Meaning of Inverted Duty structure

Word Inverted Duty Structure is not defined in GST. However when Rate of tax on INPUTS being higher than the rate of tax on output supplies then same would be treated as Inverted Duty Structure. So now the question come whether we are entitle to take the refund of such excess input.

Refund of Unutilised Input Tax Credit

Sec 54(3) of CGST Act Subject to the provisions of sub-section (10), a registered person may claim refund of any unutilised input tax credit at the end of any tax period:

Provided that no refund of unutilised input tax credit shall be allowed in cases other than-

(i) Zero rated supply

(ii) where the credit has accumulated on account of rate of tax on INPUTS being higher than the rate of tax on output supplies (OTHER THAN NIL RATED OR FULLY EXEMPT SUPPLIES), except supplies of goods or services orboth as may be notified by the Government on the recommendations of the Council:

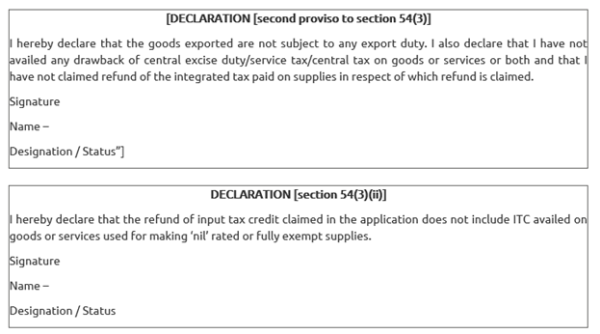

Provided further that no refund of unutilised input tax credit shall be allowed in cases where the goods exported out of India are subjected to EXPORT DUTY:

Provided also that no refund of input tax credit shall be allowed, if the supplier of goods or services or both avails of drawback in respect of central tax or claims refund of the integrated tax paid on such supplies.

How to calculate the Refund

Rule 89:-Application for refund of tax, interest, penalty, fees or any other amount-

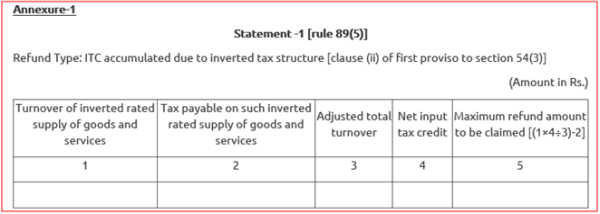

[(5) In the case of refund on account of inverted duty structure, refund of input tax credit shall be granted as per the following formula:-

Formula Maximum Refund Amount = {(Turnover of inverted rated supply of goods and services) x Net ITC ÷ Adjusted Total Turnover} - tax payable on such inverted rated supply of goods and services.

Explanation:-For the purposes of this sub-rule, the expressions -

(a) Net ITC shall mean input tax credit availed on INPUTS during the relevant period other than the input tax credit availed for which refund is claimed under sub-rules (4A) or (4B) or both; and

[Adjusted Total turnover" and "relevant period" shall have the same meaning as assigned to them in sub-rule (4).]]

Important Note - Earlier in the meaning of NET ITC Input and Input Service both were included. This Rule 89(5) has been amended retrospectively from 1.7.2017 vide Notification No. 21/2018-Central Tax dated 18.4.2018 and Notification No.26/2018-Central Tax dated 13.6.2018. Contentions are raised in the Gujrata High Court in case of Quarry Owners Association vs Union of India based on grounds of challenge that impugned amended Rule 89(5) denies the benefit of refund of unutilized input tax credit is illegal.

As per Rule 89(4) meaning of

(D) "Turnover of zero-rated supply of services" made without payment of tax under bond or LUT, to be calculated in the following manner, namely:-

Aggregate of the payments received during the relevant period for zero-rated supply of services

Add

where supply has been completed for which payment had been received in advance in any period prior to the relevant period

Less

Advances received for zero-rated supply of services for which the supply of services has not been completed during the relevant period.

(E) 'Adjusted Total Turnover' means the sum total of the value of-

(a) the turnover in a State or a Union territory, as defined under clause (112) of section 2, excluding the turnover of services; and

To view / enroll the course on GST by the author: Click Here

(b) the turnover of zero-rated supply of services determined in terms of clause (D) and non-zero-rated supply of services, excluding-

(i) the value of exempt supplies other than zero-rated supplies; and

(ii) the turnover of supplies in respect of which refund is claimed under sub-rule (4A) or sub-rule (4B) or both, if any, during the relevant period.]

(F) 'Relevant period' means the period for which the claim has been filed.

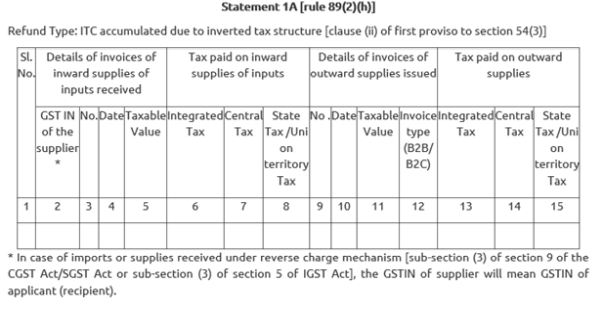

Statement as per Rule 89(2)(h) of CGST Rule 2017-

A statement containing the number and the date of the invoices received and issued during a tax period in a case where the claim pertains to refund of any unutilised input tax credit

List of Goods/Services on which Refund is not allowed due to inverted duty structure

|

S.No |

Particular |

|

|

Services |

||

|

1 |

No refund of unutilized input tax credit shall be allowed under section 54 (3) in case of supply of services specified in sub-item (b) of item 5 of Schedule II of the CGST Act. That is Construction Service. |

|

|

Goods |

||

|

1. |

5007 |

Woven fabrics of silk or of silk waste |

|

2. |

5111 to 5113 |

Woven fabrics of wool or of animal hair |

|

3. |

5208 to 5212 |

Woven fabrics of cotton |

|

4. |

5309 to 5311 |

Woven fabrics of other vegetable textile fibres, paper yarn |

|

5. |

5407, 5408 |

Woven fabrics of manmade textile materials |

|

6. |

5512 to 5516 |

Woven fabrics of manmade staple fibres |

|

1[6A |

5608 |

Knotted netting of twine, cordage or rope; made up fishing nets and other made up nets, of textile materials |

|

6B |

5801 |

Corduroy fabrics |

|

6C |

5806 |

Narrow woven fabrics, other than goods of heading 5807; narrow fabrics consisting of warp without weft assembled by means of an adhesive (bolducs)]. |

|

7. |

60 |

Knitted or crocheted fabrics [All goods] |

|

8. |

8601 |

Rail locomotives powered from an external source of electricity or by electric accumulators |

|

9. |

8602 |

Other rail locomotives; locomotive tenders; such as Diesel-electric locomotives, Steam locomotives and tenders thereof |

|

10. |

8603 |

Self-propelled railway or tramway coaches, vans and trucks, other than those of heading 8604 |

|

11. |

8604 |

Railway or tramway maintenance or service vehicles, whether or not self-propelled (for example, workshops, cranes, ballast tampers, trackliners, testing coaches and track inspection vehicles) |

|

12. |

8605 |

Railway or tramway passenger coaches, not self-propelled; luggage vans, post office coaches and other special purpose railway or tramway coaches, not self-propelled (excluding those of heading 8604) |

|

13. |

8606 |

Railway or tramway goods vans and wagons, not self-propelled |

|

14. |

8607 |

Parts of railway or tramway locomotives or rolling-stock; such as Bogies, bissel-bogies, axles and wheels, and parts thereof |

|

15. |

8608 |

Railway or tramway track fixtures and fittings; mechanical (including electro-mechanical) signalling, safety or traffic control equipment for railways, tramways, roads, inland waterways, parking facilities, port installations or airfields; parts of the foregoing |

[No.20/2018-Central Tax (Rate)] Dated: 26th July, 2018

In the notification No.5/2017-Central Tax (Rate), in the opening paragraph the following proviso shall be inserted, namely:-

[Provided that,-

(i) nothing contained in this notification shall apply to the input tax credit accumulated on supplies received on or after the 1st day of August, 2018, in respect of goods mentioned at serial numbers 1, 2, 3, 4, 5, 6, 6A, 6B, 6C and 7 of the Table below; and

(ii) in respect of said goods, the accumulated input tax credit lying unutilised in balance upto the month of July, 2018, shall lapse.]

Comment - From 1st Aug 2018 the Sr No 1 to 6 has been removed which means after 1st Aug 2018 refund will be permitted for those items due to inverted duty structure. However this notification not allows taking the refund of credit lying as on 31st July.

In case of Shabnam Petro filsPvt. Ltd.Vs union of India Gujarat High Court has ordered that, proviso (ii) of the opening paragraph of the Notification No.05/2017-C.T. (Rate) dated 28.06.2017, inserted vide Notification No.20/2018-C.T.(Rate) dated 26.07.2018, is ex-facie invalid and liable to be strike down as being without any authority of law.

To enrol for the GST course by the author in Hindi Click Here

CAclubindia

CAclubindia