Background

Today we live in a dynamic business world, where changes in business environment are eminent. Some of these changes are important for users of financial statements such as shareholders, because they play a key role in decision making. In order to bring about uniformity in changes in business environment occuring after the reporting period (eg: 31st March), this standard has been brought into effect.

The current IndAS 10 is based on 'IAS 10: Events occuring after the reporting period' which was originally issued in 1978, and which underwent a major amendment in 2003.

Preliminaries

Before we go into the standard, let us quickly recollect some preliminaries:

- Financial statements are reports on the financial performance and position of any entity.

-

Financial statements comprise of Balance Sheet, Income Statement, and Statement of Cash Flows

-

In many countries, financial statements are required to be ‘approved’ by the Board, or an equivalent authority, before releasing it to stakeholders.

-

The approval of these financial statements could take several weeks or months.

Let us look at an example below:

In this case, the financial statements were approved by the Board on 15th January. Therefore, this standard applies to all events between the closing of accounts (31st December) and 15th January (as given in the example).

The standard prescribes when an entity should adjust its financial statements for events after the reporting period. The standard also prescribes disclosure requirements regarding events after the reporting period.

Let us look at another example:

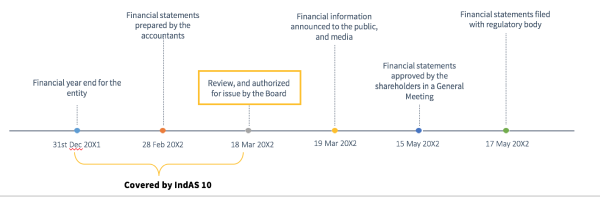

The management of an entity completes draft financial statements for the year to 31 December 20X1 on 28 February 20X2. On 18 March 20X2, the board of directors reviews the financial statements and authorizes them for issue. The entity announces its profit and selected other financial information on 19 March 20X2. The shareholders approve the financial statements at their annual meeting on 15 May 20X2 and the approved financial statements are then filed with a regulatory body on 17 May 20X2.

In this case, all events between 31st December 20X1 and 18 Mar 20X2 are covered by this standard.

Adjusting and Non-Adjusting Events

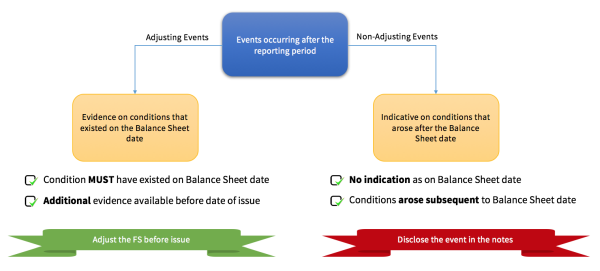

According to IndAS 10, all events between the end of the reporting period, up to the date on which they were authorized for issue, can be classified into two:

1. Adjusting Event: Where there is a condition that existed on the Balance Sheet date, and additional evidence is available before the financial statements were issued; and

2. Non-Adjusting Event: Where no indication of the event was available as on the Balance Sheet date, and such conditions arose after the Balance Sheet date.

The standard requires adjusting events to be effected in the financial statements by passing necessary entries, while for non-adjusting events mere disclosure is sufficient.

Let us look at some examples:

-

Court case existed on 31st December 20X1

-

Additional evidence after the reporting period

-

Classified as: Adjusting Event

-

Treatment: Increase the provision of $80,000 to $100,000 as on 31st December 20X1

- Customer balance existed on 31st December 20X1

-

Additional evidence after the reporting period

-

Classified as: Adjusting Event

-

Treatment: Create a provision to write-off the receivables as on 31st December 20X1

-

Downturn did not exist on 31st December 20X1

-

Condition arose subsequent to the Balance Sheet date

-

Classified as: Non-Adjusting Event

-

Treatment: Disclosure in notes to accounts. No adjustment necessary.

Other Examples of Non-Adjusting Events

- A major business combination after the reporting period or disposing of a major subsidiary

-

Announcing a plan to discontinue an operation

-

Destruction of a major production plant by a fire after the reporting period

-

Announcing, or commencing the implementation of, a major restructuring

-

Abnormally large changes after the reporting period in asset prices or foreign exchange rates

-

Changes in tax rates or tax laws enacted or announced after the reporting period

-

Commencing major litigation arising solely out of events that occurred after the reporting period

Dividends and Going Concern

- IndAS 10 clearly states that an entity shall not recognize proposed dividends as a liability at the end of the reporting period.

-

Such dividends are disclosed in the notes in accordance with IndAS 1 Presentation of Financial Statements.

-

In case of ‘Going Concern’ assumption becoming invalid after the end of the reporting period, this Standard requires a fundamental change in the basis of accounting, rather than an adjustment to the amounts recognized within the original basis of accounting.

Key Disclosures

- An entity shall disclose the date when the financial statements were authorized for issue and who gave that authorization.

-

If the entity’s owners or others have the power to amend the financial statements after issue, the entity shall disclose that fact.

The author is a Chartered Accountant (FCA), a Certified Public Accountant (CPA, Australia), a Certified Information Systems Auditor (CISA), and a Chartered Management Accountant (CIMA, UK).

CAclubindia

CAclubindia