1. What is AS 25?

Accounting Standard 25 on Interim Financial Reporting is an accounting standard issued by ICAI (The Institute of Chartered Accountants of India) that speaks about the preparation and presentation of interim financial statements of an entity. It prescribes the minimum contents of a complete or condensed set of interim financial statements and the principles for recognition and measurement of items in it.

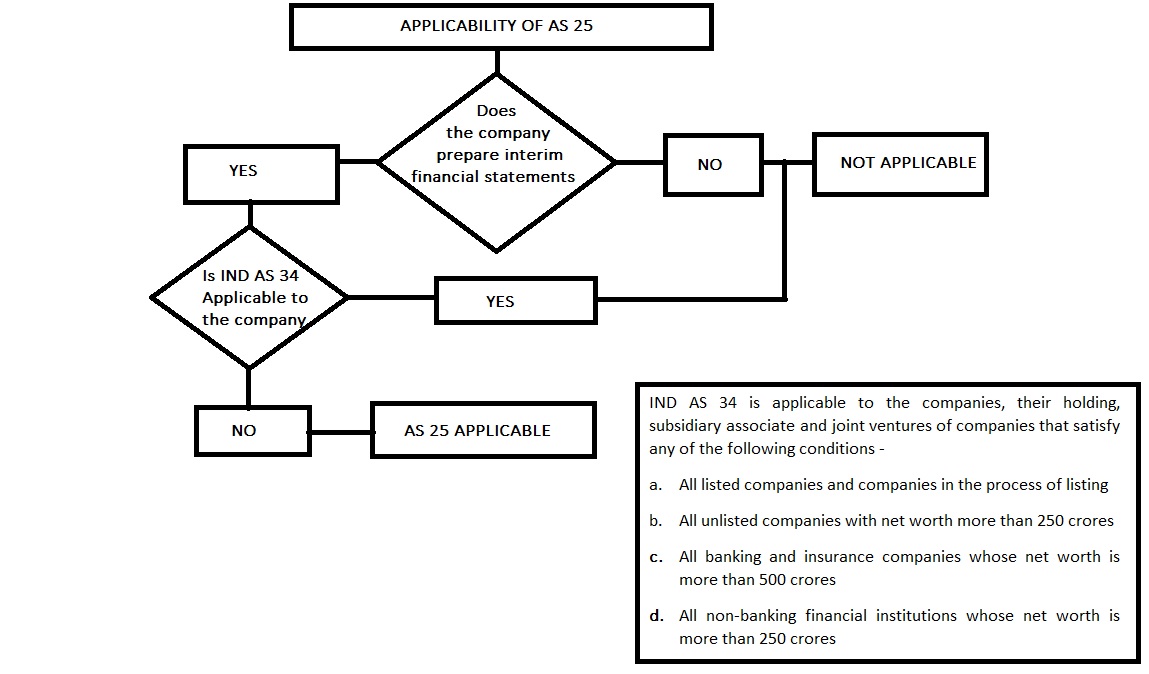

2. To whom is AS 25 applicable?

Back when AS 25 was issued in the year 2002, it was applicable to every entity that decides to or is required to prepare interim financial reports, however, the ministry of corporate affairs has notified IND AS 34 on interim financial reporting to be applicable to selected classes of companies (listed and unlisted companies with a net worth > 500 crores) in the year 2015 followed by a few additions/ modifications to the class/ classes of companies to whom IND AS 34 is applicable. AS of now, IND AS 34 applies to the following class/ classes of companies

a. All listed companies and companies in the process of listing

b. All unlisted companies with net worth more than 250 crores

c. All banking and insurance companies whose net worth is more than 500 crores

d. All non-banking financial institutions whose net worth is more than 250 crores.

If a company falls within any of the above-mentioned criteria, then AS 25 will not be applicable to such company, its subsidiaries, joint ventures, holding and associate companies irrespective of their individual qualifications as these companies need to follow IND AS 34 in the preparation and presentation of its interim financial statements.

Question 1. If A Ltd, an unlisted company has a subsidiary company named P Ltd., as a result of continuous losses in the last five financial years, the net worth of A ltd. and P ltd. are 100 crores and 300 crores respectively. Is AS 25 applicable to these companies? Why?

Answer: - No, AS 25 is not applicable to both A ltd. and P ltd. as the net worth of P ltd. exceeds 250 crores, P ltd. and its holding company i.e. A ltd. need to follow IND AS 34 in preparation and presentation of its interim financial reports as per notification of MCA, and hence AS 25 is no longer applicable to these companies.

Question 2. Would the answer to question 1 be the same if the net worth of P ltd. was 200 crores? Why?

Answer:- In such a case, the above-mentioned answer would change if the net worth of P ltd. was 200 crores as in such case IND AS 34 would no longer be applicable to the company hence AS 25 would be applicable to both the companies.

3. What is the scope of AS 25?

AS 25 mainly deals with two issues -

a. Minimum contents of complete and condensed set interim financial statements.

b. Principles for recognition and measurement of items in the financial statements.

This standard does not speak about the frequency at which the entity is required to prepare the interim financial statements nor does it specify the class or classes of entities that are required to prepare interim financial statements. The standard only specifies the minimum contents of a complete or condensed set of interim financial statements and the principles for recognition and measurement of items in the interim financial statements of entities to whom this AS is applicable. Further, at times the statute governing the entity or the regulators may require to prepare and present certain information in a way which might be different in form and/or content as required by this AS, in such cases, the principles laid down in this standard for recognition and measurement should be applied for such information, unless otherwise specified by the statute or by the regulator. For example, IRDAI requires insurance companies to prepare and present information in a specific manner, then SBI would be required to prepare and present the data in a specified manner as required by the Banking Act or as per the guidelines of RBI, however, the information contained in it would be recorded and measured using the recognition and measurement principles of AS 25 unless it is in contradiction with the principles specified under statute or principles specified by the regulator.

4. What is an interim financial report? What are its contents?

An interim financial report is a financial report containing either a set of complete financial statements (as described in AS 1) or a set of condensed financial statements (as described in this standard) for an interim period. This AS requires the interim financial report to consist, at a minimum, a set of condensed financial statements.

AS 25 requires the interim financial reports to contain at a minimum, a set of condensed financial statements, further, if an entity chooses to present a set of condensed financial statements in its interim financial report, then as per the AS, the financial statements should contain, at a minimum -

a. Each of heading and sub-heading included in the most recent annual financial statements, and

b.Selected explanatory notes as required by the statements.

However, if the company chooses to provide a complete set of financial statements with its interim financial reports, then the form and content of such financial statements must comply with the requirements of a complete set of financial statements i.e. it should comply with every requirement in relation to the preparation and presentation of financial statements as they would at the end of the financial year, any additional line item or note may be disclosed in the financial statements if their omission would make financial statements misleading. The AS also requires calculation of basic and diluted earnings per share on the face of profit and loss account if the company provides the same in its annual financial statements.

Note: - Condensed financial statements are usually prepared by the company to provide the users of financial statements an overview of the company' s financial status, business structure, and business performance. To do so, the company classifies various expenses into various groups based on their nature hence the details of every sub-category of expenses are not be disclosed in the condensed financial statements as they are in the complete set of financial statements, for example, opening stock, purchases and closing stock may be adjusted to disclose cost of goods sold in the condensed profit and loss account also, they may not show revenue from sale of goods and/ or services separately and simply disclose them as "total revenue". A set of condensed financial statements include the following:-

a. Condensed balance sheet;

b. Condensed set of profit and loss;

c. Condensed cash flow statement;

d. Selected explanatory notes.

5. What are the various disclosures to be made in selected explanatory notes as per AS 25?

This AS only specifies the minimum disclosures that are to be made by an organization in the notes to interim financial statements. The following are the disclosures that are required by the accounting standard to be made in the explanatory notes to the financial statements of the entity. Please note that these disclosures are only required to be made if such disclosure(s) is /are material and have not been made elsewhere in its interim financial report.

- A statement that the accounting policies followed in the interim financial statements are the ones that have been followed in the most recent financial statements of the entity or if the policies have changed, then the description, nature, and effect of change in the policy should be disclosed.

- Explanatory note about seasonality of interim operations.

- Nature and amount of items that are unusual by their nature, amount or incidence as per AS 5.

- The nature and amount of changes in estimates of the amount reported in prior interim periods of the current financial year or changes in estimates of the amount in the prior financial year if those changes have a material impact in the current interim period.

- Issuances, buyback, repayment, and restructuring of debt, equity, and potential equity shares.

- Dividends, aggregate or per share (In absolute or percentage), separately for equity shares and other shares.

- Segment revenue, segment capital employed (segment assets minus segment liabilities.) and segment results for business segments or geographical segments whichever is the enterprise' s primary basis of reporting (This disclosure is required only if AS 17: Segment reporting is applicable to the entity.).

- The effect of changes in the composition of the enterprise during the interim period such as amalgamations, acquisitions and disposal of subsidiaries and long term investments, restructurings and discontinuing operations.

- Material changes in contingent liabilities since the last annual balance sheet date.

The AS also requires the entity to disclose any other events or transactions that are material to an understanding of the current interim period.

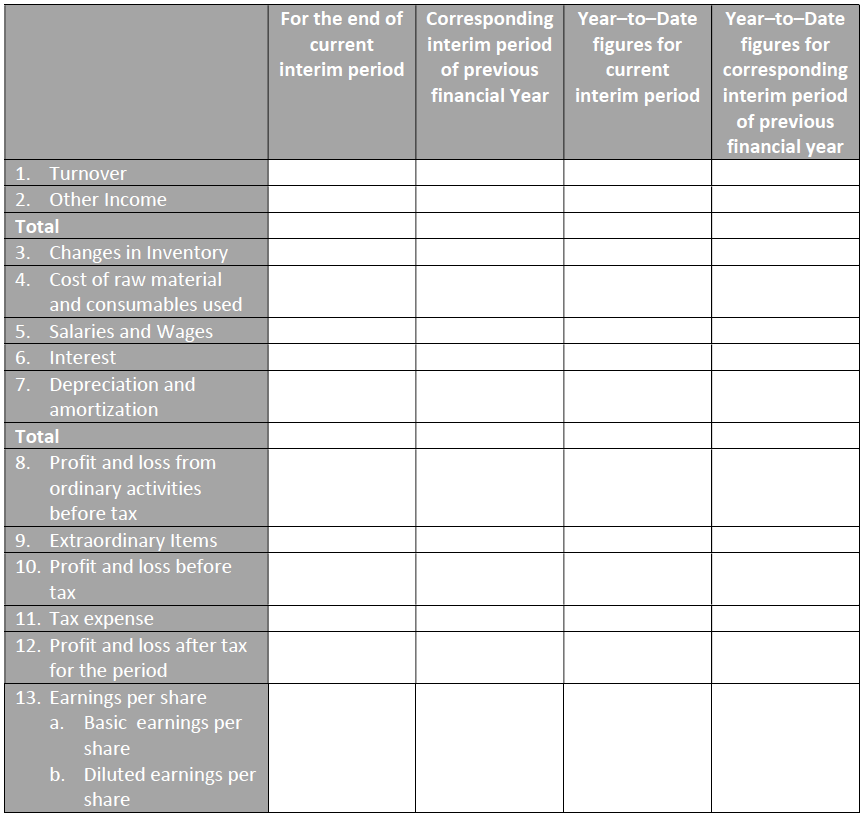

6. What are the different periods for which financial statements are required to be prepared and presented in interim financial statements?

The financial statements should include financial statements for below mentioned periods -

- Balance sheet - As on end of the current interim period and as on end of immediately preceding financial year

- Statement of profit and loss -

i. F or the current financial year - for the current interim period and cumulative on a year-to-date basis.

ii. Historical data for comparison - for comparable interim financial period and year to date of immediately preceding financial year.

3. Cash flow statement - Cumulatively for the current financial year on year to date basis and comparable year to date of immediately preceding financial year.

This could also be summarized in the table below

|

Statement |

Current |

Comparative |

|

Balance Sheet |

End of the current interim period |

End of immediately preceding financial year. |

|

Statement of profit and loss |

Current Interim period Cumulatively for year-to-date |

Comparable Interim period Year to date of immediately preceding financial year |

|

Cash flow statement |

Cumulatively for the current financial year-to-date |

Comparable year-to-date of immediately preceding financial year. |

7. What are the various other points to be considered while preparing interim financial statements and interim financial reports?

Following are a few key points to be kept in mind while preparing interim financial statements and reports -

a.Same accounting policies as annual financial statements -

- Unless changes are made in accounting policies after the date of recent annual financial statements, interim financial statements are to be prepared with the same accounting policies as annual financial statements.

- The frequency of the enterprise's financial reporting should not affect the measurement of its annual results. To achieve this, measurements for interim reporting purposes should be made on a year-to-date basis.

- The recognition of items in the balance sheet which do not meet the definition of asset or liability is not allowed.

- The nature and amount of any significant changes in estimates of the amount made to the amounts disclosed in prior interim periods are to be disclosed.

b.Revenues that are received seasonally or occasionally within a financial year should be anticipated or deferred as of an interim date only if such anticipation or deferral would be appropriate at the end of the enterprise' s financial year.

c.Costs that are incurred unevenly within a financial year should be anticipated or deferred as of an interim date only if such anticipation or deferral would be appropriate at the end of the enterprise' s financial year.

d.Presentation and disclosure requirements of AS 25 should be applied only if the enterprise presents its "interim financial reports" and not to "interim financial results". However, AS 25 should be applied for recognition and measurement of items contained in "interim financial reports".

e.In deciding how to recognize, measure, classify or disclose an item for interim financial reporting purposes, materiality should be accessed in relation to interim financial data for the reasons of the understandability of interim figures.

f.If an estimate of an amount reported in an interim period is changed significantly during the final interim period, but a separate financial report is not prepared and presented for that interim period, the nature and amount of change in estimate should be disclosed in a note to the annual financial statements for that financial year.

Mentioned below is an illustrative format for the presentation of condensed interim financial statements for your reference.

A. Condensed Balance Sheet:

|

Figures at the end of the current interim period |

Figures at the end of the previous financial year |

|

|

I. Capital and Liabilities |

||

|

1. Capital |

||

|

2. Reserves and surplus |

||

|

3. Loan funds a. Secured b. Unsecured |

||

|

4. Other Liabilities and provisions |

||

|

Total |

||

|

II. Assets |

||

| 2. Investments | ||

|

3. Current Assets: a. Inventories b. Sundry Creditors c. Cash and Bank Balances d. Loans and advances e. Other current assets |

||

|

Less : Current liabilities and provisions a. Liabilities b. Provisions |

||

|

Net Current Assets |

||

|

4. Profit and loss account |

||

|

Total |

B. Condensed Profit and Loss Account:

C. Condensed Cash Flow Statement:

|

Year- to- Date figures for the current interim period |

Year- to- Date figures for the corresponding interim period of the previous financial year |

|

|

1. Cash flows from operating activities |

||

|

2. Cash flows from investing activities |

||

|

3. Cash flows from financing activities |

||

|

4. Net increase/(decrease) in cash and cash equivalent |

||

|

5. Cash and cash equivalents at beginning of the period. |

||

|

6. Cash and cash equivalents at end of the period. |

CAclubindia

CAclubindia