accept the transfer price declared by the assessee.

Safe Harbour Rules in the following sector/ activities:

(i) IT Sector

(ii) ITES Sector

(iii) Contract R&D in the IT and Pharmaceutical Sector

(iv) Financial transactions-Outbound loans

(v) Financial Transactions-Corporate Guarantees

(vi) Auto Ancillaries-Original Equipment Manufacturers

|

Eligible International Transaction |

Safe Harbour Ratios |

|

IT services and ITES services

|

|

|

KPO services |

(Operating Profit/Operating expense) ≥ 25% |

|

Intra-group loan to wholly owned subsidiary(WOS) where the amount of loan:

|

Interest rate equal to or greater than the base rate of SBI as on 30th June of the relevant P.Y.

|

|

Explicit corporate guarantee to WOS where the amount guaranteed

|

|

|

Contract R&D services relating to software development |

(Operating profit margin/operating expense) ≥ 30% |

|

Contract R&D services relating to generic pharmaceutical drugs |

(Operating profit margin/operating expense) ≥ 29% |

|

Manufacture and export of:

|

Operating profit margin to operating expense:

|

Important Points

- SHRs are applicable for a period of 5 years starting with A.Y. 2013-14 for the prescribed sectors.

- The definition of KPO services has been modified to include only those services that require “application of knowledge and advanced analytical and technical skills”.

- Form No. 3CEFA shall be issued by a taxpayer. It requires information on the nature of business or activities of the taxpayer as well as the details of the eligible transactions opted for the SHRs.

- Taxpayer has the right to file an objection with the Commissioner against adverse order regarding the eligibility of taxpayer/international transaction

- The taxpayer can opt out of the safe harbor regime from the second year onwards.

Conclusion

- The notification of the SHRs is a step towards minimizing transfer pricing disputes and improving the overall investment climate in India from the tax perspective.

- The taxpayer’s right to file objection with the Commissioner against the orders of the Commissioner is a welcome step.

- No time limitation seems to have been prescribed for the AO’s verification of the transfer prices to be in accordance with the relevant safe harbor ratio.

- Maintenance of mandatory documentation for taxpayers opting for SHRs.

- The success of the safe harbor regime may depend on the ground-level administration measures to be implemented by the tax department.

Kanika

CAclubindia

CAclubindia