Man is a weird creation of god. Although his most perfect creation, we humans have a tendency to be jealous, short-sighted, and selfish and constrained in our views. Few are able to lift their conscience beyond the ‘stopping point’ and step ahead.

Recent days have been tumultuous and rapidly changing for all the professionals and to be professionals. The government seems to be in a state of logjam.

(This is just a comparison and discussion and it is not intended as an insult for chartered accountants or slander towards any body.)

As we all are aware, the tax structure in India will be undergoing a drastic overhaul which will bring it to an altogether different situation, at par with many advanced economies of the world. This changes are in form of the direct tax code and goods and service tax.

Chartered accountants are wonderful professionals. The ICAI is one of the finest institutes established to regulate the accountancy field in india. Four indisputable facts are that:

1) ICAI is an extremely professional and expert professional body.

2) Chartered accountants have become synonymous with accounting.

3) Alumnus of icai occupy many esteemed places in the Indian industries.

4) Being oldest of the professional institutes, it has achieved a numerical superiority over other bodies and therefore has a clout of its own. One of the greatest changes in the tax system will be the definition of accountant. Here is what the clause of direct taxes code says on definition of accountant

Clause 182.3 (not copied verbatim).1) An accountant shall be a member of icai, icmai or the icwai.

On this (as very much expected from icai) , the icai has commented as follows

In this regard, ICAI has through a representation to Ministry of Finance, placed on record its concern not only for the profession, but for the country as a whole since issuance of audit certificates by persons having limited knowledge of audit of accounts will not only be professionally incorrect and but will raise many concerns including causing huge revenue leakages.

Mixed type of reactions come to mind reading this. Does a professional body like icai needs to be so desperate to use words that of this kind ? Does this mean that cost accountants, a 50000 member strong body is imparting useless accountancy knowledge to its members? Is it appropriate for a body like icai to use such words? Certainly not.

Does the fact hold good that if the icai is the oldest accounting body in India, then there cannot be any other institute on this land which can impart accountancy training at par or better than it. Does it mean that other people are just doing a rot job and nothing else? Does it mean that the entire Indian university system outside the icai is teaching nothing to its students ?

Reading the ICAI's half knowledge argument makes one think so.

Equality is the pivot on which strength of a democracy rests. Equality means equality in all terms and in all respects. Without democracy equality cannot and will not function properly.

The apex court in the often cited case of State of west Bengal vs Anwar ali Sarkar (although this is in a different context, but just for reference) has opined on equality in following words.

If it is established that the person complaining has been discriminated against as a result of legislation and denied equal privileges with others occupying the same position, it is not incumbent upon him before he can claim relief on the basis of fundamental rights to assert and prove that, in making the law, the legislature was actuated by a hostile or inimical intention against a particular person or class; nor would the operation of Art. 14 be excluded merely because it is proved that the legislature had no intention to discriminate

Although the above case is of a different context altogether, let us adopt and apply the above guidelines to this case.

1) discriminated – Black’s law dictionary defines discrimination as ‘arbitrary action, based on individual discretion’. Is it not the discrimination of government to sideline its own creation, the icwai for so long from income tax? Agreed that the purpose behind establishment of icwai was cost auditing and costing , but that does not at all mean that they are not proficient in anything else. One should just read the icoai’s journal to see the quality and extremely meritorious work being done.

2) equal privileges- Equal privileges in our case denote equal right and opportunities. When two nearly equally competent individuals are compared, they should be given equal treatment which has not been the case. Cost accountants have the same level of expertise as a ca possesses and which is not subject to any certificate from any institute.

3) others occupying the same position – The position in our case is that of accountancy knowledge. The position of cma and ca is so similar that nearly 70 % of their study curriculum is same. The articleship requirement, the educational standards and professional competence possessed by them are nearly the same. So even if the accountancy body thinks of others as of half knowledge that does not change ground reality.

4) inimical intention against a particular person or class – Here the intention of the government is not at all inimical , but many instances of reforms have been suppressed by the icai. Be it the n.f.r.a , be it this reform , the so called partner in national building has not seen accounting expertise outside itself.

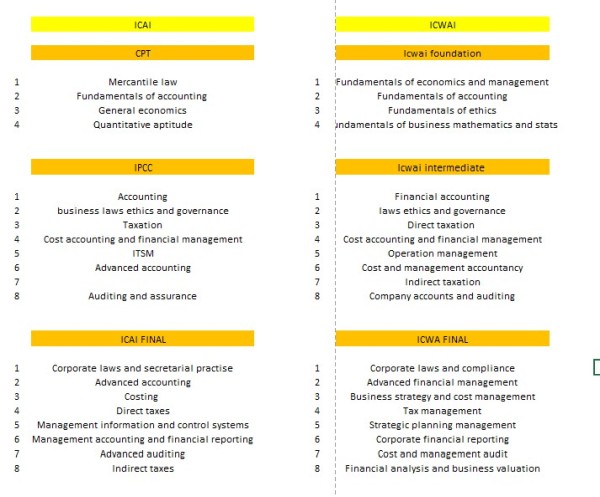

1) What makes a chartered accountant – a chartered accountant?

The Chartered accountancy course comprises of three stages viz – cpt , ipcc and ca-final. The icoai’s course also has the same structure. The duration of professional training, exposure to practical working and discipline in both of them is nearly the same. Chartered accountants can claim superiority over cost accountants if there is something really different or if there is a drastic difference between the study materials of both of the courses. The difference is not at all noticeable when it comes to the course material.

Right from the foundation level up to the final level the syllabus is nearly the same at various stages. Not only is the syllabus same but at some places even the nomenclature of the subjects is the same. We might debate that it was a deliberate move of the icmai to copy icai, Be that the case, does that mean that the icmai members do not know anything of it. When it comes to commerce, then unlike engineering and science, there is a limitation of topics that one needs to study to get acquainted with finance and commerce. Yes finance is much much deeper but that much depth is not needed either in ca or cma. Therefore as far as finance and commerce is concerned, this much is enough.

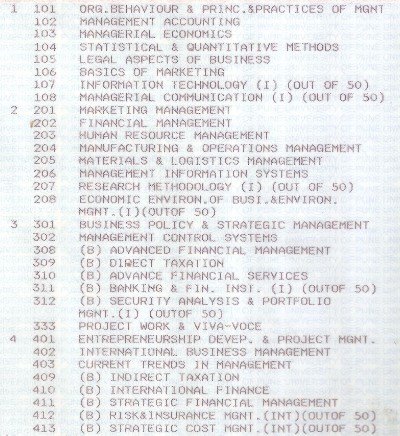

When we look at the u.g.c mba model curriculum guidelines , even the mba curriculum has some or most of the above subjects , although the nomenclature is different. Now the same thing is also taught to a lesser extent in iims also, only the standard of teaching and students is different from a normal mba college. But IIM management graduates also possess financial capabilities that as per industry status are even better than chartered accountants.

.

Therefore there is nothing novel in the syllabus of icai that differentiates it drastically from the icmai or mba course. If universities equate the ca course with mba for admission to management phd (some universities and not all) despite the fact that chartered accountants have not studied any core management subjects , there is a presumption that they have gained knowledge about the same ……. Why cannot the same presumption be applied for cost accountants , especially those who also are m.com graduates or mba graduates. A combined reading of the icmai + mba / m.com syllabus gives up ample satisfaction about the theoretical knowledge and exposure of the cost accountants.

When it comes to other professions1) Doctor – any student who completes his mbbs from anty accredited medical college is permitted to practice as a doctor but has to be registered with the medical council.2) Lawyer – any person doing llb from any college and then affliated to the bar council is a lawyer.

In the same way , there is nothing wrong in cma doing audit as they are the same level of accountants as are chartered accountants.

2) Accounting is not a rocket science. When it comes to determining capability of a person, it’s his knowledge which matters and not any qualification. But in this case we are not talking about any qualification but which are ‘related qualifications’.

Accounting is not a rocket science. With sufficient study and experience one becomes expert in it. When it comes to taxation matters knowledge and discipline is important. Discipline is imposed by chartering the person to a charter. This charter is managed by institute of which the professional is a member. Therefore even if normal post graduates have knowledge of accountancy, yet when it comes to fiscal and taxation matters, not everyone can be permitted to audit. But the icmai is a reputed body having a strong track record. Therefore even if they are allowed to do everything in tax matters what the ca.s do nothing will change? Those giving the ‘duhaai’ of revenue leakages are just wrong and nothing else. Having studied the taxation at inter and final levels coupled with accounting knowledge cma have more than enough knowledge for doing what ca.s do

3) No one needs a certificate from icai to prove their knowledge in accountancy and auditing.

The icai was established to develop the nascent accountancy and auditing in india during the fifties. Having a first mover advantage , it has gained sufficient clout in the accountancy field , thanks to extremely talented people. But that cannot be taken as a sole presumption that accountant shall always mean a c.a and therefore cma do not need icai’s certificate to prove their worth.

4) if purely the icai wants to argue about accountancy being their exclusive turf , then why were they and why are they happy to usurp and encroach upon the turfs of ICSI and ICWAI?

The three professional bodies set up by the government were so set up that there was a clear demarcation between their field, their exclusive playing field / turf and there was hardly any overlapping between them. In the course of time however, the icai was more than happy to usurp the work of other professional bodies. Be it signing of compliance certificates which is supposed to be the work of company secretaries or representation before the various tribunals which is work of advocates.

If it is their knowledge that enables them so, then the same knowledge enables the cma to do what chartered accountants are doing and therefore icai should not argue the same.

5) ICAI’s track record is mixed one ……. In the past too, it has tried hands with different gimmicks and failed badly.

The institute of chartered accountants of india is a parliamentary body and not a private charter giving organization / body like the cfa / garp. Therefore whatever it does , it also has to keep in mind the benefits to the society and uphold the constitutional values. The case of icfai vs icai would prove the same , where icai wanted to restrain their members from doing c.f.a course. The issue was of so less imposrtance that the supreme court , through Justice Markendaya katju rejected it in a mere two page judgement. There is hardly any supreme court appeal that is dismissed with a two page judgement. The issue was paltry, but icai took it right upto the supreme court.

8) ICAI boasts of being a body created by ‘acts of parliament’ …….How can it take it for granted and assume that they are granted and bestowed with a perpetual ‘legal monopoly that shall last forever ?

The legal monopoly given by the parliament is not perpetual and it is open for the government to alter it as it deems expedient. Being a parliamentary body (and not a constitutional body as argued by the icai) the government has all the power to vary the privileges and powers of icai or for the fact , grant similar power to icmai.

9) Who occupies the key position of Chief Financial Officers in the industry in India in leading companies? Nearly 50 % of cfo of sensex and nifty companies and 90 % of ceos of large indian companies are either iim mba or some other degree holders. The cfo post , which is the epitome of financial positions , requires a person who has deep knowledge of finance. If cfo of tcs can be a iim pg holder, if Asian paints cfo can be a company secretary , then income tax professionals can be cma and cs beyond any doubt.

10) The truth is that world over, in the most advanced and developed countries, all professionals are allowed to do statutory audit and income tax audit.

Who can do audit of companies in United Kingdom?

Any member of the following institutes.

|

Association of Chartered Certified Accountants (ACCA) |

|

Association of International Accountants (AIA) |

|

Chartered Accountants Ireland (CAI) |

|

Institute of Chartered Accountants in England and Wales (ICAEW) |

|

Institute of Chartered Accountants of Scotland (ICAS) |

|

Chartered Institute of Public Finance and Accountancy. |

Who can audit in Australia, New Zealand and Oceania?

Any member of the following three institutes:-

|

The Australian institute of certified public accountants. |

|

The institute of chartered accountants in Australia. |

|

The institute of public accountants in Australia |

Who can audit in Canada?

The power of a government in a democracy is unlimited, only subject to the fact that it should not be discriminating, arbitrary and excessive. While our government took years to understand the proficiency of other institutes , the Canadian government went a two steps ahead and mixed up all the professional bodies into one super body designated ‘ Chartered Public accountant ’. All members of following bodies who were first allowed to audit were merged into one. The merging process is currently going on.

|

The Canadian institute of chartered accountants. |

|

The Certified General Accountant association of Canada. |

|

Certified management accountants , Canada. |

Therefore there is nothing wrong in widening the definition of accountants to include CMA and CA, keeping in mind, the larger public interest, academic soundness and global practises. (if anyone is hurt by any part of this article, then i pardon for the same....... this is just a vis a vis comparison and demonstration of true facts)

- Rohit Jain

Facebook id - Rohit Jain

CAclubindia

CAclubindia