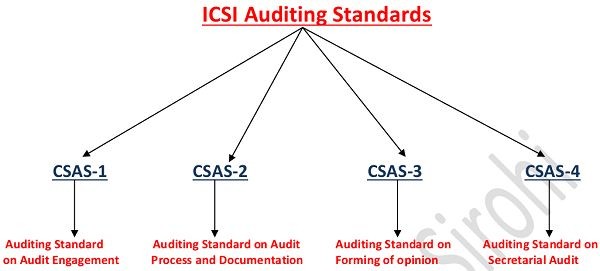

CSAS-1

Auditing Standard on Audit Engagement

Applicability:

1. Applicable to Auditor undertaking Audit Engagement under any Statute.

2. CSAS-1 deals with the Auditor’s role and responsibilities w.r.t Audit Engagement and the process of entering into an understanding/ agreement with the Appointing Authority.

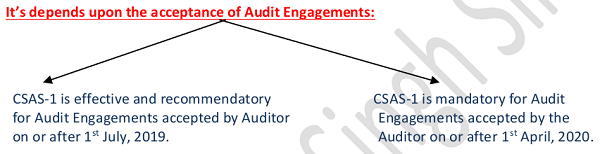

Effective Date:

Objective:

CSAS-1 is to prescribers for Auditors, principles and procedures to be followed while accepting or continuing with an Audit Engagement by agreeing to the terms of Engagement with the Appointing Authority or changes therein and matters relating thereto.

Definitions:

Appointing Authority: any person having authority to appoint Auditor.

Audit Engagement: means-

1. Detailed terms of appointment,

2. Scope of Audit,

3. Remuneration and limiting conditions, if any.

Auditee: a person who subject to Audit.

Auditor: means-

1. A Company Secretary in practice under Section 2 (2) of Company Secretaries Act, 1980, including,

2. A firm or,

3. A LLP registered with ICSI.

Management: means-

1. Board of Directors and,

2. Person who has been entrusted with the responsibility of governance and compliances of the Auditee.

Predecessor or Previous Auditor:

an Auditor who has conducted the most recent audit assignment of the Auditee and submitted report thereon prior to the incumbent Auditor or was engaged but did not complete the audit assignment due to his resignation, termination or otherwise.

1. Audit Engagement Process

Steps with respect to the Audit Engagement:

Appointment:

1. Appointment shall be as per law, act, rules, regulations, standards and guidelines, or

2. in case no such manner has been prescribed, such appointment shall be made in the manner determined by the Appointing Authority.

3. The Auditor shall submit a Certificate to the Appointing Authority confirming eligibility for appointment as Auditor.

4. The Auditor shall obtain an Audit Engagement Letter along with a copy of the resolution, if any, passed by the Appointing Authority and shall provide acceptance to the Appointing Authority.

Audit Engagement Letter: includes-

1. The objective and scope of the audit;

2. The responsibilities of the Auditor and the Auditee;

3. Written representations provided and/or to be provided by the Management to the Auditor, including particulars of the Predecessor or Previous Auditor;

4. The period within which the audit report shall be submitted by the Auditor, along with milestones, if any;

5. The commercial terms regarding audit fees and reimbursement of out of pocket expenses in connection with the audit; and

6. Limitations of audit, if any.

Intimation to the Predecessor or Previous Auditor:

The Auditor shall intimate in writing to the Predecessor or Previous Auditor, if any, before accepting the Audit Engagement.

2. Limits on Audit Engagements

The Auditor shall accept Audit Engagements within the limits of number of audits, if any, as may be prescribed under any law for the time being in force or by the ICSI from time to time.

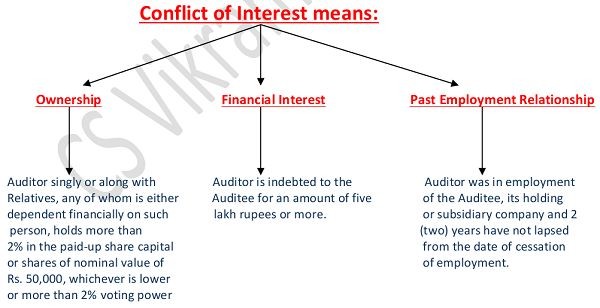

3. Conflict of Interest

The Auditor shall not have any substantial conflict of interest with the Auditee.

Explanation:

4. Confidentiality

1. The Auditor shall not disclose the information obtained during the course of Audit without proper and specific authority or unless there is a legal obligation or duty to disclose.

2. The Auditor shall not use or share with any person any information obtained except for the purposes of audit.

3. The Auditor shall take all reasonable steps to ensure that employees, staff and other team members of the Auditor and persons engaged by the Auditor to provide advice or assistance during the conduct of audit, shall also adhere to the Auditor’s duty of confidentiality.

5. Changes in terms of engagement

1. The Auditor shall not agree to a change in the terms of the Audit Engagement where there is no reasonable justification for doing so.

2. If before completion of the assignment, the Auditor is requested by the Appointing Authority to change the scope of engagement, resulting in a lower level of assurance, the Auditor shall consider the appropriateness of carrying out the same.

3. If the terms of the Audit Engagement are changed, the Auditor and the Appointing Authority shall agree on the new terms of the engagement by way of a supplementary/revised engagement letter or any other suitable form in writing.

CSAS-2

Auditing Standard on Audit Process and Documentation

Applicability:

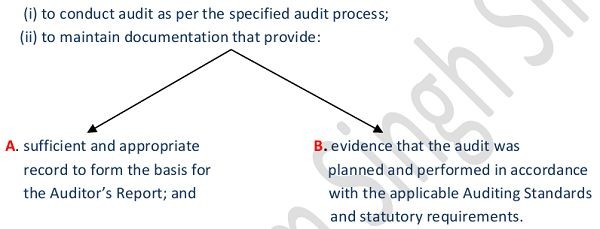

CSAS-2 deals with responsibilities and duties of the Auditor with respect to Audit Process in conducting audit and maintaining proper audit records.

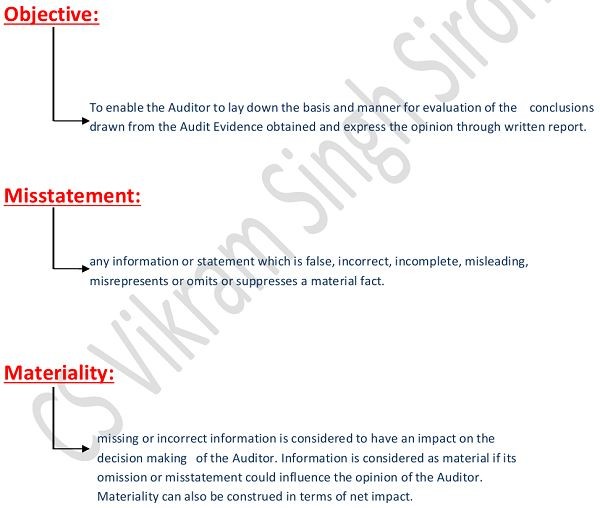

Objective:

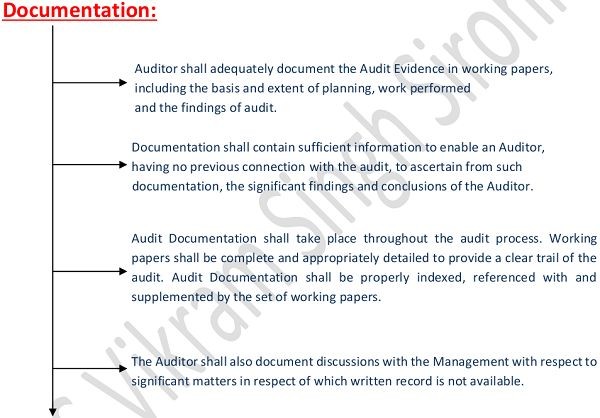

Audit Documentation

↓

working papers prepared or records obtained by the Auditor in connection with the audit.

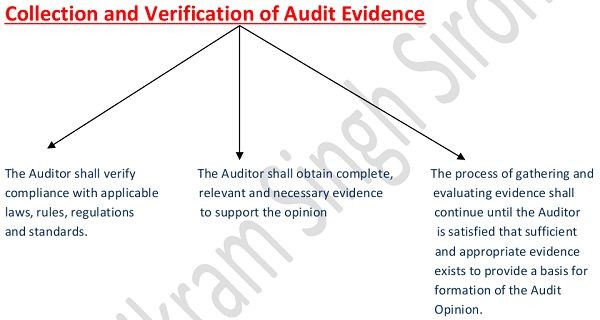

Audit Evidence

↓

relevant information and documents gathered in the course of the audit for arriving at the conclusion on which the Auditor’s opinion is based.

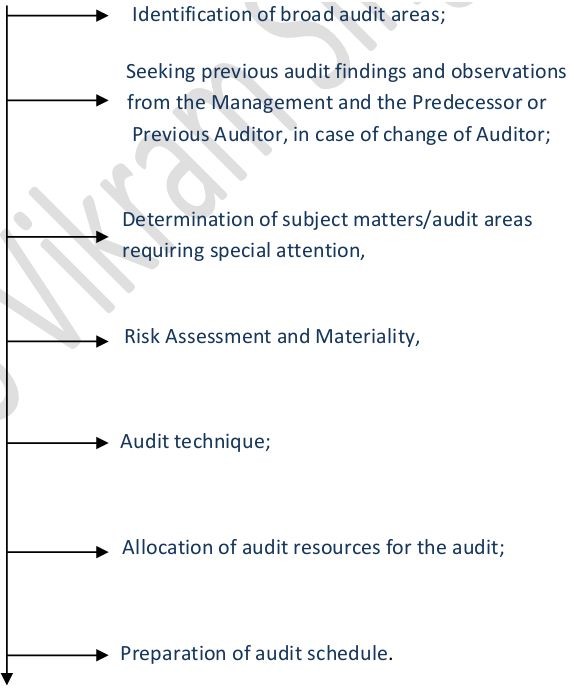

Audit Planning: Audit planning means establishing and developing an overall audit process, including but not limited to:

Information about the Auditee:

sufficient information about the Auditee that is relevant for conduct of audit and forming an opinion and its expression

Audit Checklists:

The Auditor shall use systematic and comprehensive audit check-lists for carrying out the audit and to verify the compliance requirements.

Third Party Confirmation:

The Auditor shall obtain confirmations from third party(ies), wherever required, with respect to information which is related to such party(ies).

CSAS-3

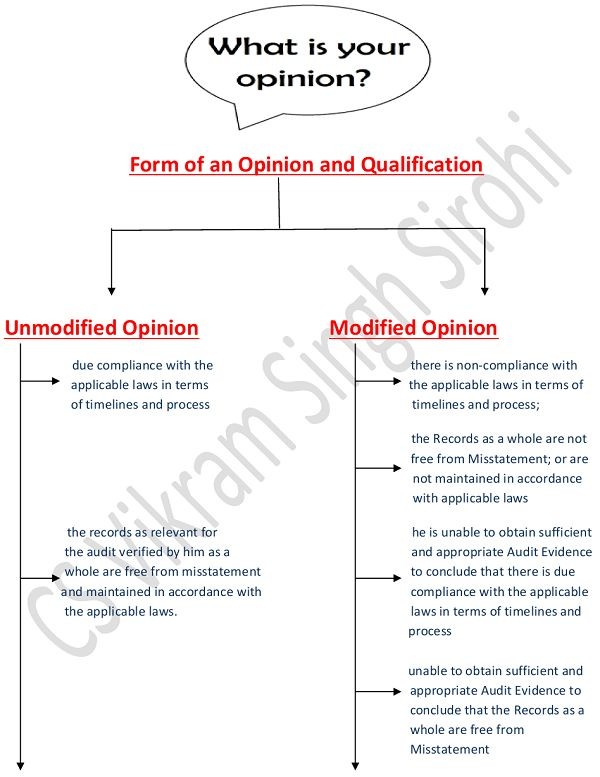

Auditing Standard on Forming of Opinion

Applicability:

CSAS-3 deals with basis and manner for forming Auditor’s opinion on subject matter of the audit.

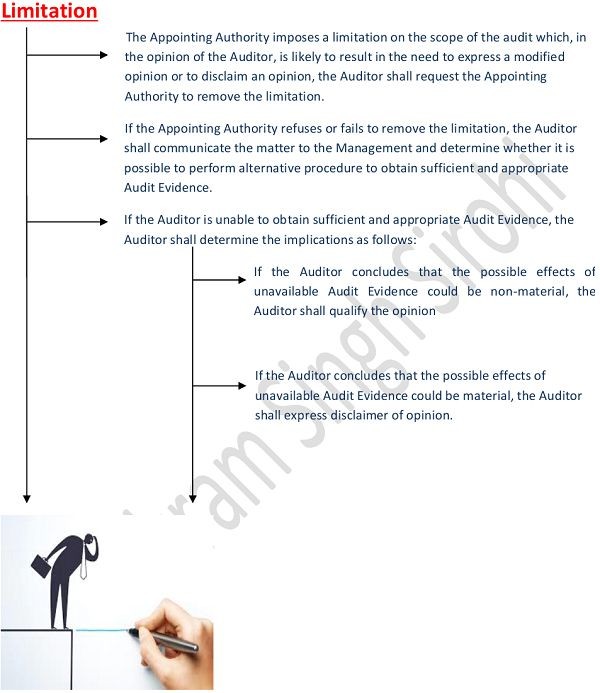

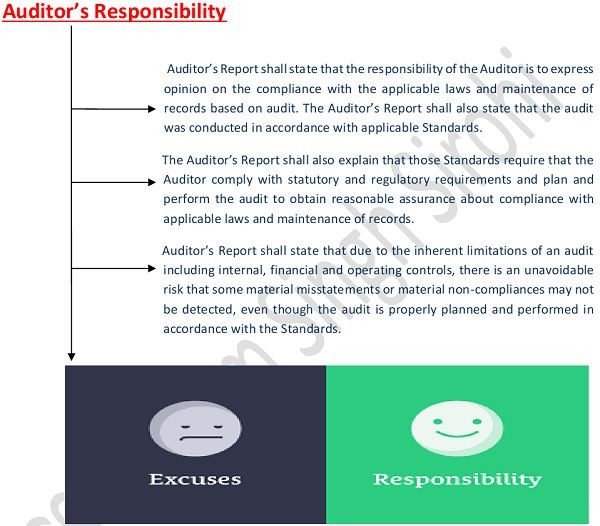

Process for forming of opinion:

The Auditor shall consider Materiality while forming his opinion and adhere to-

Judgment, Clarification and Conflicting Interpretation:

The Auditor may consider various judgments, clarifications, opinion, conflicting interpretations while framing the opinion to the best of his professional acumen.

Precedence and Practices:

The Auditor shall adhere to generally accepted precedence and practices in relation to forming of an opinion as may be available from historical perspective of any kind of audit.

CSAS-4

Auditing Standard on Secretarial Audit

Applicability:

CSAS-4 is applicable to the Auditor undertaking Secretarial Audit under Section 204 of the Companies Act, 2013 and rules made thereunder. The Standard deals with basis and manner for carrying out the Secretarial Audit.

Adherence to other Auditing Standards:

The Auditor shall adhere to the Auditing Standards on – (a) Audit Engagement (CSAS-1); (b) Audit Process and Documentation (CSAS-2); and (c) Forming of Opinion (CSAS-3).

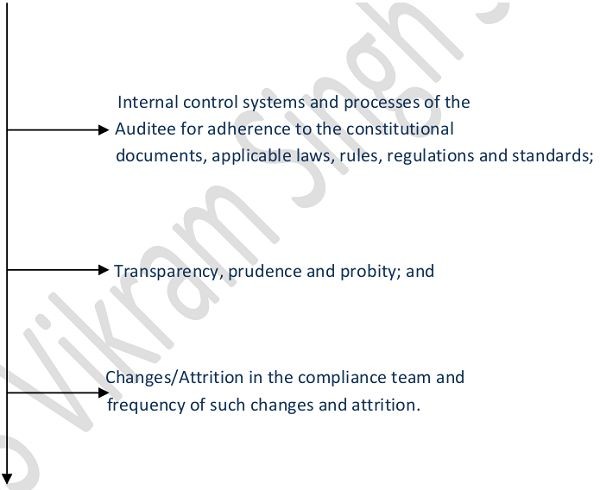

Identification and segregation of applicable laws:

The Auditor shall take note of the industry specific laws and other laws as may be applicable to the Auditee based on the identification/segregation by the Management and his own verification.

CAclubindia

CAclubindia