CA IPC Audit Amendments - May 2017

Amendments Company Audit I (Sec 139 to Sec 148)

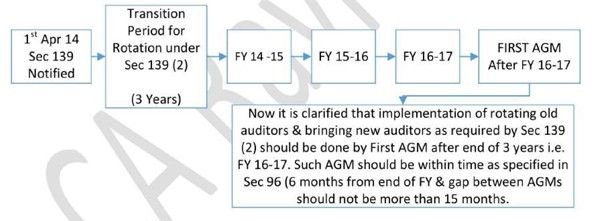

1. Sec 139 / Rotation of Auditor

Old Provision

"Provided also that every company, existing on or before the commencement of this Act which is required to comply with the provisions of this sub-section, shall comply with the requirements of this sub-section within three years from the date of commencement of this Act:"

New Provision

"Provided also that every company, existing on or before the commencement of this Act which is required to comply with the provisions of this sub-section, shall comply with requirements of this sub-section within a period which shall not be later than the date of the first annual general meeting of the company held, within the period specified under sub section (1) of section 96, after three years from the date of commencement of this Act."

2. Sec 148 / Cost Audit

Cost Audit Rules 2014 are amended.

Rule 2 Definition of Cost Audit Report is elaborated. Not significant from exams point of view.

Rule 3 There are 6 industries in regulated sector and 33 in unregulated sector, description of some industries is elaborated to include more companies under rules. Not significant from exams point of view.

Rule 4 One more exemption from Cost Audit, earlier there were 2 now it's total 3.

Company which is engaged in generation of electricity for captive consumption through Captive Generating Plant. For this purpose, the term "Captive Generating Plant" shall have the same meaning as assigned in rule 3 of the Electricity Rules, 2005.

Rule 6 which is regarding process of cost audit. Covering whole rule for better understanding not just amendments.

1. Cost Records should be maintained in form CRA-1

2. Before appointment take written consent of the cost auditor to such appointment, and a certificate from him. (Amendment)

Contents of Certificate

- the individual or the firm, as the case may be, is eligible for appointment and is not disqualified for appointment under the Act, the Cost and Works Accountants Act, 1959 (23 of 1959) and the rules or regulations made there under;

- the individual or the firm, as the case may be, satisfies the criteria provided in section 141 of the Act, so far as may be applicable;

- the proposed appointment is within the limits laid down by or under the authority of the Act; and

- the list of proceedings against the cost auditor or audit firm or any partner of the audit firm pending with respect to professional matters of conduct, as disclosed in the certificate, is true and correct.

1. Company shall within one hundred and eighty days of the commencement of every financial year, appoint a cost auditor

2. Every company shall inform the cost auditor concerned of his or its appointment as such and file a notice of such appointment with the Central Government within a period of thirty days of the Board meeting in which such appointment is made or within a period of one hundred and eighty days of the commencement of the financial year, whichever is earlier, through electronic mode, in form CRA-2, along with the fee as specified.

3. The cost statements, including other statements to be annexed to the cost audit report, shall be approved by the Board of Directors before they are signed on behalf of the Board by any of the director authorised by the Board, for submission to the cost auditor to report thereon.

4. Every cost auditor, who conducts an audit of the cost records of a company, shall submit the cost audit report along with his or its reservations or qualifications or observations or suggestions, if any, in form CRA-3.

5. Every cost auditor shall forward his duly signed report to the Board of Directors of the company within a period of one hundred and eighty days from the closure of the financial year to which the report relates and the Board of Directors shall consider and examine such report, particularly any reservation or qualification contained therein.

6. Every company covered under these rules shall, within a period of thirty days from the date of receipt of a copy of the cost audit report furnish the Central Government with such report along with full information and explanation on every reservation or qualification contained therein, in Form CRA-4 in Extensible Business Reporting Language format.

7. Every cost auditor appointed as such shall continue in such capacity till the expiry of one hundred and eighty days from the closure of the financial year or till he submits the cost audit report, for the financial year for which he has been appointed .

8. The cost auditor appointed under these rules may be removed from his office before the expiry of his term, through a board resolution after giving a reasonable opportunity of being heard to the Cost Auditor and recording the reasons for such removal in writing:

Provided further that the Form CRA-2 to be filed with the Central Government for intimating appointment of another cost auditor shall enclose the relevant Board Resolution to the effect Provided also that nothing contained in this sub-rule shall prejudice the right of the cost auditor to resign from such office of the company. (Amendment)

1. Any casual vacancy in the office of a cost auditor, whether due to resignation death or removal, shall be filled by the Board of Director, within thirty days of occurrence of such vacancy and the company shall inform the Central Government in Form CRA-2 within thirty days of such appointment of cost auditor. (Amendment)

2. The provisions of sub-section (12) of section 143 of the Act and the relevant rules made thereunder shall apply mutatis mutandis to a cost auditor during performance of his functions under section 148 of the Act and these rules. (Amendment)

To read the full article / know more in details regarding the Audit amendments for CA IPC & CA Final May 17 Exam: Click here

To enrol Advanced Auditing subject of the author: Click Here

To enrol Auditing & Assurance subject of the author: Click Here

CAclubindia

CAclubindia