CHANNEL FINANCING/

SUPPLY CHAIN FINANCING

A. Introduction

Channel financing is a structured programme though which the bank offers short term working capital facilities to the supply chain stake holders i.e. buyer and the supplier.

For example if the large corporate has to get the supply of raw material from the MSE vendors in a seamless way, the vendors also want to get the payment on due date so that they may not feel the pinch of liquidity of funds.

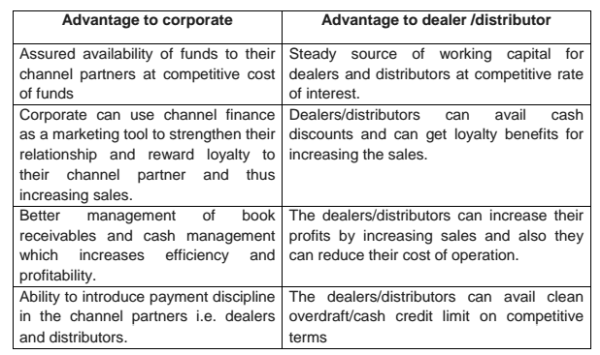

Further if the corporate wants to enhance the sales of its product, it will have to facilitate its dealers/distributors so that they may not face any problem in making the payment to the corporate on the due date or at least just after the sale of the goods.

Channel financing helps the stake holders to sustain a seamless business flow by avoiding any difficulties relating to working capital which are mainly delay in getting the payment from the buyer to the supplier.

Thus this channel financing is something different from the conventional lending. In conventional lending the banks concentrate only on the working of the large corporate or the other unit/enterprise to whom it has financed and has nothing to do with the system and procedure being followed up by or credentials of his supplier or the dealer/distributor unless there is only single buyer or the distributor.

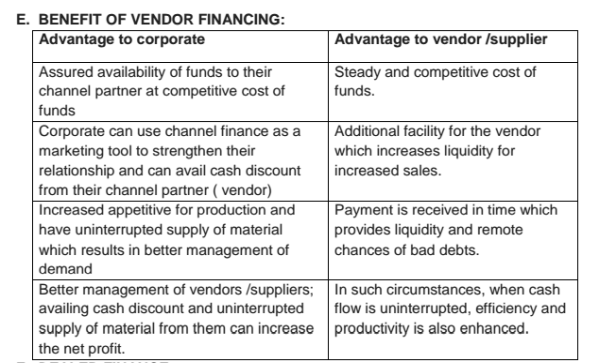

Channel financing is a need based proposition designed to cater to the needs of industries in Agriculture, Automotive, consumer durable, electronics, engineering, FMCGs, Health care, Metal and metal products and pharmaceutical sector etc. It not only helps the Indian business houses penetrate deeper into the market but also creates a value proposition for the MNCs to establish their footprint in the market.

B. Definition of Channel Financing

Channel Financing is an innovative product to extend working capital finance to dealers having business relationships with large companies in India. This may be in the form of either cash credit facilities or as a bill discounting line of credit. Thus in channel financing, the financing bank takes care not only of the corporate manufacturers but also his supplier and the dealer/distributor.

Here this is pertinent to note that in case, the supplier or the distributor of the goods to the corporate is competent to arrange their own funds for total requirement, then there is no need for channel financing product. Therefore, this product of financing arises only when the supplier or the distributor is not in a position to meet its requirement of funds from their own sources for from their own bank due to any reasons and the corporate manufactures wants to help him so that he may get the seamless supply and seamless realization of book receivables from the distributors/dealer.

C. Products under Channel finance

Banks provide different types of products under channel financing depending on the requirement of the business enterprise specifically these are either overdraft/ cash credit or usance bill discounting.

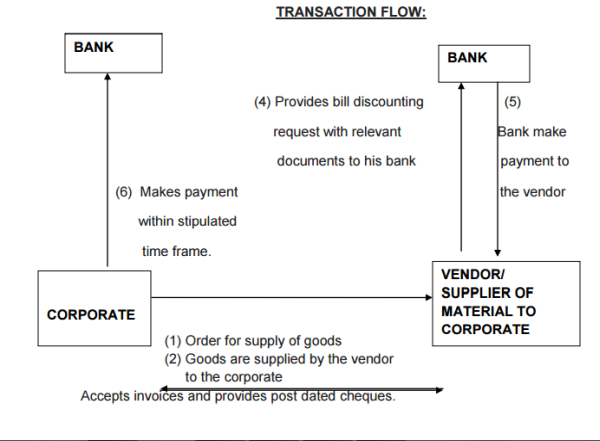

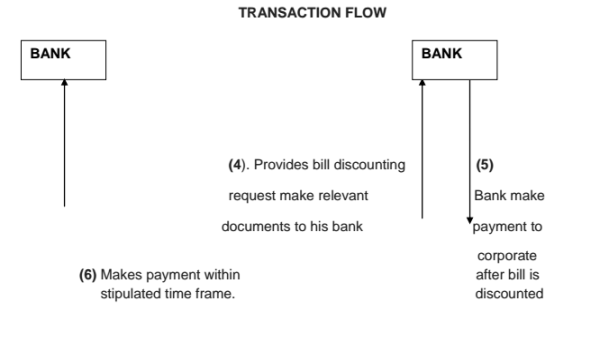

D. Vendor Finance

Channel financing is made through discounting of bills drawn by the vendor/ supplier of goods and accepted by the corporate.

Banks provides bill or invoice discounting facilities to the channel Partners (Vendors/ suppliers) of large companies for making payment on behalf of corporates to the vendors or the suppliers for the goods supplied by them.

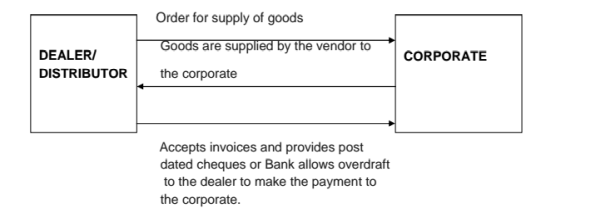

F. Dealer Finance

Channel financing is made through discounting of bills drawn by the corporate and accepted by the channel partner i.e. dealer/distributor by the banks. Banks also provides overdraft facility to the channel partners who have business dealings with the large corporate.

In such like cases, generally, banks stipulates the guarantee of the corporate for the overdraft or bill discounting facility provided to the dealer or the distributor/vendor/supplier of the corporate company.

Channel financing has been suggested for implementation in various forms by various committees set up by Reserve Bank of India. Recommendation of all these committees like Tandon Committee for financing receivables, Chore committee for drawee bill financing, K.R. Ramamoorthy committee for bill discounting and rediscounting by banks have been discussed in chapter no 22 in detail.

Recommendation of Kalyanasundaram committee for factoring has also been discussed in chapter no 24 which is also an effort to promote channel financing. In fact channel financing opens up manifold opportunities due to which the banks can make conscious efforts to make the credit delivery system more popularized so as to boost the industry growth.

CAclubindia

CAclubindia