SOURCES OF FUNDS

Explanation:

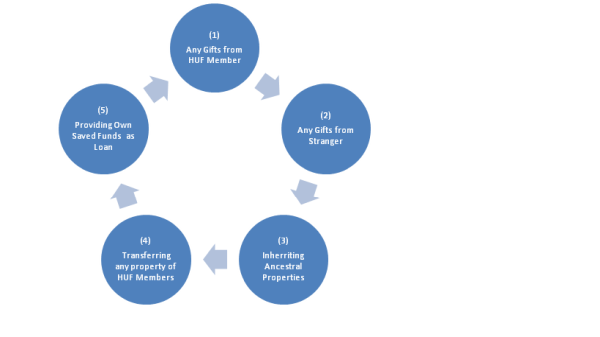

- Any gifts in cash or in kind received by a HUF from their members are tax free. Also gift received by any person from any relatives is tax free. Hence a member can receive any gift from their relatives and subsequently may gift the same to their HUF.

- Any gifts in cash or in kind from a stranger to an amount not exceeding Rs. 50K is tax free.

- Ancestral property can be inherited by way of a will or gift and thereafter it can be transferred by a member to its HUF as a gift.

- HUF member can themselves transfer their own property to its HUF as a gift.

- Members of HUF can provide interest free loans to its HUF, provided that such funds should be their own saved and taxed funds. It should not be borrowed funds.

INCOME FROM HOUSE PROPERTY:

- Can claim one property as Self Occupied

- Can Let out property and thereby offer the rent income in HUF for tax savings

- Can claim interest on borrowed funds

- Can claim standard deduction on let out property

INCOME FROM OTHER SOURCES:

- Can invest gifts received amounts to earn extra income through HUF rather than keeping it idle in individual A/c.

- Can invest loans received amounts to earn extra income through HUF rather than keeping it idle in individual A/c.

INVESTMENT OPTIONS:

- Equity Shares &Debentures

- Mutual Funds

- Bonds

- Fixed Deposits

- Real Estate

- Partnership firms

TAX BENEFITS:

- Basic tax threshold limit of Rs. 250K

- Interest on Housing Loan

- Investment U/s 80 C

- Mediclaim U/s 80 D

- All other tax benefits as available to Individual tax payer.

As per Income tax Act, 1961. Relative Includes:

(i) in case of an individual

(A) spouse of the individual;

(B) brother or sister of the individual;

(C) brother or sister of the spouse of the individual;

(D) brother or sister of either of the parents of the individual;

(E) any lineal ascendant or descendant of the individual;

(F) any lineal ascendant or descendant of the spouse of the individual;

(G) spouse of the person referred to in items (B) to (F); and

(ii) in case of a Hindu undivided family, any member thereof.

CAclubindia

CAclubindia