Date: 19.03.2016

M/s. ABC LLP ( Service Provider )

M/s. XYZ Limited ( Service Recipient )

Ref: Service Tax on Works Contract and RCM

Opinion

Before giving opinion on the issues it will be useful to refer the questions related with this transaction. Assume ABC is LLP and XYZ Ltd is Body Corporate.

a. ABC LLP is a sub contractor of XYZ Limited. XYZ Ltd sub contracted Works Contract work as well as Labor work also some time.

b. Both parties would like to know the applicability and discharging method of Service Tax under Service Tax Law and under Reverse Charge Mechanism.

My Understanding View & Opinion on above

Before going ahead I have confirmed following things from both the parties.

- Contract under question is a works contract job & Labor job.

- XYZ Ltd is Principal Contractor and Body Corporate and ABC is subcontractor and LLP

- Both are located in Taxable Territory

Fact of the Case:

XYZ Limited is a Body Corporate while ABC is a LLP registered with ROC. XYZ Limited has certain contract and this contract has been further sub contracted to ABC LLP. Some of these contracts comes under definition of Works Contract and some as a Labor Contract. Now both the parties want to know the impact of VAT Chargeability on both the cases and set off mechanism.

Opinion

Before classifying any contract under works contract we should satisfy following condition as prescribed u/s of service tax which is as follows then chargeability should be applied in such referred transaction and fact of the case.

Statutory Back Ground

1- Section 65. Definitions – In this Chapter, unless the context otherwise requires, -

(105) "taxable service" means any [service provided or to be provided ],-

(zzzza) to any person, by any other person in relation to the execution of a works contract, excluding works contract in respect of roads, airports, railways, transport terminals, bridges, tunnels and dams.

Explanation.—For the purposes of this sub-clause, “works contract” means a contract wherein,—

(i) transfer of property in goods involved in the execution of such contract is leviable to tax as sale of goods, and

(ii) such contract is for the purposes of carrying out,—

(a) erection, commissioning or installation of plant, machinery, equipment or structures, whether pre-fabricated or otherwise, installation of electrical and electronic devices, plumbing, drain laying or other installations for transport of fluids, heating, ventilation or air-conditioning including related pipe work, duct work and sheet metal work, thermal insulation, sound insulation, fire proofing or water proofing, lift and escalator, fire escape staircases or elevators; or

(b) construction of a new building or a civil structure or a part thereof, or of a pipeline or conduit, primarily for the purposes of commerce or industry; or

(c) construction of a new residential complex or a part thereof; or

(d) completion and finishing services, repair, alteration, renovation or restoration of, or similar services, in relation to (b) and (c); or

(e) turnkey projects including engineering, procurement and construction or commissioning (EPC) projects;

2- 65B. Interpretations : In this Chapter, unless the context otherwise requires,–

(54) "works contract" means a contract wherein transfer of property in goods involved in the execution of such contract is leviable to tax as sale of goods and such contract is for the purpose of carrying out construction, erection, commissioning, installation, completion, fitting out, improvement, repair, renovation, alteration of any building or structure on land or for carrying out any other similar activity or a part thereof in relation to any building or structure on land;

(37) "person" includes,–– (i) an individual, (ii) a Hindu undivided family, (iii) a company, (iv) a society, (v) a limited liability partnership, (vi) a firm, (vii) an association of persons or body of individuals, whether incorporated or not, (viii) Government, (ix) a local authority, or (x) every artificial juridical person, not falling within any of the preceding sub-clauses;

3- 66E. Declared Services.-The following shall constitute declared services, namely:––

(h) service portion in the execution of a works contract;

4- 66B. Charge of Service Tax on services received from outside India.**** ] There shall be levied a tax (hereinafter referred to as the service tax) at the rate of twelve ( now fourteen ) per cent. on the value of all services, other than those services specified in the negative list, provided or agreed to be provided in the taxable territory by one person to another and collected in such manner as may be prescribed.

5- 66BA. Reference to section 66 to be construed as reference to Section 66B (1) For the purpose of levy and collection of service tax, any reference to section 66 in the Finance Act, 1994 or any other Act for the time being in force, shall be construed as reference to section 66B thereof. (2) The provisions of this section shall be deemed to have come into force on the 1st day of July, 2012.”]

6- Notification No.3/2012 - Service Tax

[TO BE PUBLISED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART II, SECTION 3, SUB SECTION (i)]

Government of India

Ministry of Finance (Department of Revenue)

New Delhi, the 17th March, 2012

Notification No.3/2012 - Service Tax

G.S.R. (E)- In exercise of the powers conferred by sub-section (1) read with subsection (2) of section 94 of the Finance Act, 1994 (32 of 1994), the Central Government hereby makes the following rules further to amend the Service Tax Rules, 1994, namely:—

1. (1) These rules may be called the Service Tax (Amendment) Rules, 2012.

(2) They shall come into force on the 1st day of April, 2012. 2. In the Service Tax Rules, 1994 (hereinafter referred to as the principal rules), in rule 2, —

“(cd) “partnership firm” includes a limited liability partnership;”

Note : Only relevant part of notification reproduced above.

7- Rule 2. Definitions –

Rule 2 (cd)- “partnership firm” includes a limited liability partnership;”].

Rule 2 (d)(i)(F) “person liable for paying service tax”,- (i) in respect of the taxable services notified under sub-section (2) of section 68 of the Act, means,- (F) In relation to services provided or agreed to be provided by way of :- (a) renting of a motor vehicle designed to carry passengers, to any person who is not engaged in a similar business; or (b) supply of manpower for any purpose; or 3 [security services]; (c) service portion in execution of a works contract by any individual, Hindu Undivided Family or partnership firm, whether registered or not, including association of persons, located in the taxable territory to a business entity registered as a body corporate, located in the taxable territory, both the service provider and the service recipient to the extent notified under sub-section (2) of section 68 of the Act, for each respectively.

8- Notification No. 30/2012-Service Tax

Government of India

Ministry of Finance

(Department of Revenue)

Notification No. 30/2012-Service Tax

New Delhi, the 20th June, 2012

GSR......(E).-In exercise of the powers conferred by sub-section (2) of section 68 of the Finance Act, 1994 (32 of 1994), and in supersession of (i) notification of the Government of India in the Ministry of Finance (Department of Revenue), No. 15/2012-Service Tax, dated the 17th March, 2012, published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i),vide number G.S.R 213(E), dated the 17th March, 2012, and (ii) notification of the Government of India in the Ministry of Finance (Department of Revenue), No. 36/2004-Service Tax, dated the 31st December, 2004, published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i), vide number G.S.R 849 (E), dated the 31st December, 2004, except as respects things done or omitted to be done before such supersession, the Central Government hereby notifies the following taxable services and the extent of service tax payable thereon by the person liable to pay service tax for the purposes of the said sub-section, namely:-

(v) provided or agreed to be provided by way of renting of a motor vehicle designed to carry passengers to any person who is not in the similar line of business or supply of manpower for any purpose or service portion in execution of works contract by any individual, Hindu Undivided Family or partnership firm, whether registered or not, including association of persons, located in the taxable territory to a business entity registered as body corporate, located in the taxable territory;

|

9. |

in respect of services provided or agreed to be provided in service portion in execution of works contract |

50% |

50% |

Explanation-II. - In works contract services, where both service provider and service recipient is the persons liable to pay tax, the service recipient has the option of choosing the valuation method as per choice, independent of valuation method adopted by the provider of service.

Note : Only relevant part of notification reproduced above.

9- MY Analysis

If we see the above statutory provisions in chronological order you will find that

Section 65(105)(zzzza), which is chargeable as per section 66, establish the taxability on works contract and its explanation define the works contract also

Section 65B(54) again interpret the Works Contract, unless the context otherwise require

Section 65B(37) again interpret the Person, unless the context otherwise require and in this sub section clause (v) Limited Liabaility Partnership define separately from Firm which is defined in sub clause (vi). It means unless the context otherwise require both has distinction as per Section 65B(37)

Section 66E(h) define the works contract service as a declared services

On 17.03.2012, Through Notification no 3, dated 17.03.2012 Central Government notify the changes in rule 2 of definition and as per this changes, Rule 2(cd) state “partnership firm” includes a limited liability partnership;” Now as per this notification when context is otherwise required, LLP should be intent as a firm for the context required w.r.t. Rule 2(d)(i)(F).

On 20.06.2012, Through notification no 30/2012 dated 20.06.2012 Central Government notify the reverse charge mechanism in certain taxable services and redefine the person liable to pay service tax and make liable to pay service recipient also. In case of works contract it is 50:50 between service provider and service receiver. In this notification if works contract service provided by any individual, HUF or partnership firm, whether registered or not, including AOP, located in the taxable territory to a business entity registered as body corporate, located in the taxable territory. This notification came after notification no 3 dated 17.03.2012 which enabling the LLP to be understood as a partnership firm unless the context otherwise required. So for this notification LLP to be understood as Partnership firm hence reverse charge mechanism referred in this notification for firm to be read as it is applicable on LLP also, if he provides the service to body corporate. The extent of payable define in this notification in case of works contract, between LLP & Body corporate is 50:50.

We should note that RCM is applicable on certain services on service recipient because of “service recipient” define as a person liable to pay service tax under statute, hence even 100% taxes paid by service provider, service recipient himself shall not be free from this liability, he has to pay off his part irrespective of billing done by SP. Hence it is highly advisable that SP to be educated about how to bill.

10- If we summarize the above analysis in table format then it will be as follows

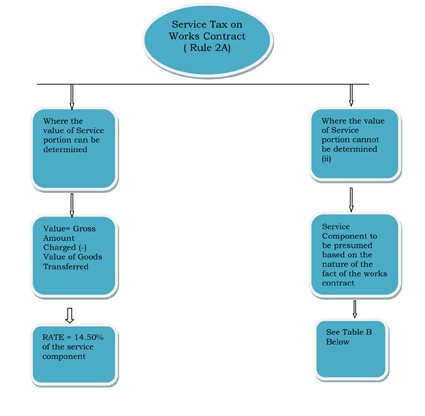

However table look in notification 30/2012 very simple, it should be noted that the ST is applicable on a composite works contract, only on the service component of the transaction and not on goods. Hence In order to determine the service component , Rule 2A of the Service Tax (Determination of Value) Rules,2012 has been amended with effect from 01.07.2012. The following chart explains the tax liability in case of composite transaction of works contracts:

11- Table B : Exact effect on SP & SR

|

Sr. No |

Situation |

Service Provider |

Service Recipient |

||

|

Component of Tax Liability Payable |

Effective Tax rate payable w.e.f.01.06.2015 |

Component of Tax Liability Payable |

Effective Tax rate payable w.e.f.01.06.2015 |

||

|

1. |

Where the service value is determined by the service provider ( irrespective of the nature of the works contract) 100% Service Value*14.50%*50%=7.25% |

50% |

7.25% of the identified service component |

50% |

7.25% of the identified service component |

|

2. |

Where the service value is not determined by the service provider (“presumptive option”) and the works contract is of the original works ( 40%*14.50%*50% = 2.90% |

50% |

2.90% of the gross amount (including free issue materials) |

50% |

2.90% of the gross amount (including free issue materials) |

|

3. |

Presumptive Option in respect other work contracts 70%*14.50%*50% = 5.075% |

50% |

5.075% of the gross amount ( including free issue materials) |

50% |

5.075% of the gross amount ( including free issue materials) |

Note 1 : For Clarity Following Services to be not read as a Works Contract

< > If pure labour service are provided, then the same won’t be covered under works contract category;If only material is provided, then again it would not be covered under works contract category as not being a service only.If separate divisible contracts are issued for supply of material and supply of services, the same is not a works contract and again it won’t be covered under the works contract category

Note 2 : Clarity on Supply of Manpower does not come under works contracts however some confusion exist between Supply of Manpower and labor charges.

< > Supply of Manpower as well as Labor Charges both are subject to service taxHowever under RCM there is distinction between Supply of Manpower & Labor Charges and Both are not similarRCM is applicable on Supply of Manpower and on Labor Charges FCM is applicableSo for billing ABC LLP has to test whether the services provided is coming under Supply of Manpower or Pure labor Charges, accordingly RCM should be applied otherwise FCM will be applied.In case of RCM on Supply of Manpower, if service provider is Individual, Firm, AOP or LLP as referred in said above notification, 100% tax shall be payable by Service Recipient.

< > Being ABC, a LLP and XYZ Ltd a Body Corporate, RCM is applicable in case of notified services provided by ABC LLP being Service Provider to XYZ Ltd who is Service Recipient.Any Transaction between ABC & XYZ to be tested whether it is Works Contract, Labor Job or Supply of Manpower or any notified service as mentioned in notification no 30.If it is Labor Job FCM will apply and service tax to be charged as 14.50% or as the rate from time to time prescribed.If it is works contract, taxable value shall be determined as per Rule 2A which is certain % of total value according to the nature, for detail of taxable value please refer table B here. After determining this taxable value it will be divided between SP & SR in 50:50 ratio which is current ratio prescribed.And after this division both the parties will charge service tax @ 14.50% on own part, which is current rate prescribed. For effective rate please refer Table B.So Total Value > Service Taxable Value > Division Between SP & SR > Apply ST rateIn works contract services, where both service provider and service recipient is the persons liable to pay tax, the service recipient has the option of choosing the valuation method as per choice, independent of valuation method adopted by the provider of service.We should note that RCM is applicable on certain services on service recipient because of “service recipient” define as a “Person liable to pay Service Tax” under statute, hence even 100% taxes paid by service provider, service recipient himself shall not be free from this liability, he has to pay off his part irrespective of billing done by SP. Hence it is highly advisable that SP to be educated about how to bill.Same Relationship and Opinion will follow if in case of Works Contract when Service Provider is Individual, HUP, Firm or AOP and receiver is Body Corporate.

This opinion is provided on knowledge sharing basis which I have as per my best of knowledge study and understanding. This opinion does not create or establish any advise, direction and/or instruction to any one to follow as per the said opinion. This I want to clear that, I will not be personally liable or indemnify to company or to any, if authority take another view. Any one are free to follow as per its own best judgment. This is to confirm that we have not covered the Recent Central Budget 2016 impact on this draft.

The author can also be reached at pankaj@anpllp.com

CAclubindia

CAclubindia