DGGST and not DGST!!

Yes, the Government has renamed Directorate General of Service Tax (DGST) as Directorate General of Goods and Service Tax (DGGST) w.e.f. 01.08.2015….GST is making headlines, Draft reports on GST are being released every now and then, popular forum messages are showcasing GST, seminars and discussions are being held ….we can say GST has become the talk of the town!!

Yet we have no idea when will it be on the floors? Well after the GST bill(The Constitution 122nd Amendment) Bill, 2014 could not be passed in the monsoon session and winter session, the government now plans to take it up in the Budget session.

Well, we can just say, sooner or later- it will be there for sure. Next year we may be filing just GSTR (GST Return) instead of Service Tax, Excise, Vat and other indirect tax returns.

Here’s an insight into the return filing under GST regime.

The Joint Committee has submitted its report on ‘Business Process for GST on GST Return’.

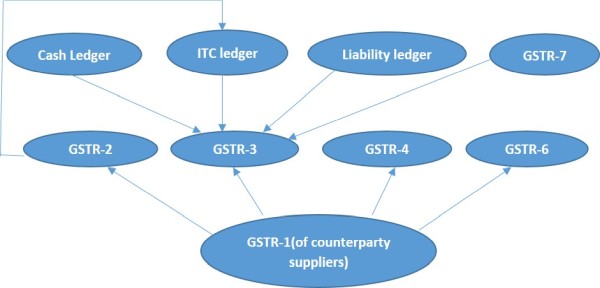

8 forms GSTR-1 to GSTR-8 have been drafted. 3 ledgers namely Input Tax Credit Ledger, Cash ledger and Liability ledger shall also be maintained on the taxpayer’s dashboard.

GSTR-1 to GSTR-3 and GSTR-8 are the regular return forms to be filed by all regular/normal taxpayers.

Every return form is designed to capture some general as well as specific information. The forms have been carefully designed to enable the auto population of data from one form to other so as to minimize duplication in feeding the forms and also to enable cross checks.

The information that would be captured by each form is summarized in the following table:

|

Form |

Information to be captured |

Due date |

Auto population |

|

GSTR-1: For Outward Supplies made by the Taxpayer |

|

10th of next month |

- |

|

GSTR-2: Inward supplies received by a taxpayer |

|

15th of next month |

|

|

GSTR-3: Monthly GST returns |

|

20th of next month |

|

|

GSTR-4: Quarterly return for compounding taxpayers |

|

18th of the month next to quarter |

|

|

GSTR-5: Return for non-resident tax payers |

|

Within 7 days after the date of expiry of registration |

|

|

GSTR-6: ISD return |

|

15th of the next month |

|

|

GSTR-7: TDS return |

|

10th of the next month |

|

|

GSTR-8: Annual Return |

|

31st December following the end of relevant financial year |

|

The auto population is depicted as follows:

Some Salient features:

- Goods and Service tax registration number (GSTIN) for each taxpayer and Unique ID for UN organizations and embassies to be allotted. Some states like Punjab have already started validating PAN of taxpayers to enable quick and easy allotment of GSTIN

- Taxpayers having multiple registrations for different business verticals within a state have to file GSTR-1, 2, 3 for each registration separately.

- Taxpayers eligible for compounding scheme may opt against it to make their supplies eligible for ITC in hands of purchasers.

- Concept of TDS, TDS returns and TDS credit introduced

- Concept of Input service Distributor under the existing Service Tax law retained in GST regime

- If return filed without payment of self-assessment tax, it would be treated invalid and would not be considered for matching of invoices and inter-governmental fund settlement.

- ITC ledger, Cash ledger and Liability ledger maintained on taxpayer’s dashboard will be auto populated from previous tax period return data.

- Return to be filed online or offline (then uploaded later) at GST common portal (GSTN). GSTN will facilitate periodic (may be daily, weekly etc.) upload of information to minimize last minute load on system.

- Returns may also be filed through Apps using Application Programming Interface (APIs)

- There would be no revision of returns. All adjustments/modifications in the monthly returns pursuant to post-sales discount, sale-purchase return, under reported invoice, ITC revision etc. can be made in the succeeding months by way of debit/credit notes, separate tables for revision of invoices and correcting errors.

- A separate reconciliation statement duly certified by a Chartered Accountant shall be filed by taxpayers who are required to get their accounts audited under Section 44AB of Income Tax Act, 1961.

To conclude, we can say that although one return is to be filed for all the indirect taxes under GST regime, return filing and supplying invoice level information on a monthly basis would be a tedious exercise for the taxpayers, especially the small ones.

Introduction of GST is a major tax reform, a new roadmap to indirect taxation! Let’s hope it makes return filing simpler where the taxpayers can just ‘File, smile and Go’.

-Presented by CA Anushri Gupta

anushrigupta.16@gmail.com

CAclubindia

CAclubindia