What are bonds?

Bond is a debt security in which the holder is paid interest at regular interval till maturity and the principal amount at the same date. You can think it as an IOU (I Owe You) given by the issuer to the lender.

How interest is paid?

General bonds (also called plain or vanilla bonds) carry a coupon having a fixed interest rate which is received during the lifetime of the bond.

Is it better than stocks?

This is a preference based question. Returns are generally high on stocks as compared to on bonds, but the return on bonds is fixed and so secured.

| Bonds | Stocks | |

| Rate of return | Generally lower than stocks | Generally high |

| Type of return | Fixed | Variable |

| Risk Factor | Negligible to Nil | Medium to High |

| Preferred by | Who doesn’t want to take risk like the ones planning for retirement or college fees | Who wants to take risk and make a good return |

Who issue bonds?

Bonds can be issued by Central government, Municipal corporations and Companies.

What are the types of bonds issued?

Fixed rate bonds – These bonds carries a fixed rate of interest.

Floating rate notes – These bonds carries variable interest rate based on MIBOR (Mumbai inter-bank offer rate) or LIBOR (London inter-bank offer rate). For e.g. LIBOR + 2% or MIBOR + 1%.

Zero Coupon bonds – These bonds doesn’t carry any interest or coupon but instead issued at deep discount and redeemed at par value. For e.g. a bond of par value Rs. 1000 is issued at Rs. 700 and will be redeemed after 5 years at Rs. 1000, then Rs. 300 is the benefit that a holder will get over a period of 5 years.

Junk Bonds – They carries high risk of default in repayment of amount but carries high rate of return due to their poor credit ratings.

Convertible bonds – These bonds can be converted into a specified number of equity shares or cash. For e.g. a unit of bond can be converted into 10 equity shares of the company or the cash of the same amount. Coupon rate is generally lower on convertible bonds as compared to vanilla bonds and market value is higher.

Exchangeable bonds – These bonds are same as convertible bonds except the fact that instead of conversion into the shares of the issuer company, the bonds are convertible into the shares of companies other than the issuer company (generally subsidiary or in which company has stake).

Gilts – Bonds issued by the government.

Inflation-Indexed bonds – These bonds’ principal and interest payments are indexed according to inflation which means as the inflation increases the rate of interest and value of bonds increases. This eliminates the risk of inflation, so the coupon rate is generally lower than the vanilla bonds. In India, wholesale price index is used to index such bonds.

Subordinate bonds – During liquidation of the company, subordinate bonds will be placed after other bonds in the hierarchy. For more on winding up hierarchy, read my previous article Winding Up of the Company.

Covered bond – As the name defines, covered means it is covered against any uncertainties and backed by pool of assets. So in case of any default, holder has the option of recourse to that pool of assets.

Perpetual bond – As the name defines, perpetual means never ending. Interest is provided on the bonds forever without any redemption of principal amount.

Bearer bond – Interest and principal payment is paid to the bearer of the bond. No records are kept of the transactions or parties involved. It ensures anonymity.

Treasury bond – Bonds issued by central government. No default risk is there so they are the safest bonds but with lower interest rate than most of the other type of bonds.

Municipal bond – Bonds issued by local government, municipalities etc.

Where can I trade in Bonds?

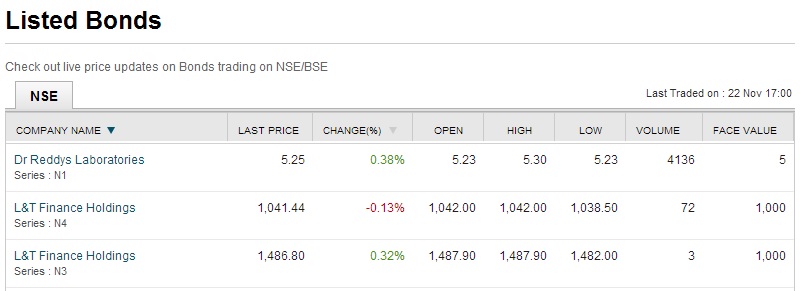

Listed bonds can be traded on NSE/BSE. A quote can be seen as:

- This is an example of bonds listed on NSE.

- Open, high, and low quotes are given which means the Opening, highest, lowest price of bond traded in the day respectively.

- Volume defines the lot in which the bond is traded and face value is given of each bond.

- There can be different bonds or different lot sizes issued by the same company like L&T Finance holdings mentioned above issuing bonds with different lot size (volume).

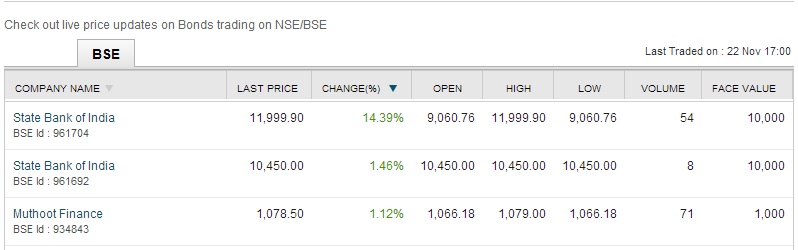

- Given below is an example of bonds listed on BSE –

Bonds require much investment, is there any other way to invest in bonds with lower amount of money?

Yes, bond funds can be bought which falls in the category of Debt long term. These are the type of mutual fund which has the portfolio of investment in different types of bonds and other debts of different companies in different proportion. For more on bond fund, read my previous article Mutual Funds.

I have heard about bond valuation. It means that bond is valued according to certain variables. I want to know that if we know that bond’s value is fixed and the interest rate is also fixed, then how valuation comes into picture?

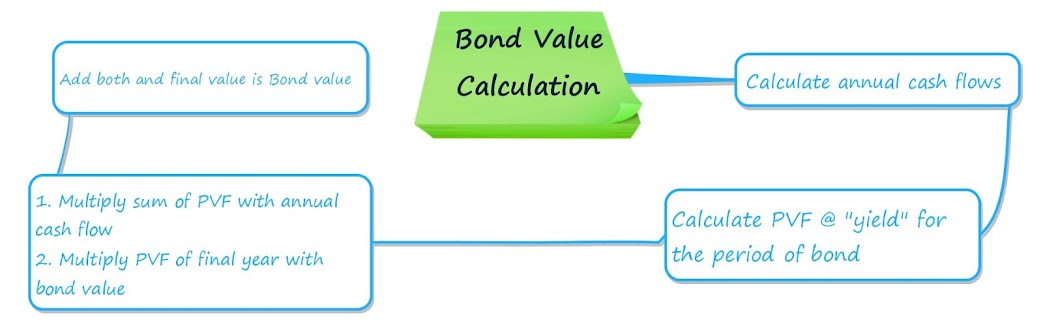

Bond valuation is based on the concept of preferred rate (yield). It is not what is being provided but what you want out of it. Take an example – There is a bond of Rs. 10,000 having 10% coupon rate with maturity of 2 years. You think that the rate of 10% is too low, you want 15% return (yield) and so you want to pay the amount which ensures that you will get a return of 15%.

For this we have to apply discount rate of 15% on annual coupon payments.

1. Calculate annual cash flow (interest received per year) = Rs. 1000

2. Present Value Factor (PVF) means the present value of all the future cash flows which is calculated by taking yield as a rate which is 15% here – (1/1.15) = 0.8695 for 1st year and (1/1.15*1.15) = 0.7561 for 2nd year.

3. Multiply the sum of PVF which is (0.8695 + 0.7561) = 1.6256 with annual cash flow which is Rs. 1000 we get 1626.

4. Multiply the PVF of final year which is Rs. 0.7561 with bond value = 7561.

5. Add both step 3 and 4 which will be 1626 + 7561 = 9187.

6. It means that an investor is willing to pay Rs. 9187 for the above bond if she wants a return of 15%.

I have seen the market value of bonds in the newspapers. How can I decide which one to buy?

First one has to decide that what yield one wants. Continuing with above example we know that the fair value of bond is Rs. 9187. If market value of bond is below this they are selling at low price so investor will want to buy it and if the price is more than the fair value calculated then investor will rather let it go.

An investor can also use the CRISIL rating (Credit Rating Information Services of India Limited). There are the ratings issued for Long term and short term finance including bonds, debentures, mutual funds, preference shares etc. Ratings are AAA, AA, A, BBB, BB, B, C and D.

| CRISIL AAA | Highest safety, lowest credit risk |

| CRISIL AA | High safety, very low credit risk |

| CRISIL A | Adequate safety, low credit risk |

| CRISIL BBB | Moderate safety, moderate credit risk |

| CRISIL BB | Moderate risk |

| CRISIL B | High risk |

| CRISIL C | Very High risk |

| CRISIL D | Expecting to be in default soon or already defaulted |

For all the above examples, I need to state the yield. Suppose I don’t have any particular preference of yield and want to know theyield the market is offering, for comparison with the other bonds then how can I calculate the yield?

The concept talked about is Yield to Maturity (YTM). Calculation is simple. We just use annual coupon payments and add annual benefits and divide it by average of market value and par value (value at which bonds were issued). For e.g. – A bond of par value Rs. 10,000 is selling at Rs. 9500 and it will mature in 2 years. Coupon rate is 10%.

There is actually no need for formula, but for the sake of simplicity, Yield to maturity will be stated as:

Note: Annual benefit = (10,000 – 9500)/2 = 250. Yield will always be greater than coupon rate in case bond is selling at discount. In case the market value of bond is more than Rs. 10,000 which means that instead of selling at discount it is selling at premium, instead of benefit it will bring loss to the investor and Annual loss will be deducted from the market value of bond, so the yield will go down below 10%.

I have heard of the term duration of the bond. How is it different from the normal term of bond?

Duration of bond is totally different from the term of bond. Duration means the time period in which the initial investment is totally recovered. Consider the following figure –

In the first figure, a lever is shown and a fulcrum which is the duration. Maturity period is 5 years which is more than the duration of 3 years. Initial 4 years have consistent cash flows while the last year has major cash flow because it includes principal amount also. Here Duration < Maturity.

Now as the coupon payment is made, the level unbalances as shown in 2nd figure where the first year coupon payment has been made.

Fulcrum needs to move rightwards to balance the lever again, here the overall duration decreased from 5 to 4 years but the on the day of payment duration momentarily increased but as a whole it decreases.

For zero coupon bonds, duration is equal to the maturity because there are no coupon payments.

I got the concept but how to calculate the duration?

(Advance Concept, absorb the basics before further reading)

There are many methods of calculation of duration. Let us discuss mostly used 2 types in short –

Macaulay Duration – This method is the basic one and is widely used. In this, annual discounted cash flows (discounted at required yield) are multiplied with the year in which they are received and are divided by the market value of the bond. For e.g. – There is a bond of market value Rs. 10,000 carrying coupon rate 10%, yield 15% and maturity period of 2 years, then duration will be:

Modified Duration – This is the modified version of Macaulay duration which is based on the concept that as the yield increases, the duration decreases and vice versa. It is obvious that when an investor gets more

return, his initial investment will be returned earlier

This means that if yield changes from 15% to 16%, the duration will decrease from 1.75 years to 1.52 years.

Chiranjiv Kumar

Email: chiranjivkumar@ymail.com

CAclubindia

CAclubindia