SECTION A - XBRL FILING OF FINANCIAL STATEMENTS

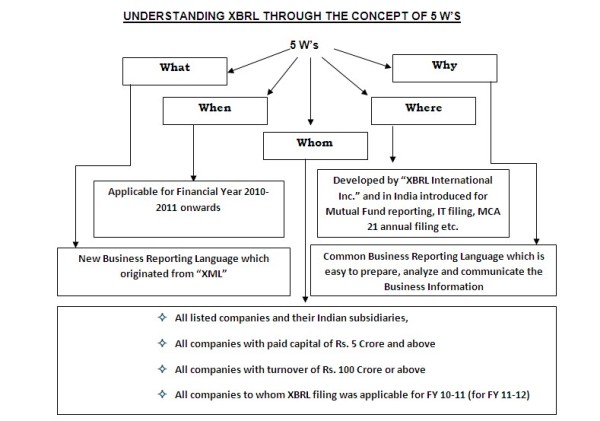

XBRL is the acronym for Extensible Business Reporting Language. As the name itself suggests, it is a language for presentation of data which permits easy analysis and interpretation thereby reducing cost, time and effort. It promotes paperless reporting and thus is in line with the green initiatives being promoted world over.

XBRL is only a method of presentation or reporting. It does not attempt to make any changes in the content to be reported. The idea behind XBRL is simple. Instead of treating financial information as a block of text - as in a standard internet page or a printed document - it provides an identifying label (tag) for each individual line item of data. This data then becomes computer readable.

Ministry of Corporate Affairs introduced the concept of XBRL filing of financial statements to ROC by mandating certain class of companies to file balance sheets and profit and loss account for the year 2010-11 onwards by using XBRL taxonomy. On 05th October 2011, Companies (Filing of documents and forms in Extensible Business Reporting Language) Rules, 2011 were notified.

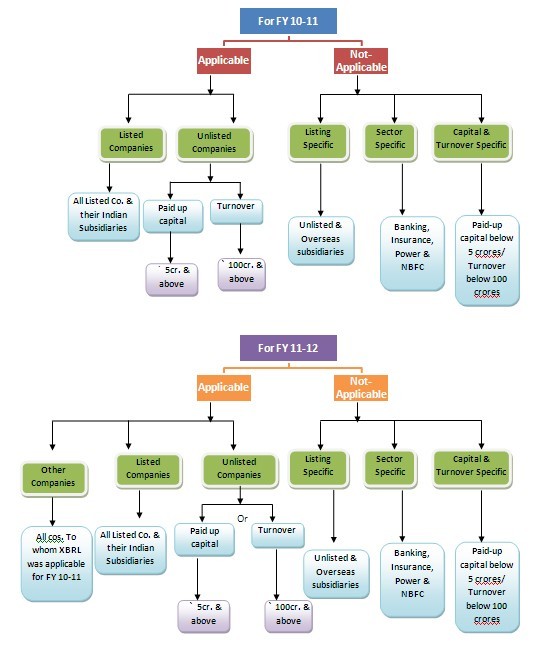

Applicability

Due Date for filing (for FY 11-12)

Non-XBRL Filing

The Ministry issued Generalb Circular No.30/2012 Dated 28.09.2012, In order to ensure smooth filing and to avoid last minute rush, the due date of filing of e-forms- 23AC(Non-XBRL) and 23ACA (Non XBRL)- as per new- schedule VI- is extended in following manner without any additional fee:-

Company holding AGM or whose due date for holding AGM is on or before- 20.09.2012, the time limit will be- 03.11.2012- or due date of filing, whichever is later.

Company holding AGM or whose due date for holding AGM is on or after21.09.2012, the time limit will be22.11.2012or due date of filing, whichever is later.

XBRL Filing

As per General Circular No. 16/2012 issued by the Ministry of Corporate Affairs on 6th July 2012, all companies referred to in para 2 of the said circular will be allowed to file their financial statements in XBRL mode without any additional fee/ penalty up to15th November, 2012 or within 30 days from the date of their AGM,whichever is later.

XBRL filing for the financial year 2011-12 is not enabled by MCA as yet since the validation tool is still under finalization. Recently, MCA has come out with the beta version of the validation tool which is likely to be made effective from 14th October 2012.

MCA XBRL Validation Tool ensures that only those XBRL documents; that satisfy the requirements of Taxonomy and Business Rules, are filed with MCA under section 220 of the Companies Act, 1956. MCA Validation Tool is an important mean for improving the quality of financial information/disclosures in XBRL. Successful validation of the instance document is a pre-requisite before filing the balance sheet and profit & loss account on MCA portal.

It may, however, be noted that mere successful validation of an XBRL document by the MCA Validation Tool does not mean that the provisions under section 211 of the Companies Act, 1956 have fully been complied with. It is important to ensure that this validated XBRL document also provides a true and fair view of the state of affairs of the company as per financial statements adopted in the AGM. MCA XBRL Validation Tool also provides the human-readable pdf version of the XBRL document for ease in authentication and certification of the XBRL document being filed by the company to MCA.

To read the full article: Click Here

CAclubindia

CAclubindia