Eligibility:

- An assessee to whom sec 44AB is applicable

- GTI includes PGBP

Intellectual:

Individual engaged in business of garments and turnover for FY 2016-17 exceeds Rs 1 crore. As he is liable for tax audit under section 44AB, he is eligible for deduction u/s 80JJAA.

Deduction allowed: 30% of additional employee cost in the previous year

Period of deduction: 3 AY's including AY in which employment is provided

Assessee not covered:

- Companies formed by splitting up or the reconstruction of an existing business

- Transfer from any other person or as a result of any business reorganization

Accountant certificate: Rule 19AB requires assessee to filed Form10AD along with return of income. Form 10DA shall be furnished electronically.

Intellectual:

X co., engaged in manufacturing of automobile parts and also is involved in international transactions. As per Income tax return, last date of filing of income tax return is 30th Nov 2017 and hence, if X co decides to claim deduction u/s 80JJAA then Form 10DA needs to submit by 30th Nov 2017.

Fundamentals to be kept in mind:

a) Additional employee cost: total emoluments paid /payable to additional employees employed during the PY. Additional employee cost in different scenarios

|

Existing business |

New business |

|

There should be increase in number of employees when compared to number of employees as on previous year ending emoluments to be paid through account payee cheque or account payee bank draft or ECS through bank a/c |

Emoluments paid or payable to employees during the previous year in which incorporated, shall be deemed employee cost |

Intellectual:

Y co., incorporated on 1st April 2013.

- As on 31/3/17 there are 100 employees and during the year 17-18 50 employees were appointed and 15 employees resigned - as there is increase of 35 employees, deduction u/s 80JJAA shall be available

- If there are 50 new appointment and resignation is also of 50 employees, no deduction shall be available

b) Emoluments: any sum paid or payable paid to employee in lieu of employment except:

- Contribution to Pension fund or provident fund or any other fund by employer

- Termination benefits given by employer

c) Additional Employees: An employee employed during the year and exists as on last day of preceding year and does not include:

- Employee with total emoluments exceeding Rs 25000 per month

- Contribution to Employee pension scheme is paid by Government

- Employee do no participate in RPF

- Employee is employed for a period of less than 240 days (150 days in case of manufacturing apparel)

Intellectual:

Z co, hires both regular and casual employees during FY 2016-17. On satisfying all other conditions, whether regular and casual employees can be considered as additional employee?

Casual workers do not participate in RPF, hence cannot be included in additional employee

Illustration:

Mr. A has commenced the business of manufacture of computers on 1.4.2017.

He employed 450 new employees during the P.Y. 2017-18, the details of whom are as follow

|

Sl.no |

No. of employees |

Date of employment |

Regular / Casual |

Total monthly emoluments per employee (Rs) |

|

1. |

75 |

1.4.2017 |

Regular |

24,000 |

|

2. |

125 |

1.5.2017 |

Regular |

26,000 |

|

3. |

150 |

1.8.2017 |

Casual |

17,000 |

|

4. |

100 |

1.9.2017 |

Regular |

24,000 |

The regular employees participate in recognized provident fund while the casual employees do not. Further, out of 75, 125 & 100 regular employees employed on 1.4.2017, 1.5.2017 & 1.9.2017, only 40, 30 & 60 qualify as a 'workman' under the Industrial Disputes Act, 1947.

Compute the deduction, if any available to Mr. A for A.Y. 2018-19, if the profits & gains derived from manufacture of computers that year is Rs. 75 lakhs & his total turnover is Rs. 2.16 crores.

Solution: Mr. A is eligible for deduction u/s 80JJAA, since he is subject to tax audit u/s 44AB for A.Y. 2018-19, as his total turnover from business exceeds Rs. 1 crore & he has employees 'additional employees' during P.Y. 2017-18.

Additional employee cost = Rs. 24000*12*75 [Working Note*] = Rs. 2,16,00,000/-

Deduction u/s 80JJAA = Rs. 30% of Rs. 2,16,00,000/- = Rs. 64,80,000/-

*Working Notes:

|

Particulars |

No. of workmen |

|

|

Total no. of employees employed during year |

450 | |

|

Less: Casual employees employed on 1.8.2017 who do not Participate in Recognized provident fund |

150 | |

|

Regular employees employed on 1.5.2017, since their total monetary emoluments exceed Rs. 25,000 |

125 | |

|

Regular employees employed on 1.9.2017 since they have been employed for less than 240 days in P.Y 2017-18. |

100 | |

|

Number of 'Additional employees'. |

75 | |

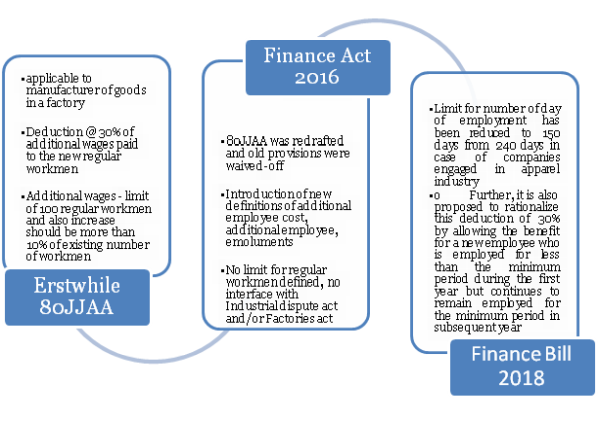

80JJAA - THEN AND NOW

MIND TWISTER

a) As per definition of additional employee, it has been specified that deduction shall be available for employees who are employed during the year and whose employment result in increase of total number of employees as on the last day of preceding year:

In case of A co., total employees recruited during the year was 50 regular employees and 15 employees resigned during the year, hence benefit of 80JJAA shall be available only for 35 employees. The section is not clear as to which 35 employees will be selected for deduction? This leaves a grey area which can be challenged by the assessing officer.

b) If the employees who have resigned are out of employees who were existing as on last day of preceding year then, whether for the purpose of deduction u/s 80JJAA, additional employee would be reduced accordingly?

CAclubindia

CAclubindia