In M&A transactions, "Slump Sales" are considered to be one of the most preferred ways of carrying out a deal due to various tax and stamp duty incentives associated with it.

Meaning of 'slump sale'

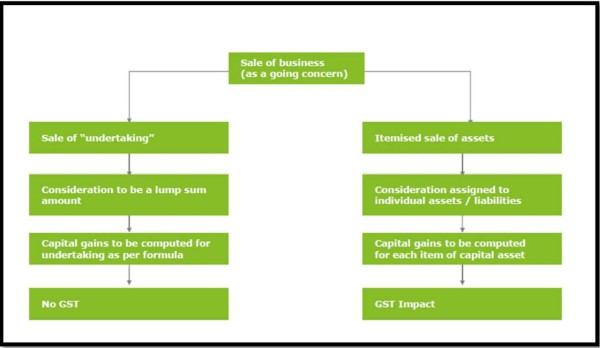

In simple words, 'slump sale' is nothing but transfer of a whole or part of business concern as a going concern; lock, stock and barrel.

As per section 2(42C) of Income-tax Act 1961,

Slump Sale means

- the transfer of one or more undertakings

- as a result of the sale

- for a lump sum consideration

- without values being assigned to the individual assets and liabilities in such sales.

As per Explanation 1 to section 2(19AA), 'undertaking' shall include any part of an undertaking or a unit or division of an undertaking or a business activity taken as a whole, but does not include individual assets or liabilities or any combination thereof not constituting a business activity.

Important Points to be noted:

- The consideration for transfer is a lump sum consideration. This consideration should be arrived at without assigning values to individual assets and liabilities. The consideration may be discharged in cash or by issuing shares of Transferor Company.

- Possibility of identification of price attributable to individual items (plant, machinery and dead stock) which are sold as part of slump sale, may not entitle a transaction to be qualified as slump sale - CIT vs. Artex Manufacturing Co., [227 ITR 260 (SC)]. However, in case of slump sale which includes land/building where separate value is assigned to it under the relevant stamp duty legislation, the slump sale will not be adversely affected in the light of Explanation 2 to section 2(42C).

- Explanation 2 to section 2(42C) clarifies that the determination of value of an asset or liability for the payment of stamp duty, registration fees, similar taxes, etc. shall not be regarded as assignment of values to individual assets and liabilities. Thus, if value is assigned to land for stamp duty purposes, the transaction will be a qualifying slump sale under section 2(42C).

- Transfer of assets without transfer of liabilities is not a slump sale

- No Court approval required

Taxability of gains arising on slump sale as per Income Tax Act, 1961

Section 50B of the Income-tax Act, 1961 provides the mechanism for computation of capital gains arising on slump sale. On a plain reading of the Section, some basic points which arise are:

1. Special Provision:

Section 50B reads as 'Special provision for computation of capital gains in case of slump sale'. Since slump sale is governed by a 'special provision', this section overrides all other provisions of the Act.

2. Period of Holding:

Capital gains arising on transfer of an undertaking are deemed to be long-term capital gains. However, if the undertaking is 'owned and held' for not more than 36 months immediately before the date of transfer, gains shall be treated as short-term capital gains.

3. Year of Taxability:

Taxability arises in the year of transfer of the undertaking.

4. Formula:

Capital gains arising on slump sale are calculated as the difference between sale consideration and the net worth of the undertaking.

Capital Gain= Sale Consideration-Net Worth

5. Net Worth:

Net worth is deemed to be the cost of acquisition and cost of improvement for section 48 and section 49 of the Act.

Net worth is defined in Explanation 1 to section 50B as the difference between 'the aggregate value of total assets of the undertaking or division' and 'the value of its liabilities as appearing in books of account'. This amendment has made it clear that the slump sale provisions apply to a non-corporate entity also.

The 'aggregate value of total assets of the undertaking or division' is the sum total of:

- WDV as determined u/s.43(6)(c)(i)(C) in case of depreciable assets.

- The book value in case of other assets.

For Computing the net worth, the assets on which deduction has been allowed under section 35AD and if such assets are transferred under slump sale, the value of such assets shall be taken as NIL.

6. Indexation Benefit:

As per section 50B, no indexation benefit is available on cost of acquisition, i.e., net worth.

7. Case of More than one undertaking:

In case of slump sale of more than one undertaking, the computation should be done separately for each undertaking.

8. Revaluation:

Revaluation of assets shall not be considered while computing the “net worth” i.e. revaluation of assets shall be nullified for computing the “net worth”, irrespective of the fact that revaluation is done in the current year or in past years.

9. P/G/B/P:

No Profits under the head P/G/B/P shall arise in case of a slump sale even if stock is transferred in slump sale

Cherry Picking under Slump Sale-Allowed or Not?

While until recently, the courts were, on a multiple occasions, consistently taking the position that in the event any part of the undertaking or the assets are retained by the transferor entity, then such transaction will not be construed as a slump sale or sale of the business as a going concern and accordingly the VAT laws will be applicable to such transactions.

As a result of the above, it became implicit that any sort of cherry picking would be inconsistent with the concept of "slump sale" as defined under Income Tax Act, 1961 and hence not permissible.

However, the judicial view recently saw a notable deviation when various forums deviated from the aforesaid understanding and stand on the scope of Slump Sale and thereby approach for determining the applicability of VAT on such deals.

For instance, Delhi High Court in the case of Triune Projects Pvt. Ltd vs. DCIT, upheld the position that a transaction does not cease to be a slump sale merely due the seller retaining certain defunct or unwanted assets of the undertaking.

The crux of the judgment is that, for a sale to be termed as `slump sale' it is not necessary to transfer all assets and liabilities, however, the core elements of the business must be transferred for a lump sum price and the Transferee must be able to continue running the business without the assets which have not been transferred.

The point to be noted here is that, Delhi High Court herein has specifically examined the issue from the perspective of Section 50 B of the Income Tax Act and although it may be quite reasonable to extend the same ratio while determining VAT and other tax liabilities, but the same is not completely unambiguous and clarity on such specific aspects by the authorities would be required before firming any view on the same. The similar position was taken by Kolkata High Court.

GST on Slump Sale:

Slump Sale before GST

Tax regime for Slump Sale prior to enforcement of GST: Under the erstwhile tax regime, transfer of a business as a going concern including transfer of whole unit or a business division was not subject to Sales Tax or Value Added Tax (VAT). The rationale behind this was that the sale of whole business cannot be equated to sale of moveable goods which was subject to sales tax only.

However, the judicial interpretation and view on applicability of VAT on Slump Sales, was not clear.

Slump Sale Post GST

India has recently switched to GST from the complex and multilayered tax regime that was prevalent till now.

The Central Goods and Services Tax Act, 2017 (CGST Act) does not clearly stipulate the law vis-a-vis transfer of business as a going concern or slump sale. Thus, there is no settled position or clarity whether the transactions involving slump sales would be taxable under the new CGST Act or not. The market players are also divided in their views on the same.

Considering the budding stage of implementation of this regime, unlike VAT, there is no judicial pronouncement on the issue. Therefore, the provisions of the CGST Act need to be analyzed in order to reach a fairly inferable view on the applicability of GST on Sump Sales.

Under the CGST Act, in terms of combined reading of the charging Section 9 (Levy and Collection) and Section 12 (Time of Supply of Goods), CGST shall be applicable on supplies of all intra state goods or services or both subject to given exemptions and the same shall get triggered at the time of supply.

WHEREAS, the scope of "Supply" under Section 7(1) of the CGST Act is wider than the definition of Slump Sale under Section 2(42C) of the Income Tax Act, 1961, as it includes any sale, transfer, disposal, lease/license or exchange of goods or services and hence sufficient to include any sale or transfer of goods within its ambit.

HOWEVER, the term "Goods" has been defined under Section 2(52) to mean any movable property other than monies and securities. Consequently, and basis the judicial views under the previous indirect tax regime, one approach that could be argued would be to infer that GST may not be applicable on Slump Sales considering "business as a going concern" to be outside the scope of "goods".

Having said this, GST shall be applicable on any itemized sale of assets considering the fact that individual assets shall be covered under the scope of "goods" and their value can be feasibly determined. Further, the CGST Act provides for availability of credit (as mentioned herein below) in the case of itemized sales as well.

I have tried to incorporate all the issues related to Slump Sale in this Write-up. Hope the article helps.

Your feedbacks are warmly welcomed.

Thank You!

CAclubindia

CAclubindia