This section lays down the provisions relating to providing loans to any person or other body corporate, giving any guarantee or providing security in connection with a loan to any other body corporate or any person, and acquiring by way of subscription, purchase or otherwise, the securities of any other body corporate. We can say this is basically relating to flow of investment from a company to any other body corporate or person. This section has been notified on 01st April, 2014 and further amendments have been introduced in this section and its related rules at different occasions.

Section 186(1):

This sub-section starts with the phrase 'without prejudice to the provisions contained in this Act' which implies that while complying this provision, we need to take care of the other provisions of the Act (Companies Act, 2013) also. This provision is dependent to other provisions contained in the law, even if other provisions provide to the contrary. In case there is any inconsistency or a departure between the two provisions, interpretation has to be constituted with the doctrine of harmonious construction.

Further, the provisions also adds a restriction that 'unless otherwise prescribed' which implies that provision of this sub-section is applicable only when there is no other contrary provision prevailing in the Act. In case, there is a differing provision to this sub-section, the differing provision shall prevail over this.

Both the above phrases conclude that while reading this provision, the reader has to consider other provisions of the Act also. It can be stated that the given provision i.e. Section 186(1) is not a non-obstante clause and it has to take into consideration other provisions of the Act also and comply with them simultaneously.

The sub-section states that a company shall unless otherwise prescribed, make investment through not more than two layers of the investment companies.

Here, we need to understand the meaning of investment companies.

The expression 'investment company' means a company whose principal business is the acquisition of shares, debentures or other securities and a company will be deemed to be principally engaged in the business of acquisition of shares, debentures or other securities, if its assets in the form of investment in shares, debentures or other securities constitute not less than fifty per cent. of its total assets, or if its income derived from investment business constitutes not less than fifty per cent. as a proportion of its gross income.

In the given definition, investment company has been defined as the company whose principal business is the acquisition of shares, debentures or other securities. Further, it is important to understand that a company shall deemed to be engaged in the business of acquisition of shares, debentures or other securities if it satisfies any of the following two conditions:

i) Asset of the company in the form of investment in the securities is not less than 50% of the total assets of the company; or

ii) Income derived from the investment business is not less than 50% of the gross revenue.

The provision can be understood with an example:

There are four companies A Ltd., B Ltd., C Ltd. and D Ltd. and all are investment companies.

In this case,

- A Ltd. can make investment in B Ltd.;

- A Ltd can make investment in C Ltd. through B Ltd.

- but A Ltd. cannot invest in D Ltd. though B Ltd. and C Ltd.

EXCEPTIONS:

Provisions of Section 186(1) shall not apply to-

1. a company from acquiring any other company incorporated in a country outside India if such other company has investment subsidiaries beyond two layers as per the laws of such country.

The exceptions says that if a company wants to make investment in any company incorporated outside India and the investee company has further investment subsidiaries more than two layers in accordance with the law of the foreign country, the Indian company shall be allowed to make such investment.

Example: If A Ltd. (which is incorporated under the Indian Law) makes investment in other company i.e. B Inc. (which is incorporated under the laws of any other country) and B Inc. has already investment in further two layers of the investment companies i.e. C Inc. and D Inc., it will not attract the provisions of this sub-section and such investment shall be allowed.

2. a subsidiary company from having any investment subsidiary for the purposes of meeting the requirements under any law or under any rule or regulation framed under any law for the time being in force. A subsidiary company can have an investment company as a subsidiary for the purpose of meeting any legal requirement.

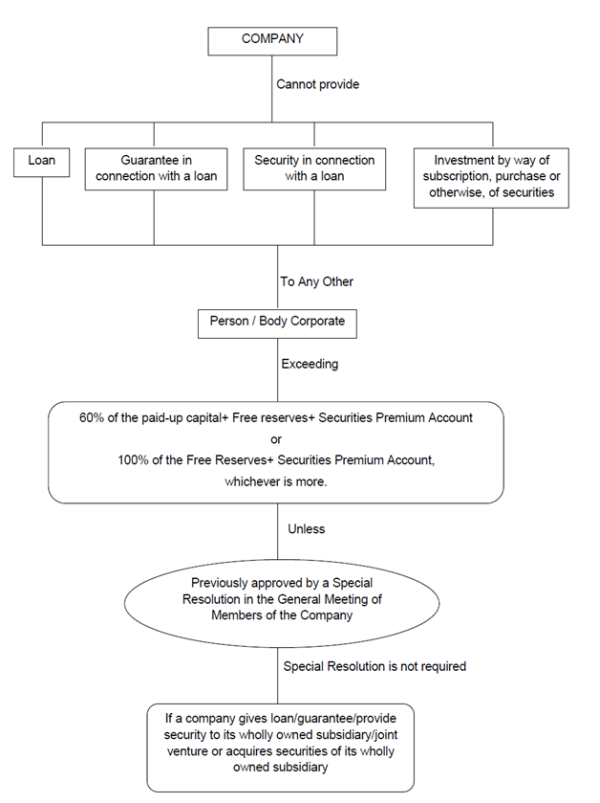

Section 186(2):

No company shall directly or indirectly-

a) give any loan to any person or body corporate;

b) give any guarantee or provide security in connection with a loan to any other body corporate or person; and

c) acquire by way of subscription, purchase or otherwise, the securities of any other body corporate,

exceeding 60% of the paid-up capital+ Free reserves+ Securities Premium Account or 100% of the Free Reserves+ Securities Premium Account, whichever is more.

Here it is to be noted that 'person' does not include an employee of the company.

Section 186(3):

Where the limit prescribed under section 186(2) i.e. the aggregate of the loans and investment so far made, the amount for which guarantee or security so far provided to or in all other bodies corporate along with the investment, loan, guarantee or security proposed to be made or given by the Board, exceeds, the investment is required to be previously approved by passing a special resolution in the general meeting of the members of the company.

A resolution passed at a general meeting to give any loan or guarantee or investment or providing any security or the acquisition under sub section (2) of section 186 shall specify the total amount up to which the Board of Directors are authroised to give such loan or guarantee, to provide such security or make such acquisition.

One exemption has been provided under the sub-section that if a company gives loan or guarantee or provide security to its wholly owned subsidiary company or a joint venture company or acquires securities of its wholly owned subsidiary company, the requirement of special resolution shall not be applicable.

Section 186(4):

The company shall disclose the full details of loan, guarantee or security provided and the purpose for which it has been provided in its financial statements.

Section 186(5):

The Board Resolution shall be passed by all the directors present in the Board Meeting conducted for making of investment, giving of loan or guarantee or providing of security by the company. Further, the prior approval of public financial institutions is also required in case there is any default in repayment of any loan, investment or interest thereon and the limit prescribed under sub-section (2) has been exceeded.

Section 186(6):

No company, which is registered under section 12 of SEBI Act, 1992 and covered under such class of company as may be prescribed, shall take inter-corporate loan/deposit exceeding the prescribed limit. Details of such loan etc. shall be disclosed in the financial statements of the company.

1. What are section 12 companies?: Stock-broker, sub-broker, share transfer agent, banker to an issue, trustee of trust deed, registrar to an issue, merchant banker, underwriter, portfolio manager, investment adviser and such other intermediary who may be associated with securities market are required to be registered under section 12 of SEBI Act, 1992 for operating in securities market.

2. What are prescribed companies?: No company has been prescribed yet.

Thus, it is implied that any company, which is registered under section 12 of the SEBI Act, 1992 and covered under class of companies notified by the Government in this regard, shall not take inter-corporate loan/deposit exceeding the limit prescribed under sub-section (2) of Section 186.

Section 186(7):

Loan shall be given at a rate of interest not lower than the prevailing yield of 1 year/3 years/5 years to 10 years of Government securities.

What is prevailing yield of govt. securities? : The yield is the interest rate that the Government pays on the purchase of Government Securities for different lengths of time. Each of the Government securities has a different yield.

The company needs to take into consideration the Government Security yield closest to the tenor of the loan.

Section 186(8):

A defaulting company in the repayment of any deposit or interest thereon shall not provide any loan/guarantee/security till the time such default is subsisting.

Section 186(9): Register of investment:

a) Every company, making loan or investment, shall maintain a register of investment from the date of its incorporation in Form MBP-2.

b) The company shall enter complete particulars of loans and guarantees given, securities provided and acquisitions made by the company.

c) Entries in the register shall be made chronologically within seven days of the transaction.

d) The register shall be kept in the custody of the company secretary of the company or any other person authorised for the purpose.

e) The register can be maintained either manually or in electronic mode and shall be authenticated by the company secretary or such other person as may be authorized in this behalf.

Section 186(10):

a) The register shall be kept at the registered office of the company and shall be preserved permanently.

b) The extracts from the register may be furnished to any member of the company on payment of fee, if any but not exceeding ten rupees for each page.

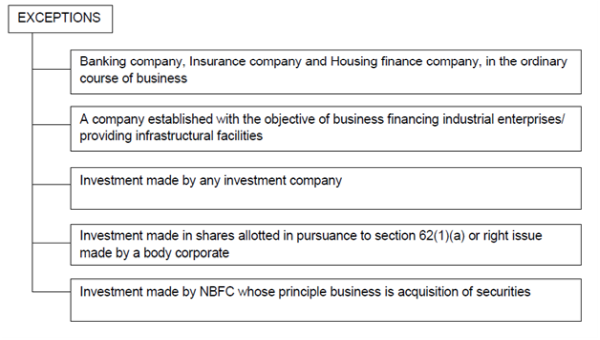

Section 186(11):

Nothing in this section, except sub-section (1), shall apply-

a) To any loan/guarantee/security or any investment by-

(i) Banking company, Insurance company and Housing finance company, in the ordinary course of business; and

(ii) A company established with the objective of business financing industrial enterprises/ providing infrastructural facilities

The expression 'business of financing industrial enterprises' shall mean business of giving of any loan to a person or providing any guaranty or security for due repayment of any loan availed by any person in the ordinary course of its business.

b) To any investment-

(i) Made by any investment company

(ii) Made in shares allotted in pursuance to section 62(1)(a) or right issue made by a body corporate

(iii) Made by NBFC whose principle business is acquisition of securities.

Section 186(12):

Central Government has prescribed Rule 11, 12 and 13 of Chapter XII The Companies (Meetings of Board and its Powers) Rules, 2014 in this regard.

Section 186(13): Penal Provisions-

In case of contravention, the company shall be punishable with minimum fine of Rs. 25,000 and maximum upto Rs. 5 Lac. and every officer in default shall be punishable with imprisonment for a term upto two years and with fine from Rs. 25,000 to Rs. 5 Lac.

The author can also be reached at harnotiapriyanka@gmail.com

DISCLAIMER: THE ENTIRE CONTENTS OF THIS DOCUMENT HAVE BEEN PREPARED ON THE BASIS OF RELEVANT PROVISIONS. THE INFORMATION STATED ABOVE IS NOT A PROFESSIONAL ADVICE OR LEGAL OPINION. IN NO EVENT I SHALL BE LIABLE FOR ANY DIRECT, INDIRECT, SPECIAL OR INCIDENTAL DAMAGE RESULTING FROM THE USE OF THE INFORMATION.

CAclubindia

CAclubindia