Derivatives & Capital Market

“To reap a return in ten years, plant trees. To reap a return in 100, cultivate the people.”- Hồ Chí Minh

To begin with

Capital markets help channelize surplus funds from savers to institutions which then invest them into productive use. It, capital market, forms a large part of the “system” that runs an economy.

As Chartered Accountants, we require a basic understanding of the capital market and its constituents to further develop expertise in the field. In the current scenario, Chartered Accounts are much sought after in the lines of Investment banking, fund management, treasury, research analysis. On a lighter note, expertise in capital markets yields gains both in professional and personal zones.

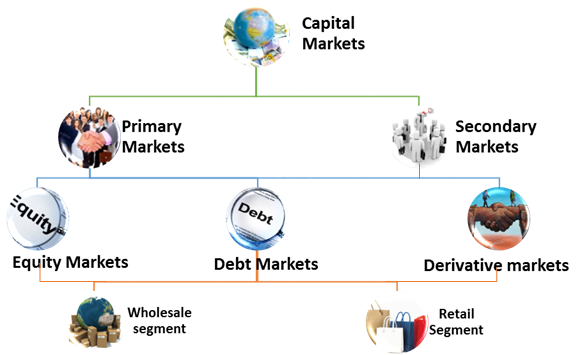

Classification of capital market

Capital markets can be classified as follows

Primary market is where new issue of shares, debentures, preference shares are issued to the public. It acts as a channel to provide funds to the corporates. This is where the buyers get ‘first-hand’ experience of the securities.

Secondary market is the place where the securities are traded after they are initially offered to the public in the primary market. Majority of trading of securities is done in the secondary market. Usually, the funds that are generated in the secondary market do not reach the company. Here, the money is just rotated between the buyers and sellers of the securities. Secondary markets serve as a monitoring and control network which enables the company to better assess their rank among the industry peers.

Equity market involves trading in equity, preference, cumulative preference, and cumulative convertible preference shares. Debt market involves purchase and sale of bonds. Derivative market is the place for organizing trades in futures and options.

Capital market, due to its diverse features, can also be classified as follows

Common terms we hear, here and there

Stock Exchange

The Securities Contract (Regulation) Act, 1956 [SCRA] defines 'Stock Exchange' as a body of individuals, whether incorporated or not, constituted for the purpose of assisting, regulating or controlling the business of buying, selling or dealing in securities. It provides a market platform where the buyers & sellers can transact among themselves. i.e. OLX in the world of securities. Examples are NSE, BSE, MCX, MSE

Stock broker

Stock broker is a registered intermediary or a bridge between the investor - buyer/seller (consumer) of securities and the exchange. On a macro level, a stock broker is thus the face of stock market. He communicates information to & fro between the exchange and the investor. Any eligible person can register with a stock exchange to provide broking services to the public. Examples are RKSV, Zerodha, Karvy, ICICI Direct, Sharekhan etc.

Trading & Demat account

Trading account is an account in which the funds are deposited exclusively for securities transactions. The unit of such account is the appropriate ‘currency’. Demat account is an account where the securities are deposited. The unit of demat account is the ‘number of securities’.

Depository & Depository Participants

A Depository is the bank of all the respective demat accounts. The intermediaries that are registered with a depository are called Depository Participants. Any eligible person can register to provide demat services to the public. Examples of Depositories are NSDL & CDSL, while the examples of depository participants are ABAN Securities Ltd, Indbank Merchant Banking Services Ltd.

Clearing corporation

A Clearing Corporation is a part of an exchange or a separate entity and performs three functions, namely, it clears and settles all transactions, i.e. completes the process of receiving and delivering shares/funds to the buyers and sellers in the market. It provides financial guarantee for all transactions executed on the exchange and provides risk management functions. Example: National Securities Clearing Corporation (NSCCL), a 100% subsidiary of NSE, performs the role of a Clearing Corporation for transactions executed on the NSE.

Nifty & Sensex

CNX Nifty (Nifty), is a scientifically developed, 50 stock index, reflecting accurately the market movement of the Indian markets. It comprises of some of the largest and most liquid stocks traded on the NSE. Sensex is also a stock market index comprising of 30 shares traded on the BSE. Sensex is managed by Bombay Stock Exchange. Sensex and Nifty are the barometer of the Indian Markets. In simple words, performance of securities market as a whole in India is usually measured by the position and movements in Nifty & Sensex. In recent years, indexes have come to the forefront owing to direct applications in finance in the form of index funds and index derivatives.

Derivatives

The Securities Contracts (Regulation) Act, 1956 defines "derivatives" to include “A contract which derives its value from the prices, or index of prices, of underlying securities.” Derivatives are usually classified as forwards, futures and options. Familiarity with these instruments is necessary in order to understand the basics of derivatives.

Forward Contract

A forward contract or simply a forward is a contract between two parties to buy or sell an asset at a certain future date for a certain price that is pre-decided on the date of the contract. The future date is referred to as expiry date and the pre-decided price is referred to as Forward Price. It may be noted that Forwards are private contracts and their terms are determined by the parties involved.

A forward is thus an agreement between two parties in which one party, the buyer, enters into an agreement with the other party, the seller that he would buy from the seller an underlying asset on the expiry date at the forward price. This is different from a spot market contract, which involves immediate payment and immediate transfer of asset.

Forward contracts are traded only in Over the Counter (OTC) market and not in stock exchanges. OTC market is a private market where individuals/institutions can trade through negotiations on a one to one basis.

Forward contracts can be settled either by physical delivery or cash settlement. Physical delivery involves delivery of the underlying asset by a seller to the buyer and the payment of the agreed forward price by the buyer to the seller on the agreed settlement date. On the other hand, Cash settlement does not involve actual delivery or receipt of the underlying asset. Each party either pays (receives) cash equal to the net loss (profit) arising out of their respective position in the contract.

Since forward contracts are not traded on exchange, forward contracts are subject to default risk. Regardless of whether the contract is for physical or cash settlement, there exists a potential for one party to default, i.e. not honour the contract.

Had the contract been traded over an exchange, a stock broker and an exchange along with the help of clearing corporation would ensure that the settlement is made between the contractual parties.

Futures

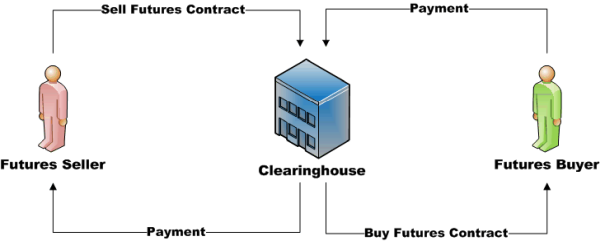

Like a forward contract, a futures contract is an agreement between two parties in which the buyer agrees to buy an underlying asset from the seller, at a future date at a price that is agreed upon today. However, unlike a forward contract, a futures contract is not a private transaction but gets traded on a recognized stock exchange. In addition, a futures contract is standardized by the exchange. All the terms, other than the price, are set by the stock exchange (rather than by individual parties as in the case of a forward contract). Also, both buyer and seller of the futures contracts are protected against the counter party risk by an entity called the Clearing Corporation. The Clearing Corporation provides this guarantee to ensure that the buyer or the seller of a futures contract does not suffer as a result of the counter party defaulting on its obligation. In case one of the parties’ defaults, the Clearing

Corporation steps in to fulfil the obligation of this party, so that the other party does not suffer due to non-fulfilment of the contract.

To be able to guarantee the fulfilment of the obligations under the contract, the Clearing Corporation holds an amount as a security from both the parties. This amount is called the Margin money and can be in the form of cash or other financial assets (which will be collected by the respective stockbrokers of the contracting parties). Also, since the futures contracts are traded on the stock exchanges, the parties have the flexibility of closing out the contract prior to the maturity by squaring off the transactions in the market.

The basic flow of a transaction between three parties, namely Buyer, Seller and Clearing Corporation is depicted in the diagram below:

We gain clarity about anything by noting out differences and by recognizing the similarities. So, let’s see some differences between forwards and futures.

|

Forwards |

Futures |

|

Privately negotiated contracts |

Traded on exchange |

|

Not standardized |

Standardized contracts |

|

Settlement dates can be set by parties |

Fixed settlement dates as declared by the exchange |

|

High counter party risk |

Almost no counter party risk |

Options

Like forwards and futures, options are derivative instruments that provide the opportunity to buy or sell an underlying asset on a future date. An option is a derivative contract between a buyer and a seller, where one party (say First Party) gives to the other (say Second Party) the right, but not the obligation, to buy from (or sell to) the First Party the underlying asset on or before a specific day at an agreed-upon price.

In return for granting the option, the party granting the option collects a payment from the other party which is called the “premium” or price of the option. The right to buy or sell is held by the “option buyer” (option holder); the party granting the right is the “option seller” or “option writer”. Unlike forwards and futures contracts, options require a cash payment (called the premium) upfront from the option buyer to the option seller. This payment is called option premium or option price.

Options traded on the exchanges are backed by the Clearing Corporation thereby minimizing the risk arising due to default by the counter parties involved. Options traded in the OTC market however are not backed by the Clearing Corporation.

There are two types of options—call options and put options.

Call option

A call option is an option granting the right to the buyer of the option to buy the underlying asset on a specific day at an agreed upon price, but not the obligation to do so. It is the seller who grants this right to the buyer of the option. Person who has the right to buy the underlying asset is known as the “buyer of the call option”. The price at which the buyer has the right to buy the asset is agreed upon at the time of entering the contract and is known as the strike price of the contract (call option strike price in this case).

Put Option

A put option is a contract granting the right to the buyer of the option to sell the underlying asset on or before a specific day at an agreed upon price, but not the obligation to do so. It is the seller who grants this right to the buyer of the option. The person who has the right to sell the underlying asset is known as the “buyer of the put option”. The price at which the buyer has the right to sell the asset is agreed upon at the time of entering the contract and is known as the strike price of the contract (put option strike price in this case).

Now when will the buyer of call/put option exercise their rights (since they are anyway not obligated to do so)?

Buyer of Call option will exercise his right when the price of underlying asset (stocks usually) is in the market is more than the strike price (agreed price) on or before the expiry of the contract. Vice versa for a buyer of Put option. He would sell only when the underlying asset fares at a lower price in the market when compared to the strike price.

Let’s see how options are different from futures

|

Futures |

Options |

|

Obligation to fulfil the contract |

Obligation on seller to fulfil only when buyer chooses to exercise his right to do so |

|

Subject to Unlimited risk of loss to both parties |

Only seller has unlimited risk, while buyer’s risk is limited to option premium |

|

Potential to make Unlimited gain or loss |

Buyer and seller have unlimited gain. However loss is limited only for buyer and not the seller. |

On the outside, Capital markets & Derivatives, are seen as instruments of gain and machines of easy money. However, they keep the economy running. Development of a country is also linked to the investing habits of the population. If the population of a country is keen on investments, why wouldn’t the country march ahead? We always remember that day our parents introduced us to savings. Haven’t we benefited from our savings?

Looking forward for a day when the hot discussion in a village is about the immense gain in the Indian stock markets.

CAclubindia

CAclubindia