Securities and Exchange Board of India vide circular dated November 26, 2018, introduced the new borrowing framework for the large entities in order to bring into the effect announcement made under the Union Budget for 2018-19.

The Union Budget for 2018-19 which inter alia include the following announcement 'SEBI will also consider mandating, beginning with the large entities, to meet about one-fourth of their financing needs from the debt market'.

The budgetary announcement by the Government and subsequent circular by the SEBI has been bought in order to develop the bond market in India. However, this announcement is not an independent event since the Government has already taken series of steps in consultation with different regulators to develop the bond market in India and to reduce the over-reliance on the Bank for corporate funding.

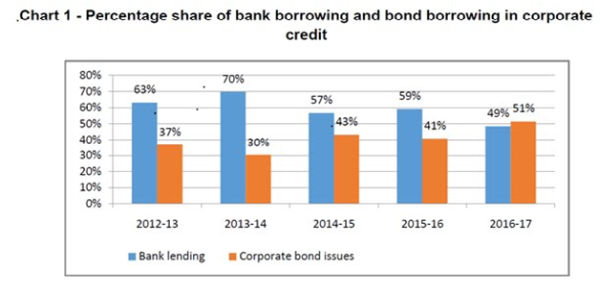

Though the past steps are showing a result and bond market is gradually improving in India with a steady growth of bond financing over the bank financing and the same can be understood through the chart below.

Source: CARE Ratings, SEBI

As we can see, in the financial year 2016-17, bond financing overtook the bank lending, so in order to provide further impetus to the bond market Government came up with this announcement.

Apart from developing the Bond market in India other probable reasons might include growing NPAs in Bank and recent banking frauds. This framework might help banks in releasing the pressure created due to high demand for bank financing which also causing the concentration of risk in the banking system.

Though the RBI with a view to addressing concentration risk in the banking system has come up with the policy framework on banks’ large exposure.

The framework involves mandating enhanced provisioning norms for banks’ exposure to large borrowers. These enhanced provisioning norms have come into effect from the financial year 2018-19.

Another leap forward in this regard and truly a game changer for the creditors was the enactment of the Insolvency and Bankruptcy Code, 2016. IBC provides a quick and efficient process both for rehabilitation and insolvency of the company.

In the backdrop of all this development, the Government has announced its intention of mandating large entities to raise 1/4th of their incremental borrowing need through debt instruments.

Further, in order to execute the announcement made by the Government in the budget of 2018-19 SEBI came up with the circular dated November 26, 2018, mandating the large entities to raise 25% of their incremental borrowing in the financial year through debt financing.

WHAT IS FRAMEWORK ALL ABOUT

As per para 3.1 of the circular, a listed entity recognized as large corporate shall raise not less than 25% of incremental borrowing, during the financial year subsequent to the financial year in which it is identified as a large corporate by way of issuance of debt securities, as defined under SEBI( Issue and Listing of Debt Securities) Regulation, 2008.

Before moving further we need to discuss three terms used in the framework i.e. Large Corporate, Incremental Borrowing and Debt securities as defined under SEBI (Issue and Listing of Debt Securities) Regulation, 2008

LARGE CORPORATE

The framework shall be applicable for all the listed entities ( except for Scheduled Commercial Bank), which as on last day of the Financial Year (i.e. March 31 or December 31):

(Note: On last day of the previous year these conditions need to be fulfilled simultaneously)

1. Have their specified securities or debt securities or non-convertible redeemable preference share, listed on a recognized stock exchange(s) in terms of SEBI(LODR) Regulation, 2015; and

2. Have an outstanding long term borrowing of Rs. 100 crores or above, where outstanding long term borrowing shall mean any outstanding borrowing with original maturity of more than 1 year and shall exclude external commercial borrowings and inter-corporate borrowings between a parent and subsidiaries.

3. Have a credit rating of 'AA and above', where credit rating shall be of the unsupported bank borrowing or plain vanilla bond of an entity, which have no structuring/support built in; and in case, where issuer has multiple rating from multiple rating agencies, highest of such rating shall be considered for the purpose of applicability of this framework.

# Specified Securities means equity share and convertible security as defined under clause (zj) of sub-rule (1) of regulation 2 of SEBI (ICDR) Regulation, 2009.

## Unsupported Bank Borrowing: A supported bank borrowing is the borrowing backed by the collateral or any other kind of security for repayment, so unsupported bank borrowing is the unsecured borrowing.

### Vanilla Bond or straight bond is a bond having a fixed coupon rate and fixed maturity period and redeemable at face value.

INCREMENTAL BORROWING

Incremental borrowing shall mean any borrowing done during a particular financial year, of original maturity of more than 1 year, irrespective of whether such borrowing is for refinancing/repayment of existing debt or otherwise and shall exclude external commercial borrowing and inter-corporate borrowings between a parent and subsidiary(ies).

It is to be noted that these borrowings have been explicitly kept out of the preview of the framework.

External Commercial Borrowing;

Inter-corporate borrowing between a parent and subsidiary;

Any loan having an original maturity period of less than 1 year;

Debt Securities

'Debt Securities' means a non-convertible debt securities which create or acknowledge indebtedness, and include debenture, bond and such other securities of body corporate or any statutory body constituted by virtue of legislation, whether constituting change on the assets of the body corporate or not, but excludes bonds issued by Government or such other bodies as may be specified by the Board, securities receipt and securitized debt instrument.

APPLICABILITY OF FRAMEWORK

For the large corporate following April-March as their financial year, the framework shall come into effect from April 1st, 2019.

For the large corporate following calendar year as their financial year, the framework will become applicable from January 1st, 2020.

For this framework, the financial year shall mean April-March or January-December, as may be followed by the entities.

It is further explained in the circular, the financial year 2020 mean period starting from April 1st, 2019 and ending on March 31st, 2020 and for those following calendar year as their financial year, it means the period starting from January 1st, 2020 and ending on December 31st, 2020.

The framework will be effective from the financial year 2020, i.e. all the entities falling under the definition of 'Large Corporate' as on 31st March 2019 or 31st December 2019, as the case may be, shall abide the framework from the financial year 2020.

However, it is to be noted that for first two financial year that is 2020 and 2021, the requirement of meeting the incremental borrowing norm shall be applicable on annual basis and accordingly listed entity identified as a Large Corporate on last day of financial year 2019 or financial year 2020, shall comply with the requirement by the last day of the subsequent financial year 2020 or financial 2021, as the case may be.

Let’s take an example, A company XYZ Limited, having its equity shares are listed on both stock exchanges i.e. BSE and NSE. They have also have unsupported bank borrowing and credit rating for the same is AA. The outstanding borrowing as on the 31st day of March 2019, is 1000 crore.

So since XYZ Limited is fulfilling all the three conditions required for being large corporate, hence XYZ is Large corporate and hence framework is applicable on XYZ limited for the financial year 2020, however, it is to be noted that these three conditions need to be checked on the last day of every financial year.

|

Current Financial Year |

2020 |

2021 |

|

|

Outstanding borrowing as on last day of PFY |

1000 |

1200( it is to be assumed we have paid 200 crore during the PFY |

|

|

Whether framework applicable |

Yes, since all the three conditions are met. |

Yes, since all the three conditions are met. |

|

|

A |

Incremental Borrowing in CFY |

400 |

500 |

|

B |

Mandatory borrowing through debt securities in the CFY |

100 |

125 |

|

C |

Actual Borrowing done through debt securities in the CFY |

50 |

150 |

|

D |

Shortfall in mandatory borrowing. (B-C) |

50 |

NIL |

|

Compliance Status |

Shortfall, hence explanation to be provided |

Complied with the requirement |

|

|

PFY= Previous Financial Year, CFY= Current Financial Year |

|||

From the financial year 2022, the requirement of 25% mandatory incremental borrowing through pure debt instruments by a large corporate in a financial year will need to be met over a contiguous block of 2 years. Hence if the company is large corporate as on last day of the financial year 2021 i.e. 31st day of March 2021, and company do incremental borrowing in the financial year 2022 than the company shall do 25% of incremental borrowing through pure debt instruments by last day of the financial year 2023.

So the listed entity identified as large corporate, as on last day of 'T-1' shall fulfil the requirement of incremental borrowing for the financial year 'T' over the financial year 'T' and 'T+1'.

|

Current Financial Year |

2022 |

2023 |

2024 |

2025 |

|

|

Outstanding borrowing as on last day of PFY |

800 |

400 |

80 |

120 |

|

|

Whether framework applicable |

Yes |

Yes |

No, because since outstanding borrowing is less than 100 crore |

Yes |

|

|

A |

Incremental Borrowing in CFY |

400 |

200 |

40 |

100 |

|

B |

Mandatory borrowing through debt securities in the CFY |

100 |

50 |

10 |

25 |

|

Block for compliance of the mandatory borrowing through debt securities |

FY 2022-23 |

FY 2023-24 |

N.A |

FY 20235-26 |

|

|

C |

Actual Borrowing done through debt securities in the CFY |

50 |

75 |

10 |

25 |

|

D |

Shortfall of PFY(For the first year of the previous block) carried forward to CFY. |

- |

50 |

25 |

NIL |

|

E |

Quantum of (D) which has been met from © |

- |

50 |

25 |

NIL |

|

F |

Shortfall, if any, in the mandatory borrowing for CFY.(B)-[©-(E)] |

50 |

25 |

NA |

NIL |

|

Fine, to be paid{in case the shortfall of PFY, if any, is not adjusted completely against the debt securities borrowings of CFY} .2%[(d)-(e)] |

NIL |

NIL |

.2% of 15 crore= 3 lakhs |

NIL |

|

|

Compliance Status |

For PY-NA For CFY- Shortfall to be carried forward to next fy. |

For PFY- Carried forward to be adjusted and for CFY- shortfall to be forwarded |

For PFY- carried forward amount to be adjusted for unadjusted amount fine to be paid to the selected stock exchange |

For PFY-NA and for CFY- no carried forward |

DISCLOSURE REQUIREMENT FOR LARGE CORPORATE

A listed entity identified as a large corporate shall make the following disclosures to stock exchange(s), where its securities are listed.

1. Within the 30 days from the beginning of the financial year subsequent to the financial year on the last day of which listed entity is identified as large corporate. Disclosure to be made in Annexure-A.

2. Within 45 days of the end of the financial year, the detail of the incremental borrowing done during the financial year, in the format as provided at Annexure-B1 and B2.

These disclosures are to be certified by both CFO and CS of the Large Corporate.

Further, these disclosures shall also form part of the audited annual financial statement.

All these disclosures made to stock exchange shall be collected by the stock exchange and stock exchange shall further submit it to the SEBI within 14 days from the last date of submission of annual financial result.

IN CASE OF DEFAULT

While reading the consultation paper it is clear that the consultation paper recommends a 'Comply or explain' for initial two years and after that penalty will be imposed. The final circular in on the same line and provide that for the financial year 2020 and 2021, in case of default the company shall explain for such shortfall to the stock exchange.

From the financial year 2022, if at the end of two years i.e. last day of the financial year 'T+1' there is a shortfall in the requisite borrowing i.e. borrowing through pure debt instrument is less than 25% of total incremental borrowing made in the financial year T then monetary penalty of .2% of the shortfall in the borrowed amount shall be levied and same shall be paid to the stock exchange chosen by the company for the same.

The author can also be reached at nishantmishra008@gmail.com

CAclubindia

CAclubindia