A financial report is a formal record of the financial activities of a business, person, or other entity. Relevant financial information is presented in a structured manner and in a form easy to understand, including related notes.

Financial Statements intended to communicate an entity’s economic resources or obligation at a point of time or changes therein for a period of time in accordance with a financial reporting framework

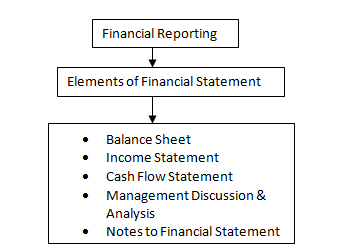

The related notes ordinarily comprise a summary of significant accounting policies and other explanatory information. Usually it means and includes balance sheet, profit & loss account, cash flow statement (if required by law), Notes to the accounts and significant accounting policies are considered an integral part of the financial statements. In summary it includes basic financial statements, accompanied by a management discussion and analysis. Preparation and presentation of financial statement is responsibility of management and those charged with governance.

The financial reporting framework (FRF) adopted by management and, where appropriate, those charged with governance in the preparation and presentation of the financial statements that is acceptable in view of the nature of the entity and the objective of the financial statements, or that is required by the law or regulation. For example under Companies Act the FRF is Schedule VI and the accounting standards. In banks the FRF means financial statements required in specific format and with RBI guidelines for income recognition (Standard and NPA advances) and Asset classification (sub-standard, doubtful, loss assets).

The objective of financial statements is to provide information about the financial position, performance and changes in financial position of an enterprise that is useful to a wide range of users in making economic decisions. Financial statements should be understandable, relevant, reliable and comparable. Reported assets, liabilities, equity, income and expenses are directly related to an organization's financial position.

Financial statements are intended to be understandable by readers who have "a reasonable knowledge of business and economic activities and accounting and who are willing to study the information diligently. Financial statements may be used by users for different purposes:

· Owners and managers require financial statements to make important business decisions that affect its continued operations. Financial analysis is then performed on these statements to provide management with a more detailed understanding of the figures. These statements are also used as part of management's annual report to the stockholders.

· Employees also need these reports in making collective bargaining agreements (CBA) with the management, in the case of labor unions or for individuals in discussing their compensation, promotion and rankings.

· Prospective investors make use of financial statements to assess the viability of investing in a business. Financial analyses are often used by investors and are prepared by professionals (financial analysts), thus providing them with the basis for making investment decisions.

· Financial institutions (banks and other lending companies) use them to decide whether to grant a company with fresh working capital or extend debt securities (such as a long-term bank loanor debentures) to finance expansion and other significant expenditures.

Different countries have developed their own accounting principles over time, making international comparisons of companies difficult. To ensure uniformity and comparability between financial statements prepared by different companies, a set of guidelines and rules are used. Commonly referred to as Generally Accepted Accounting Principles (GAAP), these set of guidelines provide the basis in the preparation of financial statements, although many companies voluntarily disclose information beyond the scope of such requirements.

Although laws differ from country to country, an audit of the financial statements of a public company is usually required for investment, financing, and tax purposes. These are usually performed by independent accountants or auditing firms. Results of the audit are summarized in an audit report that either provide an unqualified opinion on the financial statements or qualifications as to its fairness and accuracy. The audit opinion on the financial statements is usually included in the annual report.

There has been much legal debate over who an auditor is liable to. Since audit reports tend to be addressed to the current shareholders, it is commonly thought that they owe a legal duty of care to them.

In the United States, especially in the post-Enron era there has been substantial concern about the accuracy of financial statements. Corporate officers (the chief executive officer (CEO) and chief financial officer (CFO)) are personally responsible for fair financial reporting allowing those reading the report to have a good sense of the organization.

To conclude, the financial statement should show the financial information, which are truthfully recorded and are fairly presented in the financial reporting framework ensuring true and fair view of the financial position of the entity.

Click Here to view Rahul Malkan's Class on Financial Reporting

CAclubindia

CAclubindia