Ind AS-115 notified on 28.03.2018 by the Ministry of Corporate Affairs, effective from 01.04.2018.

Ind AS-115 provides single comprehensive framework to be used by entities to recognize revenue from their customers and report useful information about nature, amount, timing and uncertainty of cash flows arising from a customer. Ind AS-115 superseded the Ind AS-11 (Construction Contracts) & Ind AS-18 (Revenue).

1. Applicability

It applies to individual contract with customer. However, entity may apply it to a portfolio of contracts with similar characteristics if entity reasonably expects reasonably that effects of applying it to portfolio would not differ materially from that if applied to individual contracts.

However, this standard would not apply to:

i) Lease Contracts (Ind AS-17)

ii) Insurance Contracts (Ind AS-104)

iii) Financial Instruments and other contractual rights (Ind AS-109, 28)

iv) Non-Monetary exchanges between entities in same line of business

2. Model for Revenue Recognitions

Ind AS 115 is based on core principle that requires an entity to recognize revenue:

- In a manner that depicts the transfer of goods or services to customers

- At an amount that reflects the consideration the entity expects to be entitled to in exchange for those goods or services

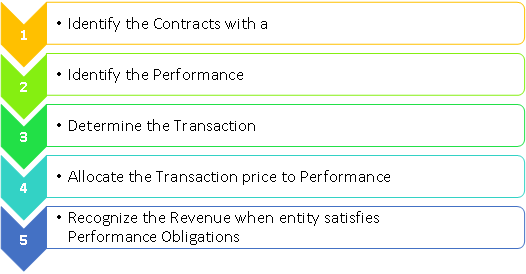

Ind AS 115 prescribes 5 Step model for recognition of revenue.

|

1 |

|

�??

Identify the

Contracts with a

Customer |

|

2 |

|

�??

Identify the

Performance Obligations |

|

3 |

|

�??

Determine the

Transaction Price |

|

4 |

|

�??

Allocate the

Transaction price to Performance

Obligations |

|

5 |

|

�??

Recognize the Revenue

when entity satisfies Performance

Obligations |

The first step for revenue recognition is identifying a contract with customer. Contract is defined as agreement between two or more parties that creates enforceable rights and obligations. A contract can be written, oral or implied by an entity's customary business practices.

This model applies only when:

� Contract has commercial substance

� Parties have approved the contract and are committed to perform their respective obligations

� Entity can identify

i) Each party's rights

ii) Payment terms for goods and services to be transferred

� It is probable that entity will collect the consideration

For purpose of Ind AS 115, a contract does not exist if each party has unilateral enforceable right to terminate a wholly unperformed contract without compensating the other party.

Two or more contracts may be combined as single contract if they are entered into at or near same time and meet any of following criteria:

i) Contracts were negotiated as a package with one commercial objective

ii) Amount paid under one contract is dependent on price or performance under other contract

iii) Goods or services to be transferred under the contracts constitute a single performance obligation

Contract Modifications

Contract modification arises when the parties approve a change in the scope and/or price of a contract, the accounting for same depends upon whether the modification is deemed to be a separate contract or not.

Entity shall account for modification as separate contract if:

� Scope increases due to addition of distinct- goods or services, AND

� Price increase reflects the goods' or services' standalone selling prices under circumstances of modified contract

Contract modification can be accounted for termination of existing contract and creation of a new contract if the remaining goods or services are distinct from the goods or services transferred on or before the date of contract modification.

If the remaining goods or services are not distinct and are part of a single performance obligation that is partially satisfied, entity should adjust both transaction price and measure of progress towards completion.

If remaining goods and services are combination of both scenarios, entity shall account for effect of modification on unsatisfied or partially satisfied performance obligations consistently.

4. Identify Performance Obligations

A Performance Obligation is a promise in a contract with customer to transfer either,

i) A good or service, or a bundle of goods or services, that is distinct OR

ii) A series of distinct goods or services that are substantially the same and have pattern of transfer to the customer

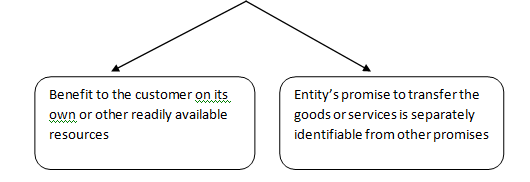

Goods or Services can be said to be Distinct - if both the following conditions are satisfied:

Series will be considered to have same pattern of transfer if

� Each distinct good or service meet the criteria to be performance obligation satisfied over a period of time; AND

� Same method would be used to measure entity's progress towards complete satisfaction of performance obligation

Performance Obligation is generally specified in contract, but could also include promises implied by entity's customary business practices, published policies or specific statement that create a valid customer expectation. However, it does not include administrative type tasks that do not result in transfer of good or service to customer.

In Ind AS 115, timing of revenue recognition is based on satisfaction of performance obligation rather than contract as a whole. Revenue should be recognized by measuring progress of complete satisfaction at end of every reporting period.

5. Determine the Transaction Price

Transaction Price is amount of consideration an entity expects to be entitled to in exchange for goods or services transferred, excluding any amounts collected on behalf of third parties (for example, GST, Electricity Tax etc.)

Transaction Price is not adjusted for customer's credit risk, but is adjusted if entity has created a valid expectation that it will enforce its rights for only a portion of contract price.

Variable Consideration

Amount of consideration may include a variable component like discount, rebates, credits, refunds, price concessions, incentives and similar items. To estimate the transaction price in a contract that includes variable consideration, entity may use any of two methods:

- Expected Value - Sum of probability weighted amounts in range of possible consideration

- Most Likely Amount

An entity should use one method consistently to estimate the transaction price throughout the life of a contract. An entity that expects to refund a portion of the consideration to the customer would recognize a liability for the amount of consideration it reasonably expects to refund. The entity would update the refund liability each reporting period based on current facts and circumstances.

Constraint on Variable Consideration

If the amount of consideration from a customer contract is variable, an entity is required to evaluate whether the cumulative amount of revenue recognized should be constrained. The objective of the constraint is for an entity to recognize revenue only to the extent that it is highly probable that there will not be a significant reversal (i.e. significant downward adjustment) when the uncertainty associated with the variable consideration subsequently resolves.

In assessing the uncertainty related to variable consideration, an entity should consider both the likelihood and the magnitude of revenue reversal. Following are the factors that indicate the high probability of revenue reversal related to the amount of consideration:

� High susceptibility to factors outside entity's control

� Uncertainty exists and it's expected to resolve for a long time

� Entity's experience has limited predictive value has a large range of possible consideration amounts etc.

Time Value of Money

An entity must reflect the time value of money in its estimate of the transaction price if the contract includes a significant financing component. The objective in adjusting the transaction price for the time value of money is to reflect an amount for the selling price as though the customer had paid cash for the goods or services when they were transferred.

In assessing if a contract contains a significant financing component; an entity should consider the relevant facts including both of the following:

� Difference between the amount of promised consideration and the cash selling price of the goods or services.

� The combined effect of the prevailing interest rate in the market and expected length of time between when the transfer of goods or services and the time when the customer makes the payment.

As a practical expedient, an entity can ignore the impact of the time value of money on a contract if it expects, at contract inception, that the period between the delivery of goods or services and customer payment will be one year or less.

Non-Cash Consideration

If a customer promises consideration in a form other than cash, an entity measures the non- cash consideration at fair value in determining the transaction price. This includes arrangements in which the customer transfers control of goods or services (e.g. materials, equipment, labour) to facilitate the entity's fulfillment of the contract.

If an entity is unable to reasonably measure the fair value of non-cash consideration, it indirectly measures the consideration by referring to the stand-alone selling price of the goods or services promised under the contract.

Consideration payable to Customer

Consideration payable to the customer includes cash amounts, credits or other items (voucher or coupon) and entity account it as a reduction of transaction price (revenue). An entity should recognize the reduction of revenue when (or as) either of the following events occurs:

� Recognizes revenue for the transfer of related goods or service to the customer

� Pays or promises to pay the consideration

6. Allocation of Transaction Price to Performance Obligation

An entity shall allocate transaction price to each separate performance obligation within that contract on a relative stand-alone selling price basis. Stand-alone selling price is price at which entity would sell a promised good or service separately to a customer. If price is not directly available it should be estimated using:

|

Method |

Description |

|

Adjusted Market Assessment Approach |

Involves evaluating the market in which the entity sells goods or services and estimating the price that customers in that market would pay for those goods or services. An entity might also consider price information from its competitors and adjust that information for the entity's particular costs and margins. |

|

Expected cost plus margin approach |

An entity would forecast its expected costs to provide goods or services and add an appropriate margin. |

|

Residual Approach |

Involves subtracting the sum of observable stand-alone selling prices for other goods and services promised under the contract from the total transaction price to arrive at an estimated selling price for a good or service. This method is permitted only if the entity either: � Sells the same good/service to different customers (at or near the same time) for a broad range of amounts; or � Has not yet established price for the good/ service and the good/ service has not previously been sold on a stand-alone basis. |

Allocating discounts & Variable Considerations

If the sum of the stand-alone selling prices for the promised goods or services exceeds the contract's total consideration, an entity treats the excess as a discount to be allocated to the separate performance obligations on a relative standalone selling price basis. However, an entity would allocate a discount to only some of the performance obligations only if it has observable evidence of the obligations to which the entire discount belongs.

Variable consideration may be attributable to the entire contract or only to a specific part. Ind AS 115 requires that variable consideration is allocated entirely to a single performance obligation (or to a distinct good or service that forms part of a performance obligation) if and only if both of the following conditions have been met:

o The terms of the variable payment relate specifically to the entity's efforts towards, or outcome from, satisfying that performance obligation (or distinct good or service)

o The result of the allocation is consistent with the amount of consideration to which the entity expects to be entitled in exchange for the promised goods or services

7. Recognize Revenue when or as an Entity satisfies Performance Obligations

An entity recognizes revenue when or as it transfers promised goods or services to a customer. Atransfer' occurs when the customer obtains control of the good or service.

A customer obtains control of an asset (good or service) when it can direct the use of and obtain substantially all the remaining benefits from it. Control includes the ability to prevent other entities from directing the use of and obtaining the benefits from an asset.

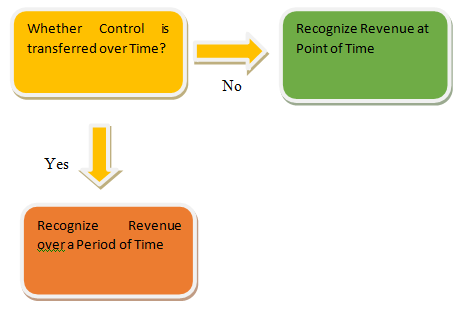

Transfer of Control over a period of Time

An entity determines at contract inception whether each performance obligation will be satisfied (that is, control will be transferred) over time or at a specific point in time.

Control is considered to be transferred over time if one of the following conditions exists:

� Customer controls the asset as it is created or enhanced by entity's performance under the contract

� A customer receives a benefit from the entity's performance as the entity performs

� The entity's performance creates or enhances an asset that has no alternative use to the entity, and the entity has the right to receive payment for work performed to date.

An entity recognizes over time revenue that is associated with a performance obligation that is satisfied over time by measuring its progress toward completion of that performance obligation. The entity must update this measurement over time as circumstances change and accounts for these changes as a change in accounting estimate under Ind AS 8Accounting Policies, Changes in Accounting Estimates and Errors'.

Transfer of Control at a Point of Time

In situations where control over an asset (goods or services) is transferred at a single point in time, an entity recognizes revenue by evaluating when the customer obtains control of the asset.

Control Indicators

i) Transfer of Legal Title

ii) Physical Possession

iii) Customer has significant risk and rewards

iv) Customer's acceptance

v) Entity has present right to payment

8. Contract Costs

Under new standard, an entity is required to capitalize certain costs incurred in obtaining a contract if specified criteria are met. Ind AS 115 provides following guidance in respect of recognition of contract costs:

� Incremental cost of obtaining contract with a customer: Entity should recognize as an asset if it expects to recover those costs. These are expenses that would not have incurred if contract had not been obtained, i.e., costs incurred are direct incremental costs associated with obtaining contract. (E.g.- Sales Commission etc.)

� Cost to fulfill a Contract: An entity should recognize an asset for cost incurred to fulfill a contract if those costs:

� Relate directly to an existing contract or specific anticipated contract

� Generate or enhance resources that will be used in satisfying Performance Obligation in future

� Are expected to be recovered

Judgment would be required to assess which costs should be capitalized and for determination of appropriate period and pattern of amortization. However, a practical expedient allows an entity to expense as incurred, incremental costs of obtaining a contract if amortization period of asset would be a year or less.

9. Presentation

When either party to a contract has performed, en entity shall present the contract in the balance sheet as a contract asset or a contract liability, depending on the relationship between

the entity's performance and the customer's payment. An entity shall present any unconditional rights to consideration separately as a receivable.

|

Sl. No |

Event |

Action |

|

1 |

Customer pays (or due to pay) consideration an entity has an unconditional right to the consideration before the transfer of goods or service |

Entity should present the contract as a contract liability |

|

2 |

Entity transfers the goods or services before the customer pay (or due to pay) |

Entity should present the contract as a contract asset, exclude any amount presented as receivable |

10. Disclosures

Following disclosures are required under Ind AS 115:

i) Revenue recognized from contracts with customers, separately from its other sources of revenue

ii) Impairment losses on receivables or contract assets

iii) Categories that depict the nature, amount, timing, and uncertainty of revenue and cash flows

iv) Sufficient information to enable users of financial statements to understand the relationship with revenue information disclosed for reportable segments under Ind AS 108Operating Segments'

v) Opening and closing balances of contract assets, contract liabilities, and receivables (if not separately presented)

vi) Revenue recognized in the period that was included in contract liabilities at the beginning of the period and revenue from performance obligations (wholly or partly) satisfied in prior periods

vii) Explanation of relationship between timing of satisfying performance obligations and payment

viii) Explanation of significant changes in the balances of contract assets and liabilities

ix) When the entity typically satisfies performance obligations

x) Significant payment terms

xi) Nature of goods and services

xii) Obligations for returns, refunds and similar obligations

xiii) Types of warranties and related obligations

xiv) Aggregate amount of transaction price allocated to remaining performance obligations at end of period*

xv) Judgments impacting the expected timing of satisfying performance obligations

xvi) Methods used to recognize revenue for performance satisfied over time, and explanation

xvii) The transaction price and amounts allocated to performance obligations (e.g. estimating variable consideration and assessing if constrained and allocating to performance obligations)

xviii) Reconciliation of the amount of revenue recognized in the statement of profit and loss with the contracted price showing separately each of the adjustments made to the contract price specifying the nature and amount of each such adjustment separately (carve-out)

11. Transition

Ind AS 115 is effective from annual reporting period beginning on or after April 1, 2018.

Ind AS 115 requires retrospective application. It permits either

� Full Retrospective' adoption in which the standard is applied to all of the periods presented; OR

� Modified Retrospective' adoption. Entities that elect themodified retrospective' method will not restate financial information for the comparative period. However, this does not imply that entities can ignore past revenue contracts. Rather, they will be required to calculate cumulative catch-up impact on all open contracts and make adjustment to the retained earnings as on April 1, 2018. In addition, they must disclose the amount by which each financial statement line is impacted due to Ind AS 115 application in the current period for the year ended March 2018. This will require entities to maintain two accounting records in the year of adoption�one as per Ind AS 115 and the other as per Ind AS 11 and/or 18 to comply with the disclosure requirement.

12. Impact

From 'Risk & Rewards' to 'Control' Model

Ind AS 115 brings a conceptual change in revenue recognition as it prescribes for revenue recognition when customer obtains controls of a good or service, whereas under existing principles of Ind AS, revenue is recognized when there is transfer of risk and rewards.

Promises made to Customers

It focuses heavily on what the customer expects from a supplier under a contract. Companies will have to necessarily determine if there are multiple distinct promises in a contract or a single performance obligation (PO). These promises may be may be explicit, implicit or based on past customary business practices. The consideration will then be allocated to multiple POs and revenue recognized when control over those distinct goods or services is transferred.

Variable Consideration

Entities may agree to provide goods or services for consideration that varies upon certain future events which may or may not occur. This is variable consideration, a wide term and includes all types of negative and positive adjustments to the revenue. Some of the concepts introduced by Ind AS 115 are completely new like upward adjustment of revenue.

Time Value of Money

Now, entities will have to adjust the transaction price for the time value of money. Where the collections from customers are deferred the revenue will be lower than the contract price, and interestingly in case of advance collections, the effect will be opposite resulting is revenue exceeding the contract price with the difference accounted as a finance expense.

This may impact entities having significant advance or deferred collection arrangements e.g. real estate infrastructure, EPC (Engineering, Procurement and Construction), IT services, etc.

The new standard can result in both increases and decreases in previously reported revenues. But importantly entities will have to closely analyze their business practices within the revenue cycle including changes to customer contracts, IT systems, tax implications, the introduction of new processes or controls, changes to management KPIs, disclosures and broader stakeholder communication.

Major impact would be seen on following sectors:

- Construction and Real Estate

- Technology

- Aero-space & Defense

- Pharmaceuticals

- Telecommunications

The author is CA-Final Student and may be contacted at damanoberoi@hotmail.com

CAclubindia

CAclubindia