What is Internal Audit?

The Institute of Chartered Accountants of India defines 'Internal Audit' as follows:

'Internal audit is an independent management function, which involves a continuous and critical appraisal of the functioning of an entity with a view to suggest improvements thereto and add value to and strengthen the overall governance mechanism of the entity, including the entity's strategic risk management and internal control system. Internal audit, therefore, provides assurance that there is transparency in reporting, as a part of good governance.'

Why Internal Audit Required?

The globalization of business, growing complexity of transactions and new-age IT infrastructure have revolutionized the concept of trade and commerce. However, parallel to this great upsurge, another growing factor has been haunting corporate board rooms - that is the phenomenon of 'Risk'. There can be a liquidity risk, a fraud risk, a reputational risk, a competition risk and sundry other forms of risk. To combat and reduce risk, managements have come up with better Internal Controls. As a corollary, the Internal Audit profession too has witnessed a sea change from the traditional typical 'compliance' or 'transaction' audit to a much more dynamic 'Risk-based Audit', 'Controls Assessments', 'Controls Rationalization' and so forth.

Which corporates are liable for Internal Audit?

Earlier, internal audit was largely voluntary, and management used to appoint internal auditors as and when they felt the need. However, now with increased complexities in business, frauds and scams internal audit has become essential for most organisations. Internal audit has now gained so much importance that conducting internal audit has been made mandatory by the regulators for listed and other specified companies.

The following class of companies shall be required to appoint an internal auditor or a firm of internal auditors, namely: -

(a) every listed company - Always applicable

(b) every unlisted public company having -

- paid up share capital of fifty crore rupees or more during the preceding financial year; or

- turnover(income) of two hundred crore rupees or more during the preceding financial year; or

- outstanding loans or borrowings from banks or public financial institutions exceeding one hundred crore rupees or more at any point of time during the preceding financial year; or

- outstanding deposits of twenty-five crore rupees or more at any point of time during the preceding financial year; and

(c) every private company having -

- turnover of two hundred crore rupees or more during the preceding financial year; or

- outstanding loans or borrowings from banks or public financial institutions exceeding one hundred crore rupees or more at any point of time during the preceding financial year.

Who can be an Internal Auditor?

- Person to be appointed as Internal Auditor shall either be a Chartered Accountant or a Cost Accountant, or such other professional as may be decided by the board. Internal Auditor may or may not be an employee of the company. Chartered Accountant means a Chartered Accountant whether engaged in practice or not.

- Internal Auditor cannot be appointed by the board by passing a resolution by circulation.

- Statutory Auditor shall not be appointed as Internal Auditor of the Company.

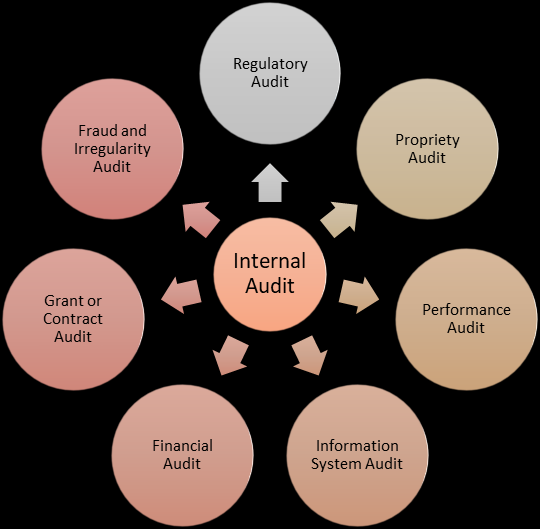

Types of Internal Audit

Stages of Internal Audit

Preliminary Survey

The preliminary survey lays the foundation for the audit project and proper organization of work. The preliminary survey is an overview of the audit topic and provides a firm foundation for the preparation of a risk-based audit program that concentrates on those matters which are of chief interest to management.

Planning Phase

During the planning phase of each project, the Internal Audit staff gather relevant background information and initiate contact with the client. Auditors meet with clients to identify risks and determine the objectives and scope of the audit as well as the timing of fieldwork and the report distribution.

Execution Phase

Once the audit is planned, fieldwork is executed by the Internal Audit staff. Clients are kept informed of the audit process through regular status meetings. We discuss audit observations, potential findings, and recommendations with the client as they are identified.

Reporting Phase

A summary of the audit findings, conclusions, and specific recommendations are officially communicated to the client through a draft report. Clients can respond to the report and submit an action plan and time frame. These responses become part of the final report which is distributed to the appropriate level of administration.

Follow-Up

Internal Audit follows up on all audit findings within one year of when the report was issued.

CAclubindia

CAclubindia