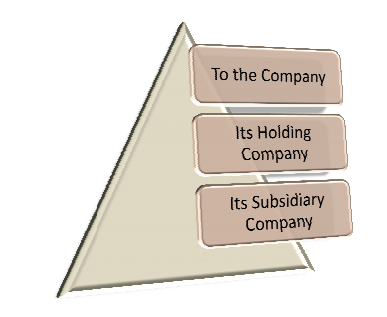

As per Provisions of Section- 144 of Companies Act, 2013, A Statutory Auditor of company can’t provide the following below mentioned services to followings:

Services which a Statutory Auditor can’t provide directly or indirectly to above mentioned Companies:

(a) Accounting and book keeping services;

(b) Internal audit;

(c) Design and implementation of any financial information system;

(d) Actuarial services;

(e) Investment advisory services;

(f) Investment banking services;

(g) Rendering of outsourced financial services;

(h) **MANAGEMENT SERVICES; AND (Its Dangerous, Must be taken care)

(i) Any other kind of services as may be prescribed. Etc.

Meaning of Following:

MANAGEMENT SERVICES: Management services means services rendered on behalf of Management, which management itself is oblige to do. E.g.

a. Preparation and filling of:

i. Income Tax Return

ii. ROC Return

iii. Service Tax Return

iv. VAT Return

v.TDS Return

vi. Excise Return

b. Maintenance of Books and Accounts

c. Preparation of Balance Sheet etc.

Above mentioned services can’t be rendered either directly or indirectly:

DIRECTLY OR INDIRECTLY:

A. In case of auditor being an individual :

i. either himself or

ii. through his relative or

iii. any other person connected or associated with such individual or through any other entity, whatsoever, in which such individual has significant influence or control, or

iv. whose name or trade mark or brand is used by such individual;

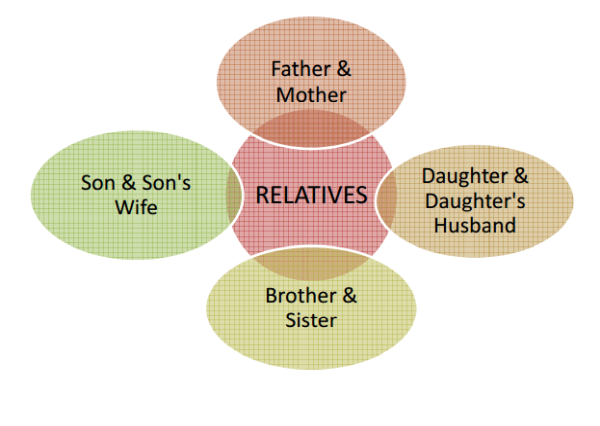

**RELATIVE MEANS:

Relatives include:

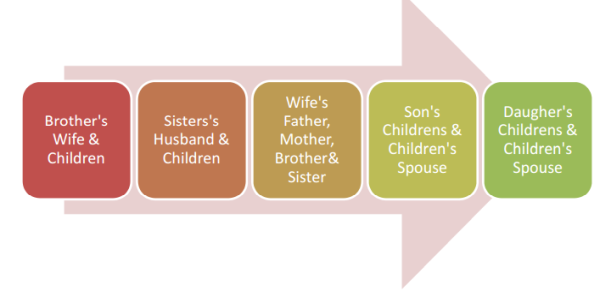

Relatives don’t include: However following are not covered under relative list:

B. In case of auditor being a firm,

i. either itself or

ii. through any of its partners or

iii. through its parent, subsidiary or associate entity or

iv. through any other entity, whatsoever, in which the firm or any partner of the firm has significant influence or control, or

v. whose name or trade mark or brand is used by the firm or any of its partners

MOST IMPORTANT:

An Statutory auditor of the company can provide the services except mentioned above “ONLY AFTER GETTING APPROVAL OF BORD OF DIRECOTRS OR AUDIT COMMITTEE”

Therefore, If Statutory Auditor want to provide service other than services not permissible u/s 144 then he need the Approval of Board of Director by passing of Resolution by board of Director in favor of auditor for providing such services.

AUDIT OF BRANCH OFFICE:

Where a company has branch office, the account of that office shall be audited by either by the statutory auditor of company or by any other person qualified for appointment as auditor of the company.

RESPONSIBILITY OF STATUTORY AUDITOR UNDER COMPANIES ACT, 2013:

A. Signing of Auditor Report: (As per Section – 145)

The person appointed as an auditor of the company shall

i. Sign the auditor‘s report; or

ii. Sign other document; or

iii. Certify any other document of the company

Note:

a) Where a firm including a limited liability partnership is appointed as an auditor of a company, only the partners who are chartered accountants shall be authorized to act and sign on behalf of the firm.

b) The qualifications, observations or comments on financial transactions or the matters, which have any adverse effect on the functioning of the company mentioned in the auditor‘s report shall be read before the company in general meeting and Open for inspection by any member of the company.

B. Attendance in General Meeting: (As per Section – 146 of Companies Act, 2013)

This Section will be applicable on all the General Meeting including Annual General Meeting.

As per Language of Section:

a. All the Notice and other Communications relating to General Meeting shall be forwarded to the Auditor of the Company.

b. The Auditor will attend all the General Meeting of the Company.

Exempted Only

When auditor will send letter for exemption from attendance in General Meeting to Company and Company will grant leave to him for not attending the General Meeting.

If auditor is not exempted by the Board then Auditor himself or his authorized representative (who shall also be qualified to be an auditor) will attend the general meeting and will heard at such meeting on any part of the business which concerns him as auditor.

CAclubindia

CAclubindia